USA backar Mileis krisande peso i oväntat drag

USA:s finansminister Scott Bessent gick i veckan ut med ett ovanligt tydligt stöd till den krisande argentinska valutan:

– Argentina är en systemviktig amerikansk allierad. Alla stabiliseringsalternativ ligger på bordet.

Uttalandet kom efter ett dramatiskt fall för peson, där Argentinas centralbank bränt en miljard dollar på två dagar för att försvara växelkursen.

Stödet ses som en livlina för president Javier Milei, vars reformagenda hotas av politiska bakslag, skriver The Economist.

Argentina’s finances just got even more surreal

Scott Bessent says Uncle Sam is underwriting Mr Milei’s laboratory.

On September 22nd, 15 minutes before Argentina’s foreign-exchange markets opened, America’s government made an intervention. “Argentina is a systemically important US ally,” Scott Bessent, America’s treasury secretary, wrote on X, a social network. He added that the United States “stands ready to do what is needed” and that “all options for stabilization are on the table.” “Argentina will be Great Again.”

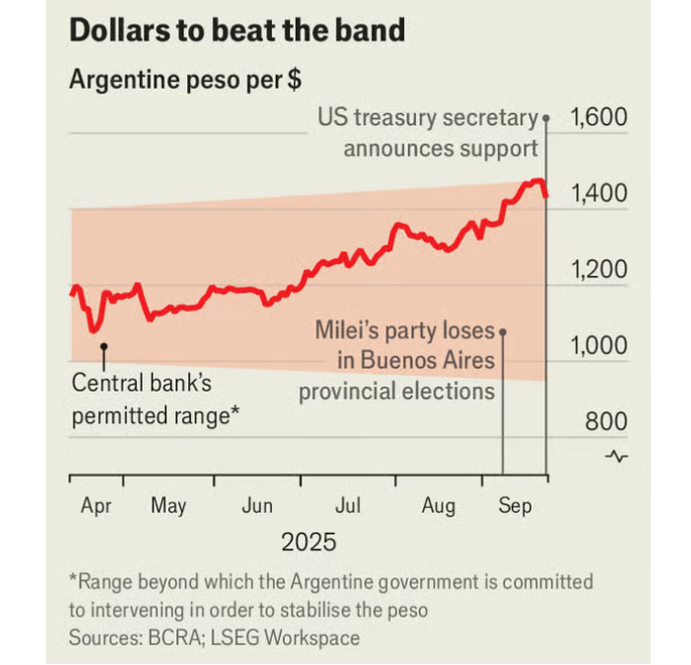

It is highly unusual for America to stand behind another country’s currency in this way. Mr Bessent’s declaration was prompted by intense and mounting pressure on the Argentine peso that threatens to derail the economic project of Javier Milei, Argentina’s libertarian president. Last month, with his sister embroiled in a corruption scandal, Mr Milei badly lost a legislative election in the province of Buenos Aires. He then suffered a series of stinging legislative losses. Markets panicked, worried that the defeat signalled the end of popular support for Mr Milei’s economic-reform project, and the potential return of spendthrift Peronists. A sharp peso sell-off began.

Since April, when the IMF launched yet another programme in Argentina, the peso has been floating within an exchange-rate band, the limits of which the Argentine government has vowed to defend. By mid-September the peso’s official rate was testing the upper limit of that band, even briefly piercing it on September 17th to reach 1475 to the dollar. Over the following two days the Argentine central bank spent some $1bn of its scarce foreign-currency reserves to defend the currency.

The bank does not have sufficient foreign reserves to keep up this level of spending for long. Drafting in the dollar-bazooka of the US Treasury should give Argentina the firepower to stabilise the peso, if needed. Mr Bessent, who went to Buenos Aires in April on his first official overseas trip, says the treasury is looking at “swap lines, direct currency purchases, and purchases of U.S. dollar-denominated government debt from Treasury’s Exchange Stabilization Fund”. The intent is to reassure markets that the band’s upper limit is backed by the might of the United States. Mr Bessent hopes the signal will be so powerful that the real extent of American support will never be tested. He promised more detail on September 23rd, when Mr Milei will meet with him and Donald Trump in New York.

Markets reacted to Mr Bessent’s statement with relief. (A big temporary tax break for agricultural exporters, which Mr Milei’s government announced earlier on September 22nd, and which should bring more dollars into the country, had already improved the mood.) Argentine bonds due in 2029, which had been in freefall, leapt by 6 cents to reach 71 cents on the dollar. The official peso had strengthened by about 4% as this story was published. Local Argentine stocks were up by about 6%.

That this calm will last is far from guaranteed. The details of the treasury’s support matter. “Anything less than $10bn in backing would look light to me,” says Martín Rapetti, an economist with Equilibra, a consultancy in Buenos Aires. Even with solid backing, difficult moments loom. The peso is now less overvalued than it has been for about 18 months. But Argentines will vote in midterm elections on October 26th. Many suspect that the government will have to change its exchange-rate scheme after the election, probably to allow the peso to float more freely. As a result, the week before the midterms is likely to be rocky, as markets try to anticipate the change. If the government’s polling is weak at that time, the pressure on the peso could be severe.

Buying time

Mr Milei’s political opponents smell blood. Congress has already succeeded in overturning his veto on one spending bill, and is in the process of overturning three more. That is a serious problem for the president, as market confidence in him rests on fiscal rectitude. His ability to control Congress, where he has few allies, has been predicated on his personal popularity. That this is now in question has fuelled investor alarm.

A poor showing in the midterms is not the only concern. Markets also worry that he will lose a re-election bid in 2027. Looming is the spectre of Axel Kicillof, the governor of Buenos Aires province, who emerged strengthened from the recent provincial elections and has presidential aspirations. His economic views are unorthodox, his record alarming.

Mr Milei’s problems are not due solely to political misfortune, though. His reform programme has relied heavily on a strong peso to contain inflation. His government’s interventions to prop up the currency, even after committing to a limited float, have long worried both voters and investors. Voters dislike the economic damage that is the inevitable side-effect of intervention. Many find that their wages buy less now than they did in early 2023. Investors first fretted that Mr Milei’s interventions meant he was failing to accumulate sufficient dollar reserves. Now they see his government burning through them, and wonder whether anything will be left to repay looming debts.

The support of the United States can buy Mr Milei time, but Argentine voters will determine his fate. The national electorate which will vote in October likes him better than do the voters in the Peronist heartland of Buenos Aires who kicked off this crisis. He has so few seats in Congress that any gains will be significant. Mr Bessent’s backing may well boost his flagging polling.

But if the midterms go badly, with markets concluding that Mr Milei has lost all control of Congress and that his re-election in 2027 is now a long shot, Mr Trump’s dollars will not save him.

© 2025 The Economist Newspaper Limited. All rights reserved.