Hollywoods jätte har många problem – inte ens Barbie kan lösa dem

Det är en svår tid för Hollywood och tv-industrin. Publiken går inte på bio så ofta längre och kabel-tv har ersatts av Netflix, Youtube och Tiktok. Inte ens succéer som Barbiefilmen kan lösa utmaningarna som den gamla underhållningsgiganten Warner Bros Discovery står inför, skriver Barron’s i ett långt reportage.

Inom bolaget har man länge skojat om att Warner är bra för de anställda och inte fullt så bra för ägarna. Det är en sanning som reflekterats i aktiekursen under det senaste dryga decenniet. Detta stämmer också väl in på bolagets legendariska vd, David Zaslav, vars årsinkomst har legat i snitt på 55 miljoner dollar de senaste 15 åren.

Men ägarnas hopp är att Zaslav ska lyckas vända utvecklingen och i så fall kan aktien, som varit pressad länge, ha stor uppsida.

Warner Bros. Discovery Has Big Challenges. The Barbie Movie Won’t Solve Them.

The Warner Bros. Discovery CEO has a big salary and a big task at the parent company for CNN and Max: turning around a media giant saddled with high debt and multiple challenges

You may have read about Warner Bros. Discovery and its high-profile CEO, David Zaslav. Often lost or overlooked are the things that matter most to investors. How is the embattled media conglomerate organized, and how can it grow? Can it service its massive debt? Is it a good investment, and what are we to make of Zaslav’s prodigious compensation?

Warner Bros. Discovery (ticker: WBD) isn’t some sort of industrial-fastener manufacturer, of course. With properties like its legendary movie studio, TV networks including CNN, and Max (the streaming service that houses HBO), Warner Bros. Discovery is the highest of high-profile companies—and for much of its 17-month existence, not in such a good way.

The product of a motivated seller—AT&T (T) was determined to offload WarnerMedia—and a motivated buyer, with Discovery keen on untethering its destiny from the declining linear-TV business, Warner Bros. Discovery was birthed into a roiling media landscape with grand ambitions and a ton of debt. Zaslav’s remit is challenging, to say the least.

Zaslav, or Zas, as he is known in the industry, has also become a bit of a lightning rod. There’s the “outrage” of Zas partying with movie stars at the Cannes Film Festival (an ambitious guy romances Hollywood—imagine that), Steven Spielberg’s public upset over job cuts at Turner Classic Movies, and Zaslav’s role in the psychodrama that is CNN—now perhaps calmed with the appointment this past Wednesday of veteran news executive Mark Thompson as its CEO.

Yes, it’s a difficult time for Hollywood and the TV business. Audiences aren’t going to movie theaters so much, and they’re cutting their cable subscriptions and instead watching Netflix, YouTube, and TikTok—newer companies that are spending tens of billions of dollars building market share and disrupting incumbents like WBD.

It’s also true, though, that people still want to watch movies like Barbie, shows like Succession, and sporting events like college basketball’s March Madness, which all happen to be Warner Bros. Discovery content (or licensed by WBD, in the case of the last). The question for Zaslav is, what’s a sustainable business model to deliver all of this content?

Discovery was founded 38 years ago, shortly after which Tele-Communications, a company controlled by billionaire John Malone, who would become a mentor to Zaslav, bought a big stake. Zaslav, who previously worked at NBC, was named CEO of Discovery in 2006 and took the company public two years later. Zas—who “always plays offense,” according to company veteran J.B. Perrette, now WBD’s top streaming executive—deserves credit for growing Discovery revenue nearly 10 times from its initial public offering in 2008, to $33.8 billion in 2022.

Zaslav achieved this early on, in part by replacing Discovery’s sleepy nature documentaries with unscripted, low-budget, lowbrow content like Shark Week, Naked and Afraid, and Dirty Jobs.

In 2018, Zaslav doubled down on reality content and paid $11.9 billion for Scripps, which owned the Food Network, HGTV, and the Travel Channel. Some analysts were skeptical, as linear television was morphing from a dual-revenue-stream (cable fees and advertising) cash cow to a declining business. Early in 2021, Zaslav reached out to AT&T CEO John Stankey, and a year later a deal was struck to merge Discovery with AT&T’s WarnerMedia business for $43 billion.

I worked at Time Warner—Fortune magazine and CNN—for 29 years until 2014 and know top executives at these companies, some of whom I spoke with for this article, some on the record and some on background. Zaslav declined to be interviewed.

“It was really orchestrated by Zas”

The merger was accomplished through the financial jujitsu of a Reverse Morris Trust, which allowed AT&T to divest Warner without paying taxes. The deal fits the modus operandi of Malone—who likes to be referred to as “Dr.” (he has a doctorate in operations research from Johns Hopkins University). Malone is a master of complex transactions that optimize tax avoidance. What is simple to understand, though, is that since the deal on April 8, 2022, WBD shares are down 46%, while the S&P 500 index is up 1%.

I asked Greg Maffei, CEO of Liberty Media, the company at the epicenter of Malone’s current holdings, what was behind the deal. “It was really orchestrated by Zas,” Maffei says. “John went along with it because he thought it was the right thing, because it was Zas’ best path. It wasn’t clear where Discovery was going. It had no easy way out.”

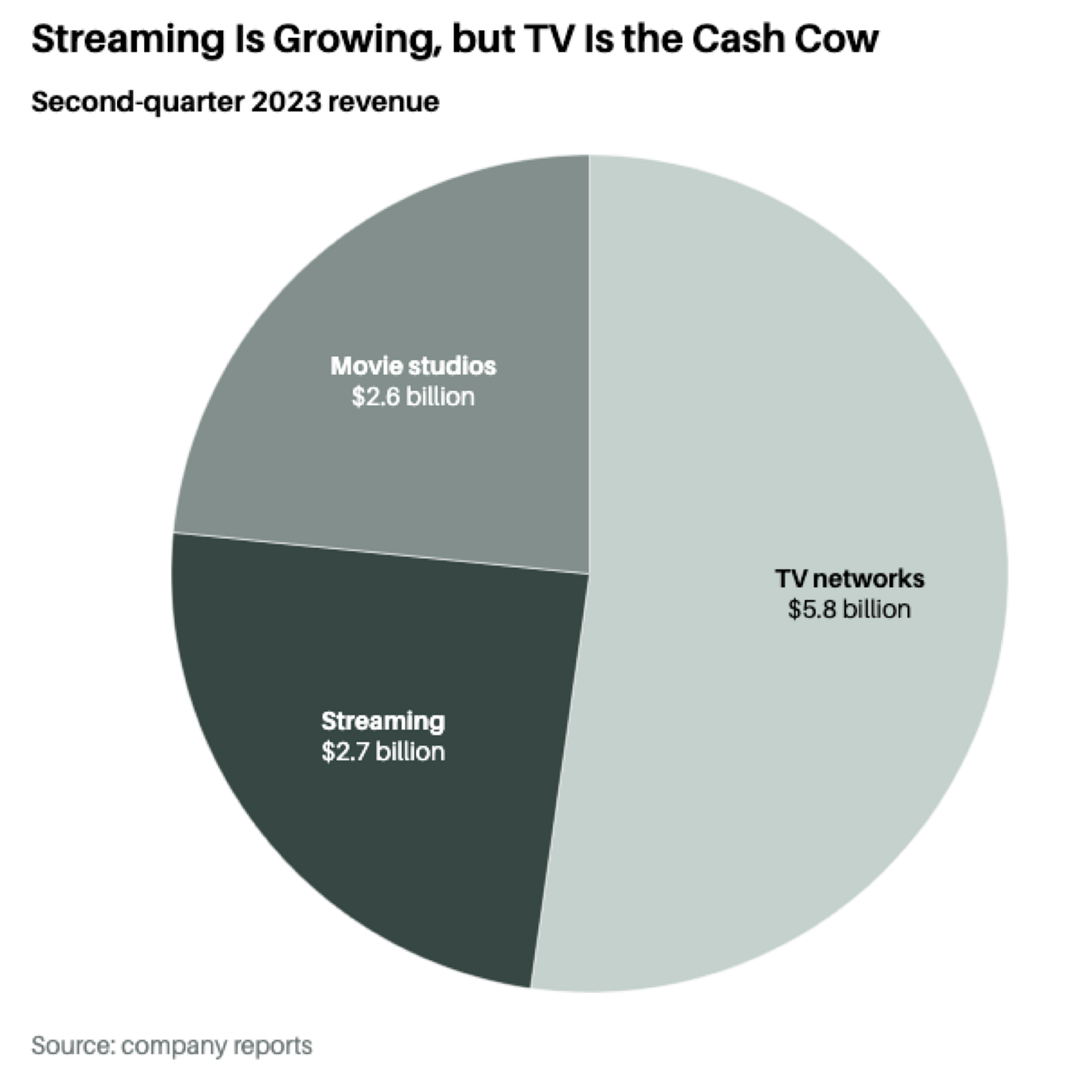

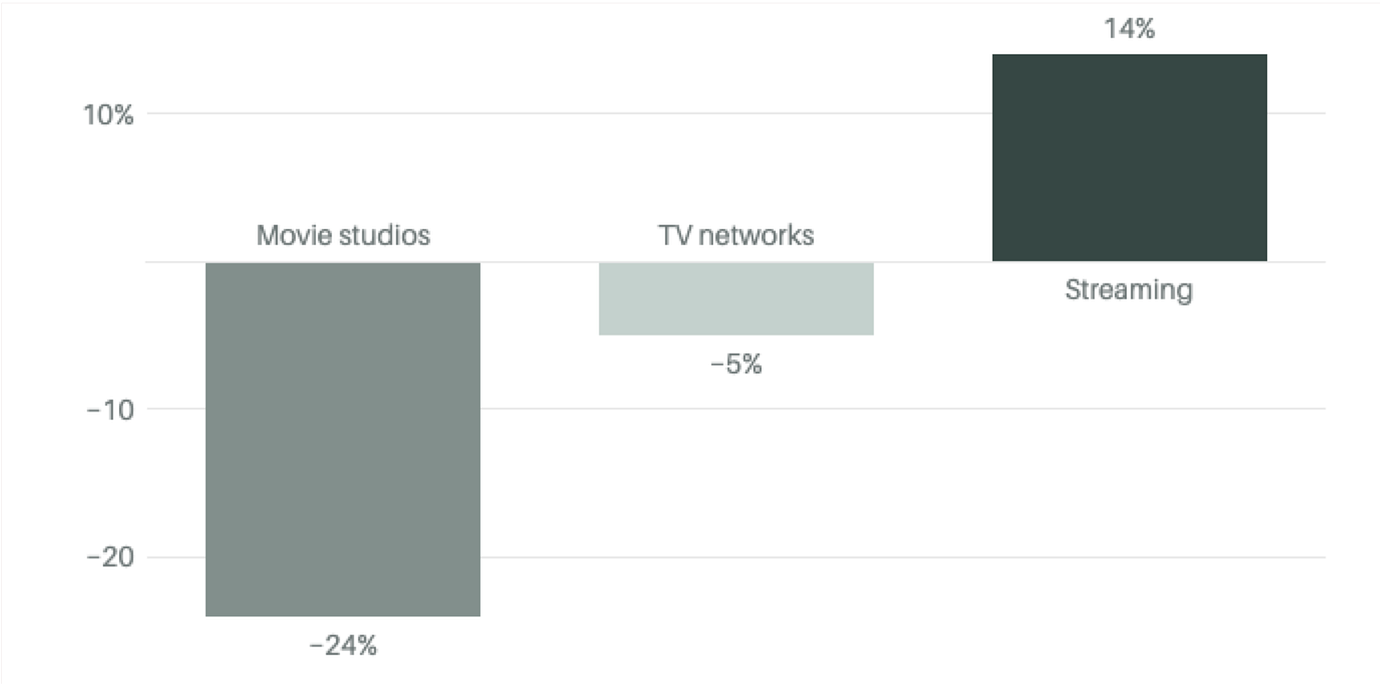

Zaslav has put WBD assets into three buckets: networks, which has cable TV operations including CNN, the Food Network, Discovery, and TBS; studios, mostly Warner Brothers; and direct-to-consumer, which has Max and includes HBO.

The key driver is networks, which according to the company’s second-quarter report—bordered in Barbie pink!—did over $5.7 billion in revenue and $2.1 billion in adjusted earnings before interest, taxes, depreciation, and amortization, or Ebitda, amounting to more than 55% of WBD’s revenue and most of the company’s Ebitda. But this business is declining—revenue and Ebitda fell 5% and 7%, respectively, in this year’s second quarter.

Year-over-year revenue change

The company uses Ebitda, since its operations are unprofitable because of the amortizations and write-offs related to the merger. In the second quarter, the company had a net loss of $1.2 billion.

Zaslav hopes the Max app, where consumers pay a monthly subscription to the company, will make up for the shrinking networks business. “A lot of the merger was predicated on combining Discovery content with Warner Brothers and HBO content, which would make a much stronger direct-to-consumer app. [The question is], is it working?” asks Alex Fitch of Harris Associates, WBD’s largest active shareholder with a 2.6% stake.

Max was just rolled out this past April, so it’s still in its early days, and while revenue grew 14% in the quarter to $2.7 billion, the business lost $3 million in Ebitda, mostly from start-up costs. Perrette thinks this business could have a 20% margin—at some point. “I’m not saying next year, but over time,” he says.

Max has 96 million subscribers as of June 30, down some 1.8 million subscribers for the quarter, which the company said is due to the churn of aggregating HBO, Max, and Discovery. Of the dozens of streaming platforms, Max is among the top-ranked domestic streamers after Netflix (238 million), Amazon Prime (estimated 200 million), and Disney+ (146 million).

”If you’re going to be a pure play, Warner Bros. Discovery has the best chance of kind of creating the new model”

The movie studio, for all its romance and glam, is significantly smaller than the network business, with more-fickle results. Second-quarter revenue there fell 24%, to $2.6 billion, while Ebitda dropped 26%, to $306 million. To be sure, Warner Bros. Pictures—the home of Batman, Harry Potter, and Lord of the Rings—was unusually weak this past quarter.

Plus, the rest of the year will be supercharged by Barbie, probably to be the biggest-grossing movie of the year and the biggest-grossing WBD movie ever, with $1.3 billion in worldwide box office and counting. (Expect sequels.) Still, WBD’s notion that it will accentuate tentpole movies and bring stronger financial discipline is a) not a new idea, and b) even if executed, probably not game-changing.

If Max ends up not making enough money, Fitch says WBD can focus on distributing content theatrically on its networks and to the likes of Netflix and Amazon—all of which it already does, reversing a streaming-only orthodoxy from the AT&T era.

“It is a lot to juggle, but it’s just one of these things where you have to do it right,” Warner Bros. Discovery board member and Redpoint Ventures founding partner Geoff Yang tells me. “What does the business look like on the other side? I think we’re going to have the best hand in terms of the assets, the breadth, the library, and the creation capability. If you’re going to be a pure play, Warner Bros. Discovery has the best chance of kind of creating the new model.”

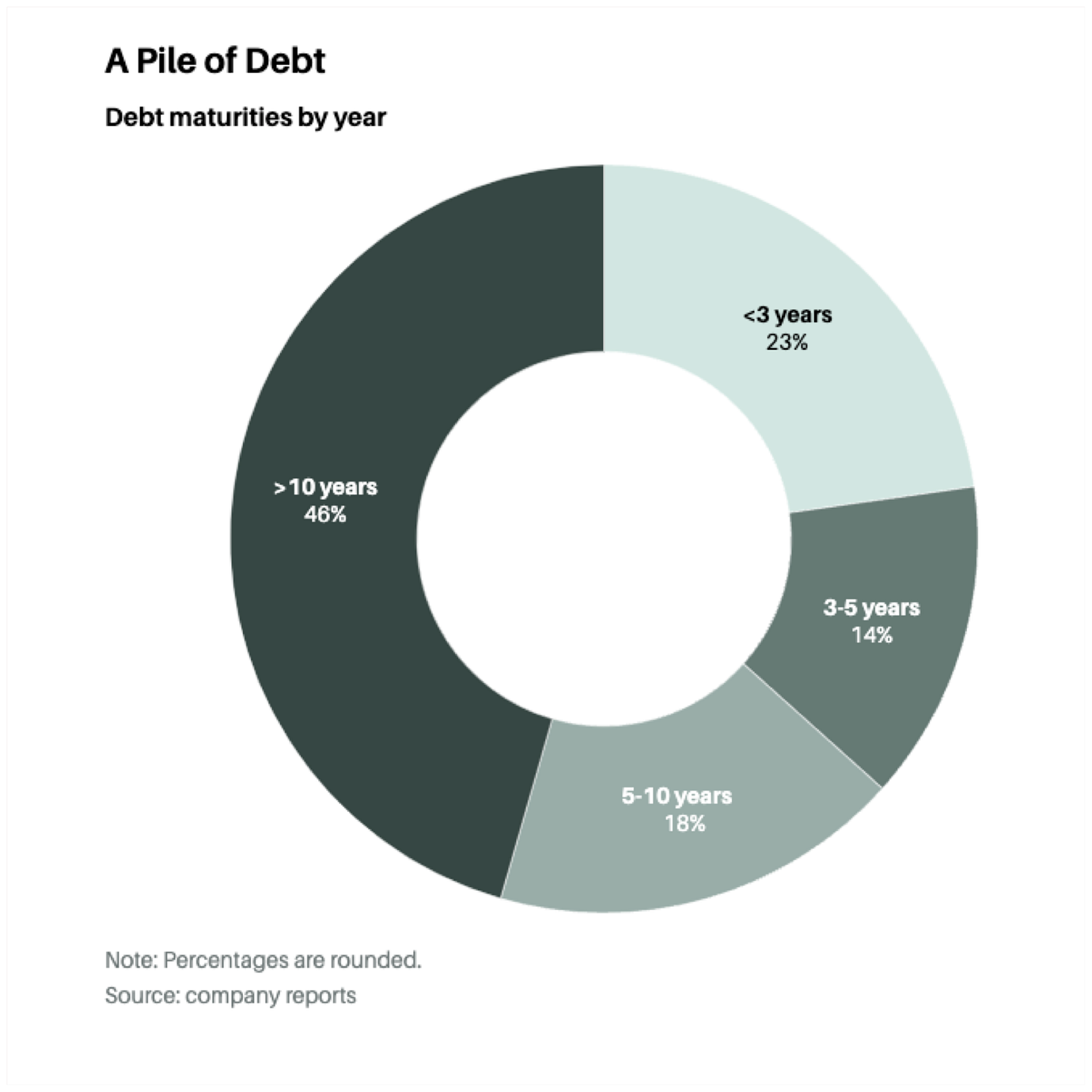

To get to that other side, the company needs to pay down debt, which it has already reduced to $47.8 billion, from $56 billion right after the Warner deal closed.

“I never lost sleep over the quantum of debt, knowing the quality of the assets that we acquired,” says WBD Chief Financial Officer Gunnar Wiedenfels, who told me the optimal amount of debt for the company is in the ballpark of $35 billion or so, “which will be 2½ to three times leverage [ratio to Ebitda]—our guidance by the end of 2024.”

A positive is that the average cost of the debt is 4.6%, with an average maturity of more than 14 years. Most analysts believe that barring some sort of catastrophe, the company can handle the debt load.

Mission critical for Zaslav and Wiedenfels, though, is generating enough cash flow to service the debt. And the company delivered in the second quarter, with free cash flow more than doubling to $1.7 billion. For the year, Wiedenfels is telling Wall Street it should generate $4.5 billion to $5 billion in free cash, coming from more revenue (Barbie again) and Max subscriptions, but also from reducing costs, culling weak content, and layoffs.

The writers and actors strike paradoxically benefited WBD to the tune of $100 million in the second quarter and more in the third quarter, as the company saves money by not producing content. Of course, that’s akin to forsaking capital spending, which makes for short-term gain and long-term pain.

“This is a fight against the endless pursuit of more wealth. How many private jets does David Zaslav need?”

The strike has other downsides—like Rep. Alexandria Ocasio-Cortez calling out Zaslav at a July rally in Manhattan. “This is a fight against greed,” AOC told the strikers. “This is a fight against the endless pursuit of more wealth. How many private jets does David Zaslav need?”

In fact, any way you cut it, Zaslav has been paid a serious amount of money since Discovery went public in 2008. According to Equilar, which tracks corporate leadership data, Zaslav’s total realized pay (really, his take-home pay), which includes base salary, bonuses, stocks that vested and options exercised, and the value of all other compensation within the given fiscal year, is $825,794,276 since Discovery’s IPO 15 years ago, making his average annual pay at just over $55 million.

Does Zaslav deserve all of this money because he has done so well by shareholders? Not particularly. WBD stock has underperformed the S&P 500 in nine of the past 15 years, over which time WBD stock had a total return of 22.6% versus 418% for the S&P 500.

Zaslav and Discovery did have a good run early on—from 2008 through 2013—when WBD stock beat the market four out of six years, giving investors a 294% total return, versus 60% for the S&P 500, but the stock has badly lagged over the past decade. It’s almost as if the WBD board fell into the habit of showering Zas with pay when performance was good, but forgot to turn off the spigot when it wasn’t.

Only Les Moonves—then CEO of CBS, now part of Paramount Global—has appeared on Equilar’s list of the 10 highest-paid CEOs more than Zaslav (six times, to Zaslav’s five) over the past decade. Paramount stock has lagged along the lines of WBD, down 70% since September 2013.

What do WBD shareholders think about this? “We’re generally OK with compensation packages that provide a management team with a lot of upside—if they create a lot of value for shareholders,” says an institutional shareholder. “It just needs to also be paired with a base salary that is arguably below the peer group. If you’re gonna get outsized upside, you shouldn’t also get outsize compensation in the downside scenario.”

Is this the case with Zaslav? I asked.

“No.”

Have you voiced your concern about this to the company?

“Yeah.”

Zaslav’s comp defenders point out that his current batch of options are priced in the $30s and $40s, far above the stock’s current $13 price and deeply out of the money. They argue that shareholders would need to do very well for Zaslav to do well going forward. That’s true to an extent.

But in a Securities and Exchange Commission filing on March 6, Zaslav’s pay was amended so that he is now rewarded in part based on free cash flow and debt reduction. Zaslav will be eligible for an additional $12 million in performance-based restricted stock units every year through 2025. He would be eligible for another $11.5 million a year over the same period if the company hits some yet-to-be-defined cash flow and deleveraging goals.

I asked an institutional shareholder what he thought about this new plan. “Our opinion is these compensation committees get a little bit cute with trying to come up with metrics that are palatable, and ultimately it’s the stock price that matters.”

”Mr. Zaslav’s compensation is more than 90% performance-base”

WBD Chairman Samuel Di Piazza says the board “is confident that these additional incentives offer a more competitive package against the backdrop of ongoing industrywide transformation and economic headwinds, and better position the company to advance core drivers of shareholder value.”

You could make the argument that this change better aligns Zaslav’s pay with the current goals of the company. You could also argue that his plain-vanilla stock options aren’t working out, and the new plan is a make-good. Another way to look at it: Zas is now getting compensated directly for generating free cash flow, but shareholders aren’t.

The company has a different view. “Mr. Zaslav’s compensation is more than 90% performance-based, and thus any benefit he receives reflects exceptional value delivered for the company, its stockholders, and employees,” it said when asked about the CEO’s pay. “Likewise, Zaslav’s total compensation during his nearly two-decade tenure reflects his proven track record of building Discovery from a collection of domestic cable networks into one of the world’s leading media companies, as well as his pivotal role in the acquisition and integration of WarnerMedia, and his strong leadership of Warner Bros. Discovery and its diverse businesses.”

Is WBD a good stock to buy? The pro argument is that WBD today is like the early days of Discovery; its properties are sleeping giants, the stock is depressed, and Zas will work his magic. The con argument is that this time, Zaslav has all kinds of headwinds: The company is highly leveraged, the bulk of its business—linear cable TV—is in decline, and its best avenue for growth—streaming—is highly competitive.

There’s also the ever-spiraling cost of sports rights—WBD has some for the National Basketball Association and the National Hockey League and half of March Madness—perhaps the only content that keeps consumers on cable. That’s a lot of moving parts—some of which aren’t moving in the right direction.

There are really only three major pure-play legacy media companies left now: Warner Bros. Discovery, Paramount, and Walt Disney, a status quo that seems unlikely to last. The standard interpretation of a Reverse Morris Trust is that the newly created company is prohibited from making any major deals for two years to prevent the transaction from being a fig leaf to reset the company’s valuation. Warner Bros. Discovery will hit that anniversary in April, eight months from now. Will Zas be a buyer or a seller? And of what and/or to whom?

”It doesn’t seem like it’s reflected in the stock price yet”

Decades ago, I was at a swanky Time Warner event, and an executive whispered in my ear that our company was great to work for—referring to the Town Cars, cocktails, and other perks—but not so great for shareholders. Fast-forward to today, where you might say that this descendant of Time Warner is a great place to be a bondholder—and still not a great place to be a shareholder. With the stock in the tank, Fitch of Harris notes “that credit markets have been much more positive about the progress that we’ve seen than the equity markets. You’ve seen spreads on the bonds get to the lowest levels since the deal closed. The credit market is seeing a lot of progress there, [and] it doesn’t seem like it’s reflected in the stock price yet.”

Of course, there’s one constituent who has been treated even better than bondholders, and that’s Zas himself. Zaslav likes to say that his two mentors are Malone and former General Electric CEO Jack Welch—with Malone known for his acumen and strong, long-term track record, and for building a complex and frustrating empire, and Welch for his charisma and chutzpah and for his extravagant compensation and management approach that was once celebrated but is currently not held in such high regard.

Now it’s time for Zaslav to demonstrate to his shareholders, employees, and customers what his legacy will be.