Börsens oväntade vinnare och förlorare på oljerallyt

Oljeprisrallyt skapar vinnare och förlorare på aktiemarknaden – en del otippade och andra mer väntade namn. Snabbmatskedjan Chipotle, skojätten Nike och kryssningsbolaget Norwegian Cruise Line förknippas knappast med råvaran, men plågas alla av trenden.

Galopperande energipriser innebär en dubbelsmäll för många företag. Dyrare olja driver inte bara upp kostnaderna – konsumenterna håller också hårdare i plånboken, skriver The Economist.

The war’s biggest corporate winners and losers may surprise you

Markets are beginning to signal the long-term consequences of the surge in fuel prices

For many businesses, a jump in fuel prices is a one-two punch. First comes the rise in input and operating costs, which compresses profit margins. Then, before bosses have got their bearings, the second jab lands: their customers start penny-pinching. Nearly all households in America own a car; most own two or more. When petrol prices rise from around $3 a gallon to $4 they end up spending over $1,000 more per year on the fuel. For a typical household, that is an eighth of their discretionary spending—meaning money is diverted from things such as eating out, clothing and entertainment.

It has been almost a month since America first bombed Iran, killing Ali Khamenei, its supreme leader. At the start of 2026 oil prices were around $60 per barrel. In March they have swung wildly as the intensity of the conflict has gone up and down and on news about efforts to mitigate the impact, but have gyrated around $100. Consumers are already feeling the pinch: at the pump average petrol prices are $4, up from $3 at the end of February.

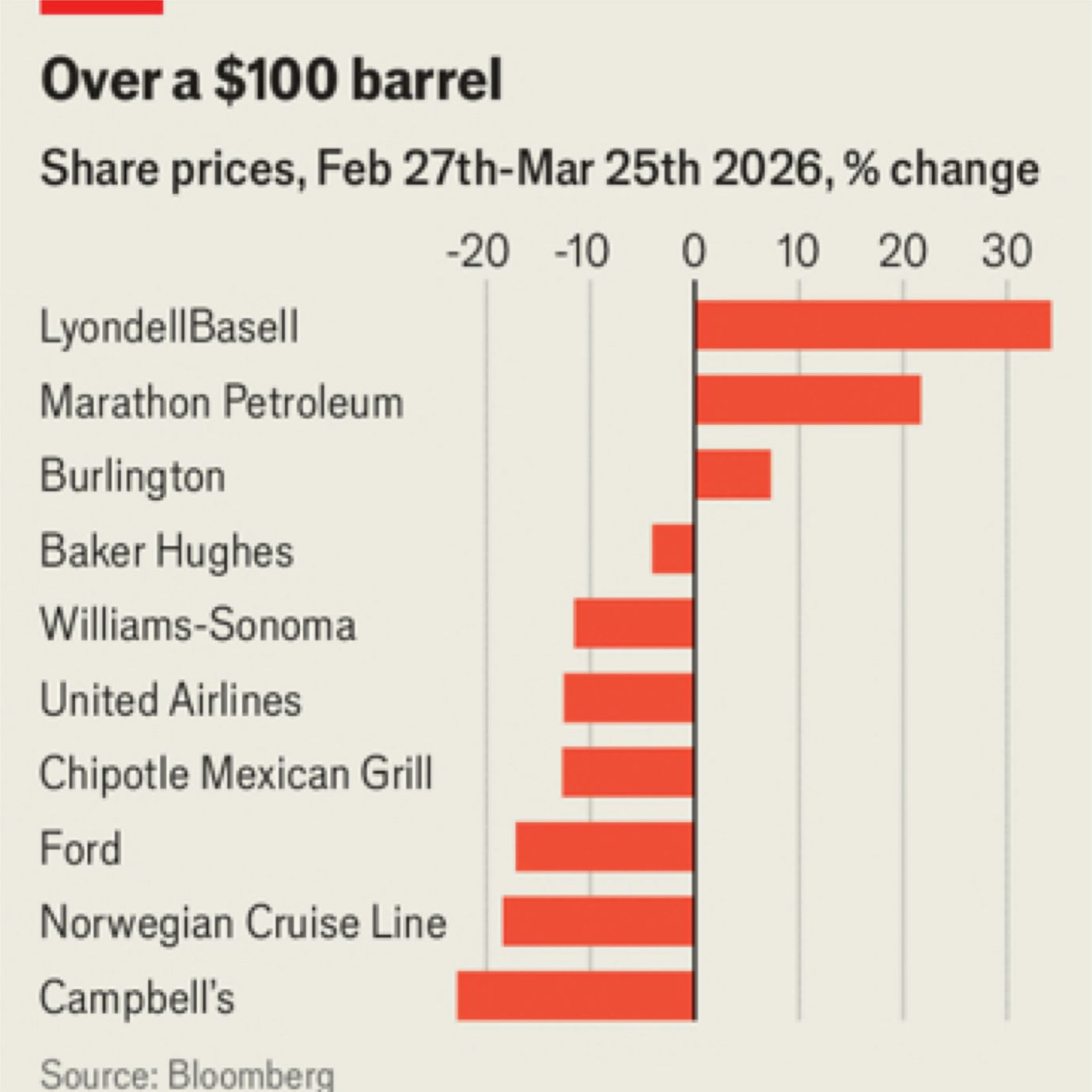

For American businesses, that creates winners and losers. Some are obvious. Higher prices are good news for the oil-and-gas sector, at least in the short term. Its listed companies have seen their share prices rally by an average of over 8% since February 27th. Airlines and cruise operators, by contrast, are suffering. Most carriers in America long ago abandoned hedging their fuel costs using futures contracts. The share price of American Airlines has slumped by 20% since the end of February, while that of United is down by 13% (Delta, which is more insulated because it owns a refinery in Pennsylvania that supplies three-quarters of its domestic fuel, has seen its share price rise by 3%). Firms that rely on discretionary spending including Chipotle, a fast-casual Mexican chain, Nike, a sportswear-maker, and Williams Sonoma, which sells posh kitchen equipment, have lost 12-15% of their value since the end of February.

Elsewhere, however, the impact is more surprising (see chart). You might think that companies which make chemicals from hydrocarbons would suffer because of higher costs for both energy and feedstock. Yet the share prices of LyondellBasell and Dow Chemicals, two of America’s biggest producers, are both up by around 30%. Unlike competitors abroad, they benefit from access to North America’s natural gas, which is now much cheaper than that elsewhere. CF Industries, a fertiliser manufacturer that uses that gas an input for ammonia, has likewise seen its share price surge.

Some pedlars of discretionary wares are also doing well. Burlington, a discount department store, is up by around 7% over the past month, as investors bet that shoppers will soon be hunting for bargains. At the same time, some companies making essential products are feeling the heat. Shares in packaged-food producers including Campbell’s and General Mills have tumbled by more than 20% since the war began. Investors reckon these companies, which jacked up prices during the previous inflation wave following Russia’s invasion of Ukraine in 2022, will be unable to repeat the trick this time. Many shoppers have already switched to private-label alternatives—which should help to offset any pressure on grocery-sellers such as Costco, Kroger and Walmart (whose shares are broadly flat).

On the whole, investors are expecting that companies will face higher costs and thriftier consumers. But what of the long-term consequences of the conflict? Here the signals are weaker, but worth paying attention to. Baker Hughes, which provides services and equipment to oil companies, would benefit if higher fuel prices led to a surge in investment. But, after swooning initially amid concerns over the impact on their projects in the Middle East, its shares are trading just below where they were before the crisis began, which may reflect doubts that production will rise much in response.

A lasting increase in fuel prices would have a big impact on carmakers. Ford and, to a lesser extent, General Motors have seen their share prices reverse since the war began. Partly that reflects the coming strain on would-be car-buyers. But it may also point to a less petrol-powered future. Shares in BYD, China’s electric-vehicle champion, are up by 15% since the start of the conflict; those of CATL, a big battery-maker, are up even more. The repeated oil shocks of the 1970s dealt a heavy blow to Detroit, as consumers turned away from gas-guzzlers and purchased fuel-efficient Japanese cars instead. For now, the course of the war remains unclear. But businesses should recognise that the repercussions will still be felt well after it ends. ■

© 2026 The Economist Newspaper Limited. All rights reserved.