Dragkamp om vinsten mellan universitet och grundare i Storbritannien

Brittiska universitet spenderar miljarder årligen för att omvandla forskning till framgångsrika företag; enligt konsultfirman Beauhurst handlar det om en femfaldig ökning de senaste tio åren. Ett exempel på en avknoppning från Oxford är Vaccitech som äger teknologin i AstraZenecas Covid-vaccin.

Trots det ökande intresset från både universiteten och den brittiska regeringen höjs kritiska röster från forskarna som blivit företagare. De menar att universiteten kräver en för stor del av kakan och jämför med USA, där de tar betydligt mindre.

The growing tensions around spinouts at British universities

Millions of pounds are being invested to turn scientific research into global companies. But some founders say they have to give up too much equity.

When Bo Jing signed up for a PhD at the University of Oxford a decade ago, he did not intend to become an entrepreneur. He certainly did not expect to end up in a legal battle with one of the world’s most esteemed academic institutions.

Yet the 37-year-old is today at odds with Oxford after the company it set up to develop academic research into intellectual property sued his biotech start-up Oxford Nanoimaging for more than £700,000. The dispute, over Jing’s refusal to pay what he deems unfair royalties to the university, could become a landmark case for similar businesses, especially at a time when UK universities are ramping up investment into the commercialisation of ideas cultivated on their campuses.

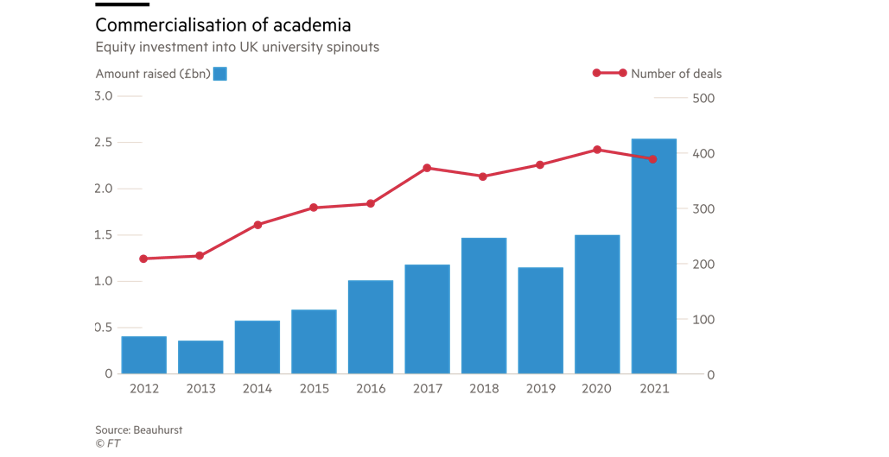

According to consultancy Beauhurst, equity investment in university spinouts increased more than fivefold in the decade to 2021, from £405mn to £2.54bn. Universities are spending millions of pounds annually on incubating spinout companies, licensing technology and training academics to become entrepreneurs. These efforts, advocates say, will bring cutting-edge research down from ivory towers and solve global problems, as well as jump-starting economic growth. It is also a part of the British government’s vision to turn the UK into a science superpower.

In the last decade, Oxford has led the UK-wide drive to turn cutting-edge research into commercial success. Oxford University Innovation (OUI), a subsidiary technology transfer office devoted to helping academics commercialise their work, formed 31 new companies and generated £25.1mn in revenue in 2021.

Spinouts include Vaccitech, which owns technology underlying AstraZeneca’s Covid-19 vaccine; ORCA, which supplied the Ministry of Defence with its first quantum computer; and First Light Fusion, a company working on creating clean energy from combining atomic nuclei. Some companies receive funding from the university’s own investment vehicle, Oxford Science Enterprises (OSE), which holds assets of more than £1bn.

“People are now looking to universities to come up with global solutions to big global problems,” says Chas Bountra, the university’s pro-vice chancellor for innovation, and an evangelist for commercialisation. Scaling up research into companies is among the best ways to do it, he says. “If we created a trillion-dollar company, I would not worry about the economy of this country then. The impact would just be enormous.”

“People are now looking to universities to come up with global solutions to big global problems”

However, Jing’s dispute with Oxford is one sign of the growing tensions around spinouts — and the relationship between academic-entrepreneurs and their universities.

Some founders and investors say universities are benefiting unfairly from the work of the entrepreneurs. They argue the spinout ecosystems are doing little to help — or worse hindering — the release of technology that could benefit all of humanity.

Nathan Benaich, the founder of venture capital firm Air Street Capital, believes that university tech transfer offices are “more of a hindrance than a help” and are too greedy to keep a share in new companies. Fearful of letting a “golden goose fly away” they end up losing more by obstructing the company’s success. “There’s too much focus on value capture.”

Role of the founder

When Jing arrived at the lab run by Achillefs Kapanidis, a professor of biological physics, in 2013, he joined a project that already aimed to bring a product to market, and make a difference to the world.

Three years earlier, according to court documents, Kapanidis and his team had started a project to “develop a compact microscope” using a technique called single molecule fluorescence. It had already secured funding and teamed up with a commercial partner.

In the years that followed, however, Jing was instrumental in turning that nascent technology into a shoebox-sized microscope capable of observing tiny processes happening in cells in real time. In 2016, he spun out Oxford Nanoimaging with Kapanidis, and later became chief executive. Last year, Jing led the company to close a $75mn Series B funding round.

The association with Oxford university, however, came with a price. Like most technology transfer offices, OUI retains an equity stake in the companies that spin out from it, as well as licensing rights over some of the intellectual property the company is based on.

The university jointly retained a 50 per cent stake, against 25 each for Jing and Kapanidis, although that stake had been significantly diluted by the time of trial as investors piled in. Oxford also holds a licensing agreement that dictates OUI is entitled to a sliding royalty of 3.5 per cent to 6 per cent of ONI’s net sales. But since 2019, Jing refused to pay.

“If you have any context of what a co-founder does in a start-up it’s literally hell . . . ”

The stand-off came to the patents court with a royalty claim by Oxford in 2021. Jing says he took a stand to free his company from what he says is an excessive financial burden that was stopping it flourishing, and to push for fairer terms for entrepreneurs like him. He argues that universities tend to “overestimate” their impact on spinouts, and contribute little compared to the years of grinding work put in at later stages.

“They see themselves as this entitled entity that should be treated as a co-founder,” Jing says from San Diego, where he moved the company. “If you have any context of what a co-founder does in a start-up it’s literally hell . . . the university has nothing to do with that.”

[Universities] see themselves as this entitled entity that should be treated as a co-founder

But in a ruling published in December 2022, Daniel Alexander KC took a different view and said more was at stake: a fundamental challenge to OUI’s right to Jing’s inventions.

In his judgment, Alexander recognised Jing had contributed the “majority” of work in the redesign of existing research, but “was not working completely alone and his work built on that of others”.

He ruled in favour of OUI, concluding that it was properly entitled to claim rights under the licence, and that Jing should pay the money he owed. The young, gifted scientist, he wrote, had developed a “rigid” view that he and other entrepreneurs had been unfairly treated by Oxford, and viewed himself as the “saviour” of the project, downplaying the role of others.

“I think he also had a characteristic, sometimes exhibited by clever and self-confident people, namely something of a blind spot when it comes to recognising the extent to which their success was built on the foundations — and sometimes failures — of others,” Alexander wrote.

He backed up Oxford’s contention that it had acted fairly in retaining the stake it did in the company, given its taxpayer-funded and charitable status, its early involvement in the business and wider commitment to helping scientific advancement. In a statement, the university said it “will continue to support researchers, staff, investors, and other important partners in the Oxford University innovation ecosystem to deliver the greatest possible impact and societal benefit.”

Value of a support system

Imperial College London’s White City site is a glossy campus of basement laboratories, breakout rooms and open-plan offices. It is home to the new Institute for Deep Tech Entrepreneurship, which opened in 2022 to offer guidance and early-stage funding to 10-15 cutting edge research projects each year.

Professor Ramana Nanda, who heads the institute, believes solutions to crises such as child hunger or climate change exist but are stuck at universities. The “grand challenge”, he says, is getting them out into the real world.

“It’s very hard for commercial investors to come digging inside universities,” adds Nanda. The institute’s job, he says, is to be a “support system”: cultivating links with founders, helping companies get the proofs of concept and funding research at its very early stages.

This work is not restricted to the Golden Triangle, a cluster of research-intensive universities in London, Oxford and Cambridge that have long attracted the lion’s share of research and development funding.

In 2021, Leeds, Manchester and Sheffield universities launched Northern Gritstone, an investment vehicle focused on their spinouts, which last year closed a £215mn funding round. Its chief executive, Duncan Johnson, hopes the money will turn the region into an innovation hub rivalling Silicon Valley.

Before the investment vehicle even thinks about funding nascent companies, however, the university has already been working with them for some time. Luke Georghiou, deputy vice-chancellor at Manchester, estimates the university spends about £5mn annually on “intellectual property services”, mostly based at its Innovation Factory.

It is here where a team identifies cutting-edge ideas, coaches academics, links researchers with management teams and funders, and carries out due diligence and patenting. “We’ve always been the ones who support the very early stages,” Georghiou says. “It’s normally the hardest part of the system.” Some 150 research ideas a year typically get support. About 10 per cent of those will ultimately spin out.

Alice Frost, director of knowledge exchange at UK Research and Innovation, the funding body, says universities such as Manchester are investing in research possibilities that many venture capital firms would not touch.

One role of tech transfer offices, she says, is to build networks of investors that are able to make early-stage, long-term investments in cutting-edge technology, often known as “patient capital”.

“Universities at their most academic are at their most commercial”

But they also provide space that is isolated from commercial interests where truly groundbreaking ideas can develop. “It’s a weird conundrum,” Frost says. “Universities at their most academic are at their most commercial.”

Like Oxford, Manchester seeks to cover the costs of this work by bringing some of the revenue of successful companies back into the system, through licensing or retaining equity stakes in spun-out companies.

According to Beauhurst, Manchester retains an average of 32 per cent which is diluted as more investors become involved. The stake is higher than the average 24 per cent recorded by the consultancy. Across the sector, founders retain an average 54 per cent.

Last year, Oxford changed its equity policy, dropping its standard cut from 50 per cent to 20 per cent. The University of Cambridge required an average 12.6 per cent. But both still demand much more — in the first instance — than most US universities: Berkeley in California, for example, states that it will not generally take more than 10 per cent.

Universities’ mission to spinout research is driven too by government policy. Prime Minister Rishi Sunak has pledged to make the UK a science superpower in part by boosting funding for research and development.

But something is awry. According to Beauhurst, university spinouts represent just 3 per cent of the UK’s high-growth companies, and 0.03 per cent of all companies in total.

Specialists such as Sir John Bell, the Oxford university medicine professor who helped develop the Covid-19 vaccine, bemoan the absence of Boston-level life science clusters. While the UK performs strongly on spinouts, it has failed to scale these new companies to the size of market leaders in the US.

Some founders agree. In a database of dozens of testimonies collected by Benaich, they tell stories of “egregious” equity expectations torpedoing funding rounds. Others describe “painful” spinning-out processes that took years.

Richard Murray, the chief executive of Oxford quantum spinout ORCA, credits the university as being “supportive” in its success. But high equity stakes retained by the university put founders at a disadvantage, he says, especially in the US where investors believe founders are better motivated if they hold the equity themselves.

”We need to keep investing in the health of the whole system”

Spinouts in the UK are also dealing with more immediate challenges. In and beyond the Golden Triangle, entrepreneurs say their growth is stymied by a lack of lab space and shortages of talented people. While frustration with the spinout process was part of his decision, Jing, of Oxford Nanoimaging, ultimately moved his company to San Diego in search of highly skilled recruits, which he says he could not find in the UK.

The absence of “scale up” capital, to bridge the gap between early-stage investment and support for companies becoming more established, is also a problem.

Tomas Coates Ulrichsen, a University of Cambridge researcher who last year authored a report into equity stakes, says tackling these problems requires money — and it is universities that shoulder the cost.

Debate at the top of government has been “driven by investor perspective” but the reality is “much more complicated”, he adds. “It costs money to put in infrastructure to help academics develop spin out companies . . . We need to keep investing in the health of the whole system.”

Wholesale reform

Last week, Jing was refused an initial attempt to appeal the outcome of the case against him, and ordered to pay more than £2mn in continuing royalties, interest and legal fees. Undeterred, he plans to turn to the Court of Appeal to challenge the decision.

As chief executive of Oxford Nanoimaging, he wants to free the company from the “financial burden” of royalties. He hopes a decision in the judgement that PhD students should be treated as consumers will support his case that universities have to offer them fairer terms. But the case is also a more ambitious attempt to challenge what Jing sees as unfair practices towards spinout founders: “We want better treatment of entrepreneurs full stop.”

Jing and Benaich, of Air Street Capital, are part of a vocal contingent of founders and investors calling for wholesale reform of the system. A spinout playbook, written by Benaich, recommends universities retain lower stakes in fledgling companies, and suggests government targets for the number of companies tech transfer offices spin out, and legislate for standard terms, he adds.

Murmurs in Westminster suggest some of these ideas are gaining traction. People close to discussions say that the government is considering reform of spinout terms as part of its economic vision in which science and technology has a starring role.

“We’d kill the goose that lays the golden egg”

Requiring universities offer a broader range of equity options, including one with lower stakes, is one idea being mooted in a Labour party plan to support small businesses. Advocates say if the university takes less it will gain more long term, as spinout companies thrive.

But across the sector, some are nervous about potential changes.

Although the government has committed to increase public investment in research and development funding to £20bn annually by 2024-25, a deadlock over UK involvement in Horizon Europe, an EU-wide research and innovation programme that has a budget of €95.5bn, means many projects face an uncertain future.

A long-term freeze in tuition fee income from UK students is also straining the overall finances of higher education. As the UK government seeks to cut its debt levels, it is not clear where the funding for the university ecosystems that germinate these companies will come from.

“The overall big picture is that research operates at a deficit,” Georghiou says. He fears a change in policy would direct more funding into the pockets of investors, while the universities that generate the research and nurture companies continue to struggle. “We’d kill the goose that lays the golden egg.”

©The Financial Times Limited 2023. All Rights Reserved. FT and Financial Times are trademarks of the Financial Times Ltd. Not to be redistributed, copied or modified in any way.