Revanschläge i UPS som inte alls levererat på börsen

Transportjätten UPS försök att förbättra sina marginaler imponerar inte på Wall Street. Fjolårets vinstras och fallande omsättning har tryckt ner aktiekursen. Framåt ser det fortsatt tufft ut för intjäningen, men åtminstone vinsterna verkar ha bottnat.

Det bör snart ge resultat på börsen och i väntan på det får investerare en fin direktavkastning på drygt 4 procent, skriver Barron’s i en köprekommendation.

UPS Stock Failed to Deliver in 2023. Now It’s Time to Buy.

UPS stock looks attractive after a selloff as the package-delivery leader works to cut costs and boost profits. Investors reap a 4.4% dividend yield while waiting for the rebound.

United Parcel Service is set to bring investors better returns.

The leading package-delivery service is seeking to cut costs, increase automation, boost margins, and lift volumes to offset higher expenses from a headline-grabbing contract with the Teamsters union last summer.

Wall Street isn’t won over. UPS stock has come under pressure, falling 7% since the company offered disappointing 2024 guidance in conjunction with its fourth-quarter earnings report at the end of January.

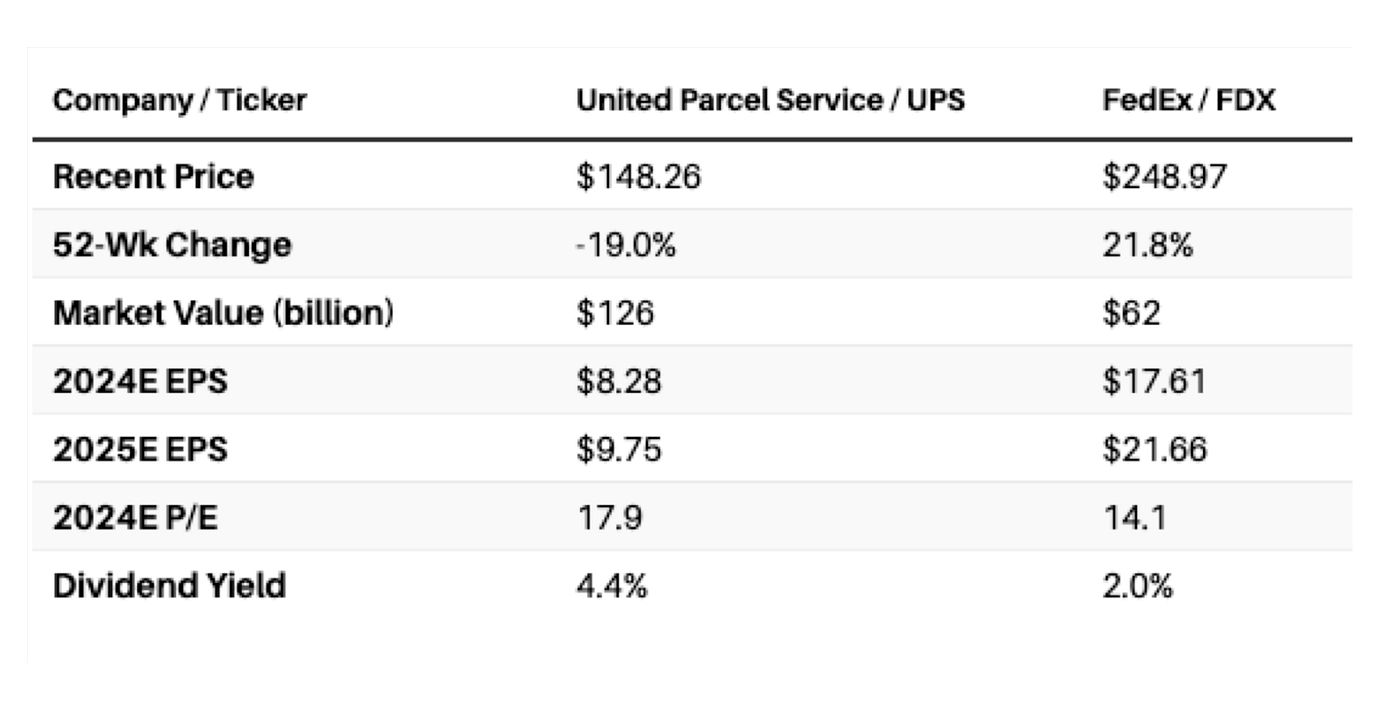

With the selloff, the stock, now around $148, looks appealing. The valuation isn’t cheap, at 18 times projected 2024 earnings of $8.28 a share. But this year looks like an earnings trough as UPS absorbs nearly half the cost of the front-end loaded Teamsters contract that covers about 70% of its 500,000 workers. Wall Street sees about $10 a share in earnings next year and $11 a share in 2026.

UPS offers a 4.4% dividend yield, highest among the 20 companies in the Dow Jones Transportation average.

While dividend coverage this year is tight, with projected free cash flow roughly equaling dividend payments, Chief Executive Carol Tome said on the January earnings call that UPS is “rock solid” and that she’s “confident” about the dividend

She noted that the company boosted the quarterly payout by a penny in early 2024 to $1.63 a share. And the company bought back over $2 billion in stock last year. UPS is valued at $126 billion and carries modest net debt of $15 billion.

“Everything good that management said will happen will occur but investors may have to wait a little longer,” says David King, lead manager of the Columbia Flexible Capital Income fund, which holds the shares.

“The company is coming off a challenging 2023, and we have confidence that management can execute against a cost-focused program to drive margin expansion and upside in the stock,” says Tom Wadewitz, a UBS analyst who upgraded the stock to Buy from Neutral a month ago. He has a price target of $175.

A more bullish King sees the potential for $15 a share in earnings per share in a few years and he thinks the stock can top $200.

UPS is a leader in domestic packages, delivering an average of 16 million a day. The company also has a sizable international business—mostly small packages—and a large “supply-chain solutions” business that involves freight forwarding and logistics.

Missed Delivery

UPS benefits from a more integrated domestic network than rival FedEx .

UPS is coming off a tough 2023, when revenue fell 9% to $91 billion and adjusted earnings dropped 32% to $8.78 a share. The company underestimated the negative effect on volumes from negotiations with the Teamsters, prompting shippers to shift business over fears of a strike, which was averted with the summer settlement.

Some of the shine has come off CEO Tome. She was hired as UPS’ CEO from a top finance job at Home Depot in 2020, a break from the corporate lifers who had historically run the 117-year old company. Tome, 67, emphasized profits over volume; her phrase was “better, not bigger.” More recently, the company has sought to rebuild sales volume. The stock doubled from early 2020 to early 2022 but has since given half of that back.

The revenue outlook for 2024 isn’t great. UPS sees sales of around $93 billion this year, up 2% from 2023, and projects that domestic package volume will rise 1% in 2024. Profit and margin improvement will be weighted to the second half of 2024, the company has said.

The near-term bull case involves costs, and analysts see a potential catalyst in the company’s investor day on March 26.

Baird analyst Garrett Holland upgraded UPS in mid-February to Outperform from Market perform, citing “longer-term cost savings and productivity opportunities.”

”Everything good that management said will happen will occur but investors may have to wait a little longer”

On its January earnings call, UPS management talked about achieving $1 billion in annual cost savings from reducing management ranks by 12,000, and Holland sees the potential for another $1 billion in annual savings from reducing nonunion labor and consolidating facilities. Each billion dollars of savings is worth nearly $1 a share.

These initiatives could offset the contract with the Teamsters, which many viewed as a victory for a more-aggressive labor movement.

Union leadership called it a win. Full- and part-time employees got an immediate pay increase of $2.75 an hour, which will rise to a total of $7.50 an hour over the five-year contract. The highest-paid delivery drivers will earn $49 by the end of the contract in 2028, and UPS said the average full-time driver would earn $170,000 in pay and benefits at that time.

The company pushed back against critics who said it caved to the union, noting that the average annual wage cost of the Teamsters contract is a manageable 3.5% over five years, and that there aren’t restrictions on the company’s use of technology and automation to reduce costs.

A unionized workforce does mean that UPS has higher labor costs than rivals such as FedEx, which uses nonunion labor in its ground operations.

But UPS drivers are productive, motivated, and popular with the public. The company views them as brand ambassadors.

Many are also owners. UPS workers—active and retired—effectively control the company through a class of supervoting A shares. The publicly traded B shares represent about 85% of the total shares outstanding. The supervoting shares, meanwhile, make it harder for an activist to target the company.

The UPS negatives are that it’s a capital-intensive, economically sensitive, unionized company that faces competition from lower-cost delivery enterprises, including Amazon.com .

But the company remains a dominant player in package delivery and a vital piece of the economy, with plenty of opportunities to cut costs and boost margins.

Profits appear to have bottomed. And investors get a 4%-plus yield while they wait for improvements to take hold.

If management were ever open to a sale, Berkshire Hathaway likely would be interested, Columbia’s King says. CEO Warren Buffett has long sought what he calls an elephant-size acquisition—and UPS is a big, high-quality, U.S.-oriented company that could fit that bill.