Följ Buffetts råd – köp i rädslan efter ”Oraklets” exit

Berkshire Hathaways aktie har backat 10 procent sedan vd:n Warren Buffett – ”Oraklet från Omaha” – i maj meddelade att han lämnar över det operativa ansvaret till Greg Abel. Buffett stannar visserligen kvar som styrelseordförande under nästa år, men investerarna är ändå oroliga över strategin framåt.

Det är en onödig oro, enligt Barron’s.

”Det här skapar en möjlighet för investerare att följa hans råd om att köpa när andra är rädda.”

Berkshire Stock Is Losing Its Buffett Premium. Now Is the Time to Buy.

Shares have dropped 10% since the company’s annual meeting.

Berkshire Hathaway stock has been in a funk since the company’s May 3 annual meeting, when CEO Warren Buffett said he would step down as CEO at the end of the year. That has created an opportunity for investors to follow his advice to buy when others are fearful.

Shares of Berkshire have declined over 10% since the meeting, trailing the S&P 500 index by more than 20 percentage points after outperforming at the start of the year. Several factors are behind the flagging performance: an erosion in the “Buffett premium” ; concern that the property-and-casualty insurance cycle has peaked; scant new investment activity by the company; no stock buybacks in more than a year; and a recent shift away from defensive stocks like Berkshire.

Berkshire, though, still has a lot going for it. Its main businesses remain among the most dominant in their industries, while its stock portfolio still has a diverse mix of companies that could outperform if the market hits a speed bump. And it has a fortress balance sheet with over $330 billion in cash, a third of the company’s market value of $1 trillion, which could be used for buybacks, a dividend, and even a large deal—the purchase of railroad operator CSX is a real possibility.

“It’s getting to be more compelling now,” says Mac Sykes, a portfolio manager at Gamco Investors.

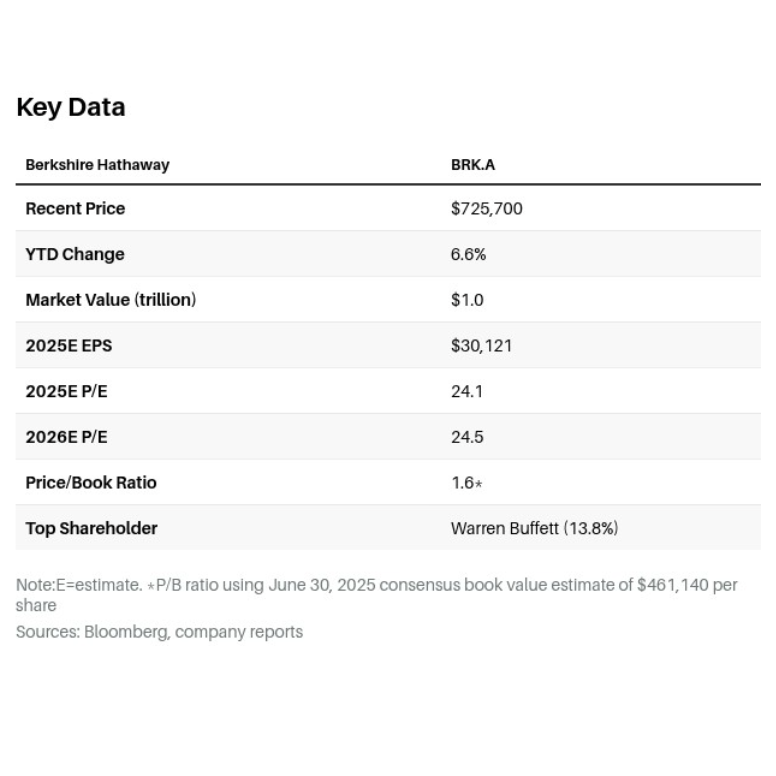

Berkshire’s shares are no bargain, but they look appealing in a richly valued stock market. The company’s Class A shares, at around $725,000, trade for less than 1.6 times the consensus estimate of the company’s June 30 book value of $461,140—in line with the average of recent years. The company’s Class B shares recently traded at $480.

”It’s getting to be more compelling now”

The stock trades for about 24 times projected 2025 earnings, in line with the S&P 500. Berkshire’s price/earnings ratio is even lower, at around 20, if earnings are adjusted upward to account for the profits of Berkshire’s equity portfolio companies, including Apple, Coca-Cola, and Bank of America. This non-GAAP measure, called look-through earnings, has been endorsed by Buffett.

Berkshire is generating about $45 billion in annual operating earnings. That should help lift book value to perhaps $525,000 per A share by the end of 2026, meaning the stock trades for a reasonable 1.4 times forward book value.

$525,000

Estimated book value per A share by the end of 2026, according to Barron’s.

“It’s a great stock to hold in this uncertain environment,” says UBS analyst Brian Meredith, who has a Buy rating and a price target of $892,120 on the A shares, up 23% from current levels. “Berkshire is no different than it was in April, before Buffett said he would step down.”

Buffett, 94, isn’t going away just yet— he plans to remain chairman in 2026. But no matter his role, the company’s three major businesses—insurance, railroads, and electric utilities—are in good shape.

Berkshire is one of the world’s largest property-and-casualty insurers, and while price increases have eased this year, they remain in the 4% to 5% range, auguring well for future results. It also owns Geico, the No. 3 auto insurer. Berkshire’s former insurance problem child, Geico has been largely fixed thanks to a technology overhaul and now is highly profitable and poised to grow.

Berkshire’s utility business is one of the biggest in the country and encompasses regulated electric utilities, a large renewable-energy portfolio, an electricity transmission network, and several natural-gas pipelines. Known as Berkshire Hathaway Energy, it’s deploying $10 billion a year of capital for a slew of projects and stands to benefit from the artificial-intelligence boom.

Berkshire’s Burlington Northern Santa Fe, together with rival Union Pacific, dominate freight railroads in the Western U.S. Union Pacific’s talks with Norfolk Southern

about a merger create the possibility that Berkshire would buy CSX, the other major Eastern railroad, and create a transcontinental railroad. Such a deal, which would face considerable regulatory scrutiny, could cost Berkshire $80 billion or more, assuming a 25% premium to the current CSX price, but be 8% accretive to Berkshire’s 2026 earnings, according to UBS’s Meredith.

”Investors are highly sensitive to the changing of the guard, and the Buffett premium is being extracted from the stock”

Berkshire’s other key asset—its $300 billion equity portfolio—is probably lagging behind the market this year, as gains in American Express, Bank of America, Coca-Cola, and Chevron are offset by losses in its largest holding, Apple, which is down almost 15%.

Still, it may take more than solid businesses and hopes for a bounce to get Berkshire stock moving again on its own. Buffett could help investors understand what management will look like after he steps down. Berkshire has said nothing about Greg Abel’s executive team once the head of Berkshire Hathaway Energy takes over as CEO, and it’s unclear whether Ajit Jain, the 73-year-old head of the insurance business, will stay on. The status of Todd Combs and Ted Weschler, who together run about 10% of Berkshire’s equity portfolio, is also unclear.

“Investors are highly sensitive to the changing of the guard, and the Buffett premium is being extracted from the stock,” CFRA analyst Cathy Seifert says. “The lack of clarity is not helping.”

A major acquisition, such as the aforementioned CSX or perhaps Occidental Petroleum, could do the trick. While Buffett says he doesn’t want to own all of Occidental—Berkshire now holds 27%—his successor, Abel, may see it differently, and Occidental CEO Vicki Hollub has said she would love the idea of being owned by Berkshire. Such a deal could cost $45 billion, well within Berkshire’s means.

Another possibility: Berkshire owns 27% of Kraft Heinz stock, and the big food company said in May that it’s considering strategic alternatives. Berkshire could swap its stock for the old Heinz business. Buffett, after all, is a big fan of Heinz ketchup.

A renewed share-repurchase plan would signal that Buffett views the stock as attractively priced, and it’s something the company hasn’t done since May 2024. It has been even longer since Abel, who owns $167 million worth of Berkshire shares, made a large personal stock purchase. His last buy came in March 2023, when the A shares traded around $450,000. Aligning himself more closely with shareholders would be a winning signal as he becomes CEO. Berkshire could even start paying a dividend—given its cash and earnings, it can afford a 2% payout—like most companies its size.

With so many levers left to pull, don’t count Berkshire out yet.