Fynda Expedia när Uber sneglar på uppköp

Efter ett turbulent år ser det bättre ut på flera fronter för resebokaren Expedia, som bland annat driver Hotels.com. Det tycks ha gått marknaden förbi att nya vd:n genomfört flera positiva förändringar och att bolaget kommit starkare ur pandemin. Expedias värdering är anmärkningsvärt låg jämfört med rivalen Booking, noterar Barron’s som plockar fram köpstämpeln.

Ytterligare en krydda är att Uber uppges överväga att lägga ett bud på företaget i sin ambition att bygga en superapp för resor.

Expedia Is Ready to Catch Booking. Why It’s Time to Buy the Travel Stock.

The online travel agent has gotten more efficient even while trading at half the multiple of its competitor.

Although it has had a rough year, Expedia Group could be an investor’s ticket to paradise. A report that Uber Technologies has looked into purchasing the online travel agent only makes the case stronger.

Expedia , whose bread and butter is matching people with empty hotel rooms, has made something of a round trip in 2024: The stock crashed in early February following mixed quarterly results, lackluster guidance, and the departure of CEO Peter Kern. While Kern had led the company through the tumultuous pandemic period, investors grew impatient as they waited for his transformative strategy to unfold.

The results looked even worse when compared with Priceline owner Booking Holdings , which has returned 20% annually over the past three years to Expedia’s annual loss of 4.2%. Only recently has Expedia stock climbed back to where it started the year.

Signs of improvement under new CEO Ariane Gorin are already visible, with the company targeting increased market share for its Expedia, Hotels.com, and VRBO brands, says Naveen Jayasundaram, a senior analyst at ClearBridge Investments, as well as improvements in efficiency and sales growth. Its overhaul puts it in position to play an impressive game of catch-up with Booking. “Expedia is a business in the midst of a turnaround,” Jayasundaram says. “There are early signs of progress.”

In recent months, Uber has discussed a potential bid for Expedia, according to the Financial Times . Uber CEO Dara Khosrowshahi was previously the CEO of Expedia and remains on its board.

Expedia, of course, rises and falls with travel spending. Though travel demand is down from the immediate postpandemic frenzy, it’s still at remarkably high levels. Domestic and international air traffic in the first half of the year was back in line with 2019 levels, and nearly five million more people will set sail on cruises in 2024 than they did in the year before the pandemic.

While bears worry that hotels, unhappy about forking over a percentage of profits to other sites, could fight back, as airlines have done in the past, the vast majority of hotels are owned by small operators that don’t have the same clout. Tech behemoths aren’t a big worry, either. While investors have fretted that Google parent Alphabet will use its considerable resources to muscle out smaller online travel services, it hasn’t been able to crush its rivals.

“The more fragmented the industry is, the harder it’s going to be for [competitors], even Google,” says Christopher Conway, a senior portfolio manager at GYL Financial Synergies.

”There isn’t going to be just one winner here”

The new travel normal has also brought more novice users online looking for hotel and airfare bargains. They are less likely to be brand loyal and intent on booking directly with providers, and tend to turn to online travel agents as a one-stop shop. Increasingly, that means Booking and Expedia, which enjoy a near duopoly, controlling roughly 42% of global bookings, according to travel industry firm Skift.

“There isn’t going to be just one winner here,” says Jay Aston Jr., a portfolio manager on Neuberger Berman’s global equity megatrends team. “Booking does a good job, but Expedia has a pretty fantastic platform.”

And one that has gotten better. As painful as the pandemic was for online travel agents—and the industry as a whole—it allowed Expedia to rapidly integrate the numerous brands it had acquired in the prepandemic years into a more streamlined platform, giving it a chance to maximize the value of its data and capture the benefits of scale. Those changes have helped it generate $1.3 billion in free cash flow in the most recent quarter, up 42% from the year-ago period, leaving the stock trading at 8.4 times free-cash-flow estimates for the next 12 months, about half Booking’s 16.2 times and a third of the S&P 500 index’s 25.6 times.

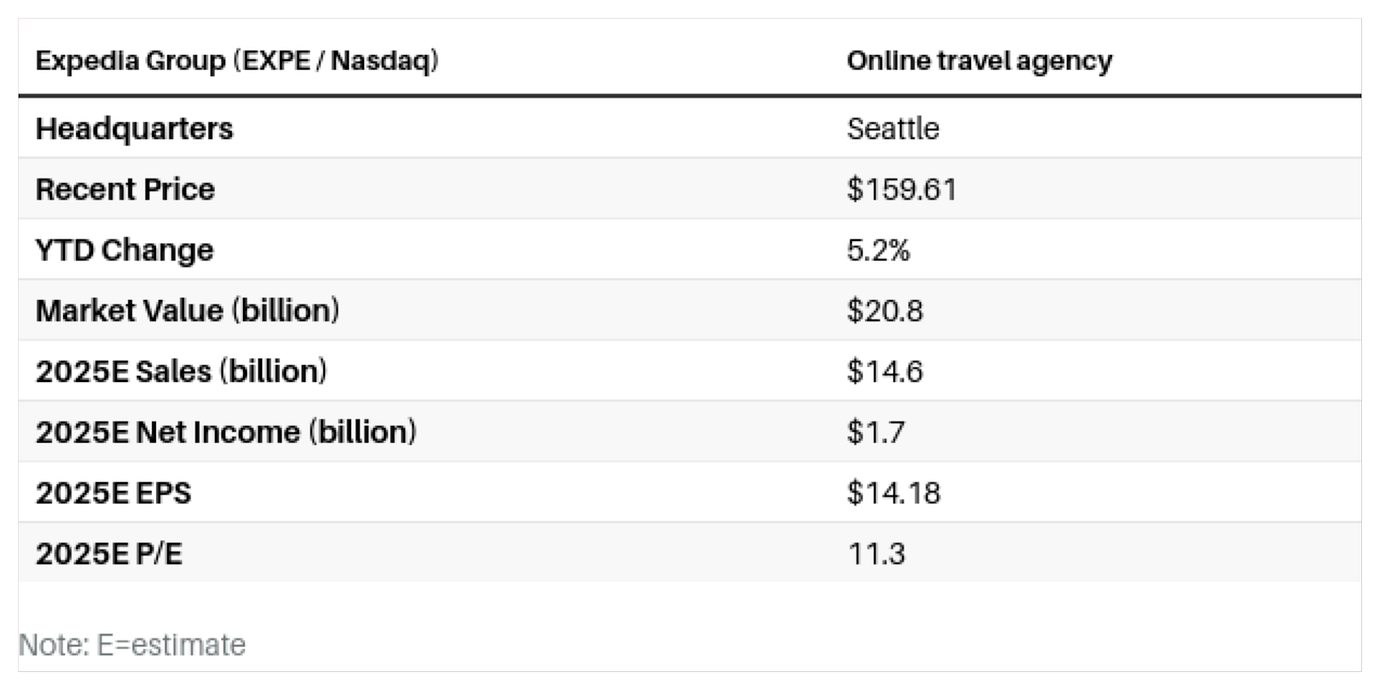

Key Data

“A more unified platform will allow Expedia to generate significantly more meaningful cash flow, and there’s a lot more operating leverage to come,” says Aston. “If you look at free cash flow, it’s wildly undervalued.”

And not just on free cash flow. Expedia trades for just 11 times forward earnings, half of Booking’s 22 times—simply too cheap for what Dan Ahrens, managing director and portfolio manager at AdvisorShares, calls a “blue-chip travel stock.”

And it isn’t for a lack of growth. Analysts predict earnings per share to climb 21.5% this year, to $11.78, and another 20% in 2025, to $14.18—and on about 7% revenue growth for each year. Earnings will get a boost from VRBO, which showed a promising rebound in the second quarter as it benefits from the company’s recently launched One Key loyalty program. In addition, Expedia’s business-to-business division, in which other travel players fulfill their orders through Expedia’s inventory, has also been growing. The company will report third-quarter results on Nov. 7, when it will have another chance to show that its initiatives are working.

“Expedia is probably interesting here, relative to Booking, since the valuation is more attractive—we like that,” says Randy Hare, director of equity research at Huntington National Bank. “Their estimates seem doable…we could see decent growth and upward movement.”

Sure, it may still not be cheap to book a vacation, but at least Expedia looks like a bargain.