Inflationsspöket väcks till liv med nya energichocken

När inflationen just såg ut att vara besegrad kom nästa smäll. Irankriget har åter skakat energimarknaden, med stigande olje- och bensinpriser som följd. För hushållen betyder det risk för en ny runda av dyrare transporter, el och varor, skriver The Economist.

Bedömare tror visserligen inte att världen står inför en akut recession, men väl att levnadskostnaderna kan börja rusa igen.

Om oljepriset biter sig fast på höga nivåer kan inflationen ta ny fart – och sätta både centralbanker och regeringar under hård press.

How high could global inflation go?

With luck, the Iran war won’t cause a recession. But the surge in energy prices will push up the cost of living.

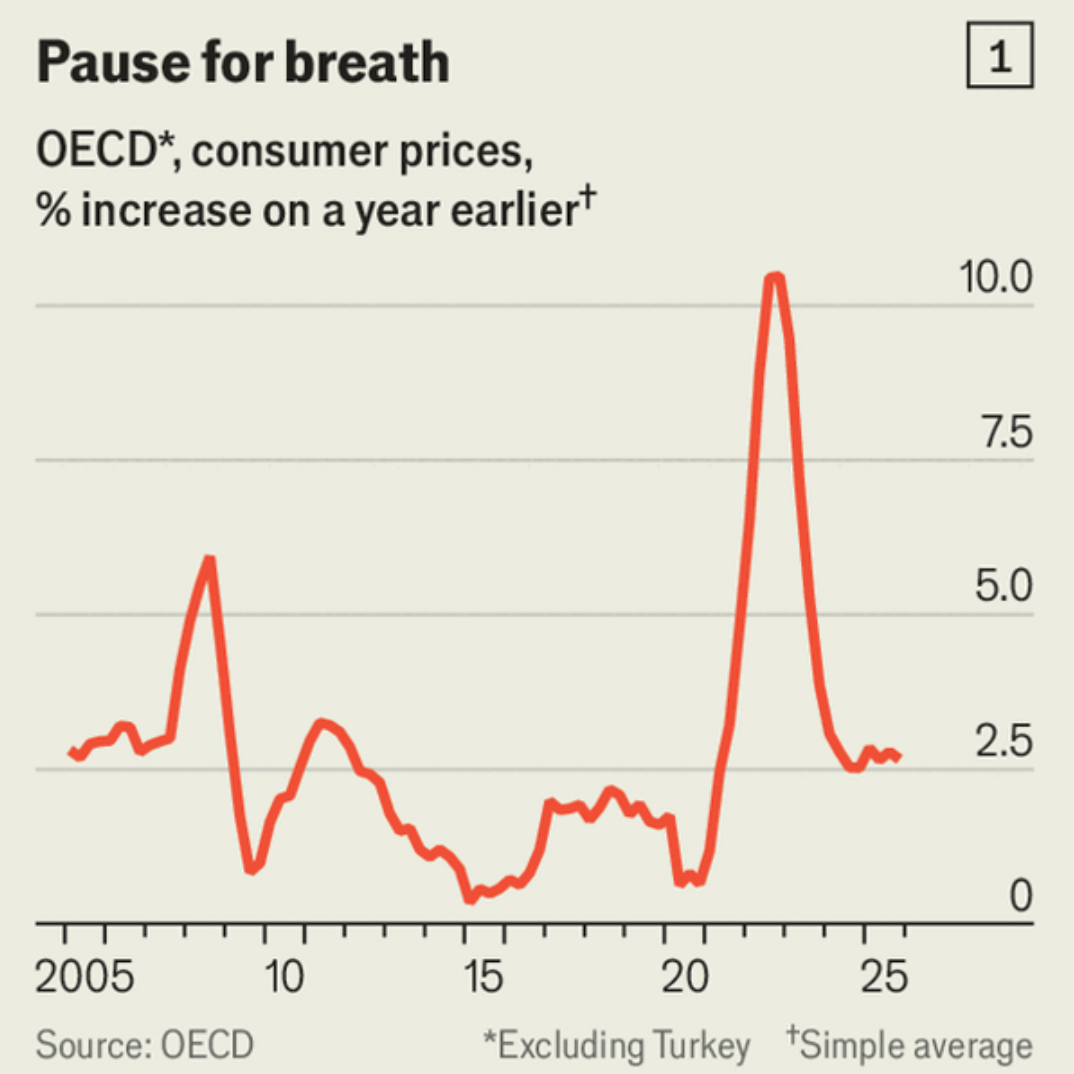

After peaking at more than 10% in late 2022, owing to post-pandemic supply-chain snarl-ups, overgenerous stimulus cheques and an energy shock from Russia’s full-scale invasion of Ukraine, average inflation across the rich world fell. By the beginning of this year it was near 2% (see chart 1). Central bankers thought they had slain the inflationary beast.

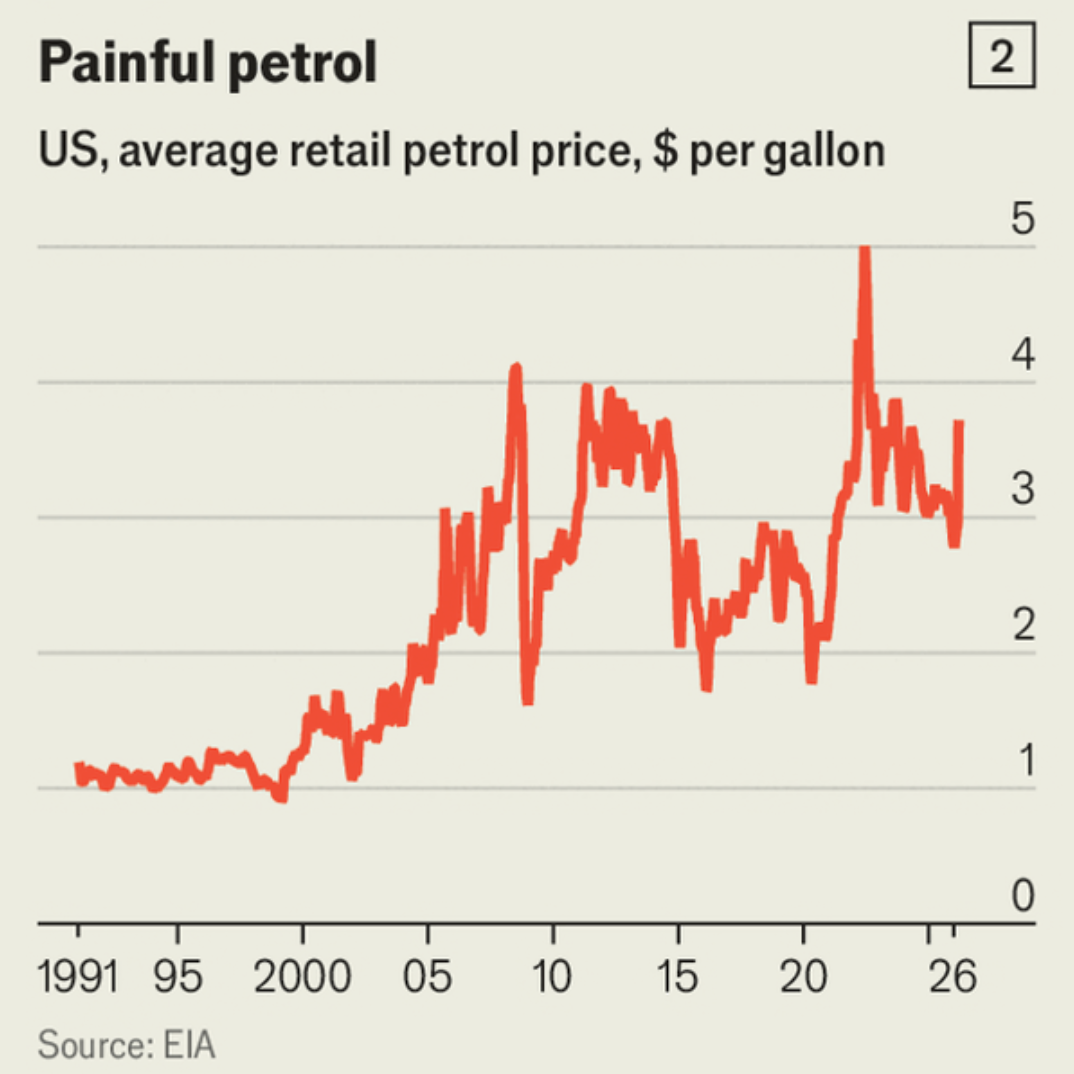

Just as they turned away, however, its eye twitched open. America’s and Israel’s war against Iran has disrupted energy markets once again. Even as Donald Trump seeks to soothe markets by saying hostilities could end soon, flows of oil through the Strait of Hormuz remain perhaps 97% below normal levels. Outmatched by its enemies on the battlefield, the Islamic Republic has retaliated by bombing natural-gas plants across the region. Energy prices have soared. The price of Brent crude is around $100 a barrel (albeit jumping about), up from $60 at the start of the year. American petrol prices have risen (see chart 2).

Fortunately, these ructions would need to get much worse to provoke a global recession. Less happily, they will almost certainly further stoke popular anger over the cost of living.

At some point a rise in the cost of energy causes output to fall. Firms’ profit margins decline as they pay more for fuel and power. Consumers forced to fork out more for petrol cut discretionary spending. A recent study by Oxford Economics, a consultancy, reckons that two months of crude-oil prices at $140 (alongside higher natural-gas prices) would push parts of the global economy into a mild slump. A survey of economists by the Wall Street Journal suggests that $138 is America’s tipping point. Many economies seemed primed for a downturn even before the Middle Eastern chaos began. Consumer confidence is close to an all-time low in America and scarcely higher elsewhere.

Today’s shock is closer to touching a cattle prod than to a toaster in the bathtub

That scenario may be too gloomy. Research from Deutsche Bank shows that the change in oil prices matters, not just the level. America’s recession of 1973-75 was so deep because oil prices more than tripled in short order. So far in 2026 they have not even doubled. Steven Blitz of TS Lombard, a consultancy, points out that around the oil-induced GDP contraction of 1990, the price of West Texas Intermediate crude rose by 166%. To provoke a comparable shock today, it would need to hit $175. Today’s shock is closer to touching a cattle prod than to a toaster in the bathtub.

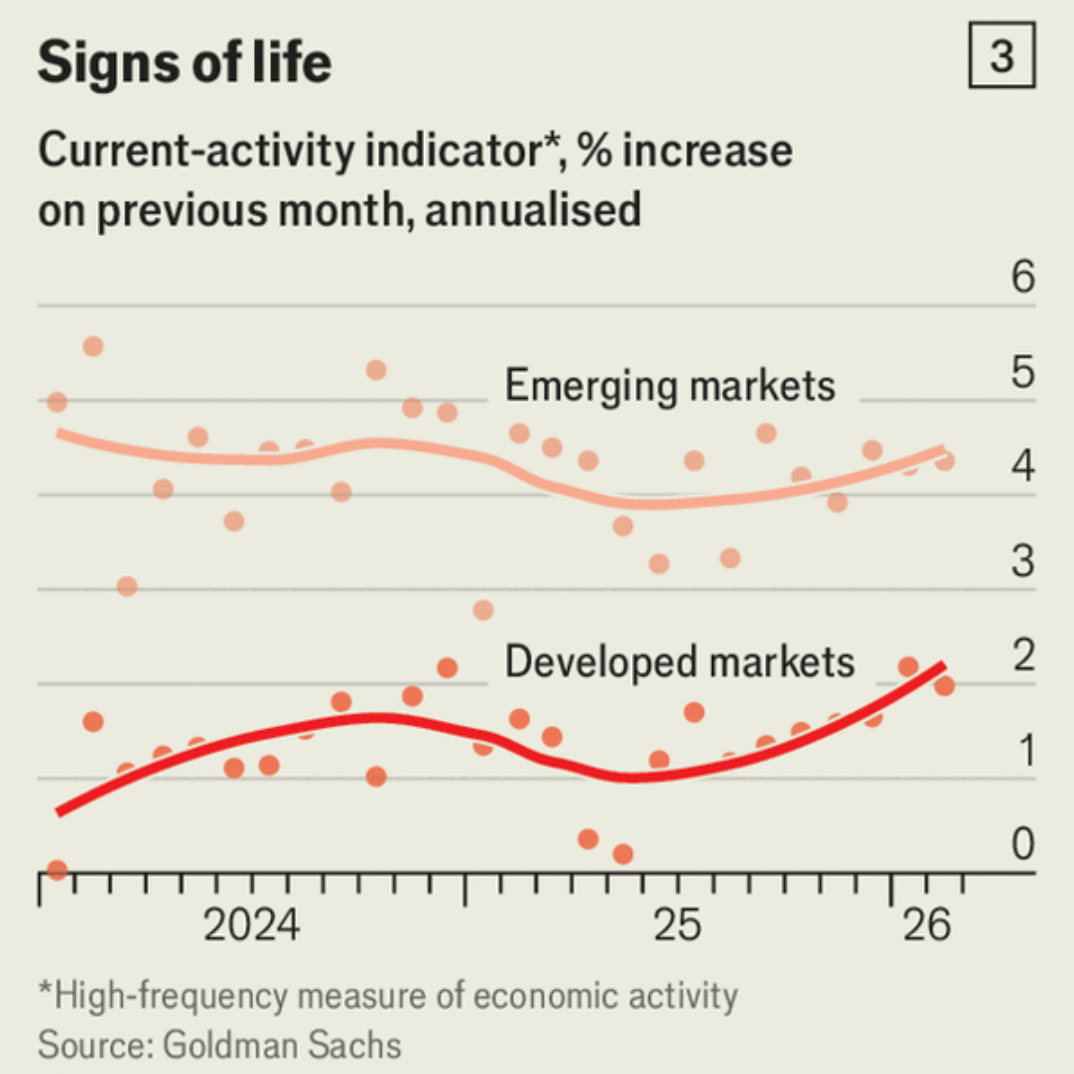

Moreover, the world economy came into the energy crisis in decent nick. Real wages across advanced economies are growing by at least 1% a year. In the fourth quarter of 2025 global corporate earnings rose by 15% in nominal terms, compared with a year earlier. A range of real-time data suggests that in recent months growth in the rich world has picked up (see chart 3). Despite the gyrations in energy markets, few investors are panicking about a recession. Measures produced by Goldman Sachs, a bank, which combine analysis of equities, foreign exchange and other assets, suggest that investors are pricing in a mild slowdown, not recession.

That same dataset, however, suggests that investors worry a great deal about inflation. Market-based measures of inflation expectations are shooting up. A rule of thumb says that a sustained $10 rise in oil prices eventually adds 0.3-0.4 percentage points to overall inflation. Assuming oil stays around $100 a barrel, the OECD’s average inflation rate might therefore rise above 4%; at $140, inflation of 5-6% is not out of the question.

More worrying, central banks might be less able to respond to an inflation shock than they were in 2022. Companies might be quicker to pass costs on to consumers this time than they were in 2022-23, having proved a few years ago that they can get away with raising prices. Central banks, meanwhile, might feel constrained in raising rates to combat any inflationary surge. Mr Trump would go ballistic if Kevin Warsh, his doveish pick to lead the Federal Reserve, started his tenure in a few months’ time by tightening monetary policy.

Though real-time data are not always reliable, they hint that the inflation scourge is stirring. Alternative Macro Signals, a consultancy, analyses millions of news articles. Their global inflation index, which has proved to be a useful predictor of official numbers, has recently risen sharply. If historical patterns hold, by July monthly global inflation could be above 0.6%. That is more than 7% on an annualised basis.

Alternative Macro Signals is not the only worrying datapoint. Truflation, a consultancy, analyses prices in real time from a wide variety of sources. Its figures suggest that this month American year-on-year goods inflation has jumped from less than 1% to nearly 3.5%. This was almost entirely the result of rising petrol prices.

If central banks will not nip another cost-of-living crisis in the bud, governments may feel forced to bail out citizens. In 2022-23 European governments allocated roughly 3-4% of GDP on average to reduce soaring energy costs facing households and businesses. The measures helped Europe’s poorest avoid severe deprivation. But they came at enormous fiscal cost. Perhaps half the spending was untargeted, so rich people—the biggest energy users who needed least help—benefited most.

Would governments pick more focused measures this time? At a time of populist anger and spendthrift politicians, do not bank on it. The longest-lasting economic consequence of war in the Middle East could be to compound the rich world’s fiscal woes.

© 2026 The Economist Newspaper Limited. All rights reserved.