”Indiens API-satsning är överlägsen USA, EU och Kina”

Indien, som just gått om Kina som världens folkrikaste land, håller på att bygga upp en världsunik digital infrastruktur, skriver Financial Times: Mer jämlik än USA:s laissez faire-ansats, mer innovativ än EU:s regeltunga modell och mer transparent än Kinas totalitära, enligt entusiasterna.

Nyckeln till ”India Stack” – den digitala infrastrukturen som sömlöst länkar ihop olika operatörer – är regeringens öppna API:er som utvecklare kunnat bygga vidare på. Farhågor reses emellertid kring mängden data som företag och myndigheter samlar på sig samtidigt som landet saknar dataskyddslag.

The India Stack: opening the digital marketplace to the masses

New Delhi has pioneered a new approach to online infrastructure in its drive to connect 1.4bn. But there are privacy and data protection concerns.

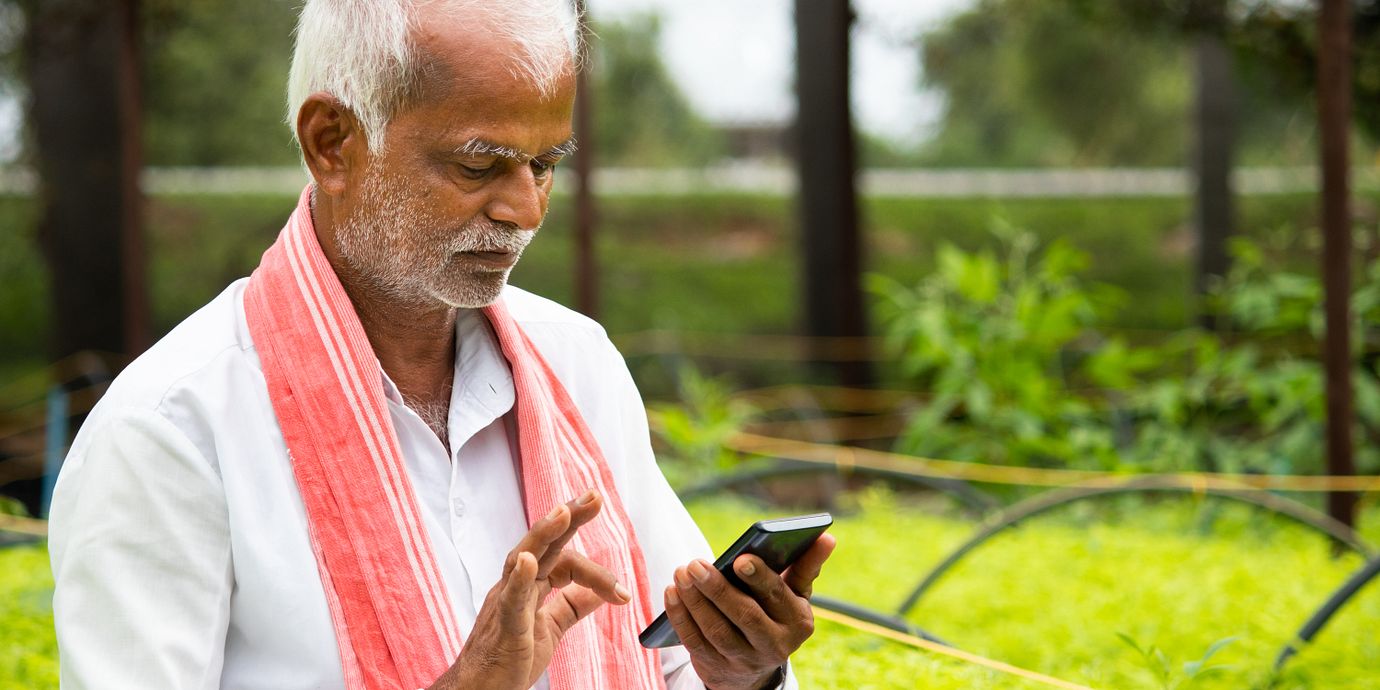

A decade ago, Tej Pal signed up for India’s Aadhaar biometric identity scheme, acquiring his first national ID card.

A few years later the 44-year-old, who sells fruit near Delhi, used it to open his first bank account. Last year he took a loan to buy his first smartphone to sign up for the Unified Payments Interface (UPI), India’s digital money system.

Now Pal, who grew up in a north Indian village without banks or landlines, takes payments for bananas or mangos directly into his bank account via apps such as Google Pay or Walmart-owned PhonePe.

“Earlier, when I used to go home to my village, I had to hide all the cash — literally all my savings for months — in my socks, so as to not be robbed on the train,” he says. Life has become “much easier”.

Pal’s story has been replicated millions of times in recent years in India as the authorities launched an unprecedented drive to bring its 1.4bn population online.

At the heart of this effort is the so-called India Stack: government-backed APIs, or application programming interfaces, upon which third parties can build software with access to government IDs, payment networks and data.

This digital infrastructure is interoperable and “stacked” together — meaning that private companies can build apps integrated with state services to provide consumers seamless access to everything from welfare payments to loan applications.

Supporters argue that India has found a world-beating solution for building out and regulating the online commons that is more equitable than the US’s laissez-faire approach, more innovative than the EU’s regulation-heavy model and more transparent than China’s totalitarian template.

Now, as New Delhi hosts this year’s G20 presidency and surpasses China as the world’s most populous country, India’s public digital infrastructure has become a core part of Prime Minister Narendra Modi’s efforts to present India as a nascent economic superpower, alternative investment destination to China and leading voice of the global south.

At panels and events featuring global government and business leaders, Modi’s government has launched a digital diplomacy drive to promote its digital infrastructure template as a new model for development around the world, with some success. Countries including the Philippines and Bhutan have adopted elements of Indian-designed infrastructure.

“This kind of public-private partnership approach is neither there in the west nor in the east,” says Ashwini Vaishnaw, India’s minister of information technology. “We believe this is a great contribution from our side to the world — so that’s why we have offered it to the world.”

However, as the scope and ambition of India’s digital push have grown, so too have the concerns. India’s government and companies are collecting unprecedented quantities of data without a data protection law, creating ample opportunities for surveillance and abuse in a country where civil liberties groups have accused the state of over-reach in snooping on citizens.

And while boosters describe digitisation as a great leveller for India’s poorest, critics say the growth of digital services is not enough to compensate for the inequality of skills and internet access that leave hundreds of millions on the wrong side of the country’s digital divide.

“Technology cannot substitute fundamental existing gaps, such as inadequate service delivery and low digital literacy,” says Prateek Waghre, policy director with the Internet Freedom Foundation.

‘A huge bet on IT’

India’s government argues that bringing the world’s poor online is one of the fastest means to the end of global development. Around 850mn globally don’t have legal ID and 1.4bn are unbanked, according to the World Bank.

Digital infrastructure is not unique to India. The IMF says 99 per cent of digital pioneer Estonia’s population has ID while nearly 80 per cent of adult Kenyans have used digital payments, thanks to the country’s mobile money network. But analysts say the scale and interconnectivity of India’s digital infrastructure has little parallel.

India’s model “is very innovative. It’s different to what you see in most other countries in the world,” says Luis Breuer, the IMF’s senior resident representative to India. “India as a country has made a huge bet on IT.”

The India Stack started with the Aadhaar digital ID scheme, which was launched in 2009 and — though controversial with privacy advocates — now covers nearly the entire adult population. Atop this “identity layer” sits a “payments layer,” which includes the UPI digital money system, and a “data layer” where citizens can, for example, store official documents virtually.

The India Stack

Identity

Indian citizens and foreign residents sign up for Aadhaar, the Indian state biometric identification database. A 12-digit identity number is allotted to each person, and linked to a photograph, fingerprint and iris scans in a database administered by the Unique Identification Authority of India. A card is issued with these details, which can be linked to a mobile phone

This universally recognised ID enables banks, telecoms companies and others to verify a new customer’s identity immediately, which the government says cuts the risk of fraud and the costs of verification. It allows the government to send direct benefits payments to Aadhaar-linked bank accounts.

Payments

Cashless economy

The Unified Payments Interface links people with banks and mobile money apps developed by India’s fintech sector into one large transaction system. This means that even small traders can accept mobile payments for goods, and remittances could be sent instantly and at a lower cost.

Data

Paperless state

The third layer includes the storage of important data, from the Aadhaar card details to driving licences, vehicle registrations, academic qualifications and medical documents, in a digital database called DigiLocker. These can then be verified or shared with consent.

Though backed by Modi’s government, Aadhaar started when the opposition Indian National Congress was in power, and the private sector also helped develop India’s digital infrastructure. Apps and services have proliferated on top of it, from paperless Covid-19 vaccination certificates to a one-roof system for paying utility bills to a platform for sharing school curricula digitally.

Supporters say this digitisation saves time and money. The authorities made $66bn of benefit payments online in the year ended 2021, for example, compared with $1.2bn in 2014, helping to cut waste and leakage.

And the cost to banks of verifying customer identities using Aadhaar can fall from Rs1,000 (approximately $12) to Rs5 each, according to one estimate in an IMF report this month. This helped banks to open hundreds of millions of new accounts over the past decade, leading to important gains in financial inclusion.

“I can bet nowhere in the world does this exist at this speed, at this price point”

Several countries have already begun working with India on their own programmes. The Philippines and Morocco use made-in-India digital identity schemes, while Jamaica used the country’s technology for its Covid-19 vaccination certificates. Singapore recently connected its digital payments system to India’s to allow instant cross-border remittances from its 400,000 residents of Indian origin.

“I can bet nowhere in the world does this exist at this speed, at this price point,” says Sopnendu Mohanty, chief fintech officer at the Monetary Authority of Singapore. “A poor immigrant worker can now send money at small values — $10, $20 — instantly . . . This creates a massive impact at the bottom of the pyramid.”

The UN Development Programme estimated last year that digital public infrastructure could add as much as 1.4 per cent growth to lower- and middle-income countries by 2030, allowing them to accelerate financial inclusion and “leapfrog” other countries.

Many in India “have a common belief that digital public infrastructure is a way to transform a country”, says Nandan Nilekani, the co-founder of IT multinational Infosys who is helping lead India’s digital infrastructure push. “Now we have evidence on the ground.”

A new model for digital business?

India has made some of the tech behind its digital infrastructure public for others to use.

Officials say this guards against both excess state control and market capture by Big Tech giants such as Amazon and Google in advanced economies like the US.

This has indeed proved a powerful tool for businesses to innovate. UPI’s interoperability, for example, means that customers use it to carry out transactions with whichever bank or app they choose.

Companies such as Google and PhonePe in turn built successful payments apps on top of it, helping the service take off — with more than 8bn transactions a month.

Ambarish Kenghe, vice-president at Google Pay, says that as digital payments grow “a bunch of opportunities become available”, from allowing customers to pay bills through the app to taking loans. “You’ll see us enabling commerce, enabling services on top of payments. That’s my hope,” he says.

The Indian authorities are now experimenting with even more ambitious initiatives. Among them is the Open Network for Digital Commerce, an interoperable ecommerce scheme that the authorities began testing in India’s tech hub Bangalore last year.

While platforms such as Amazon manage everything from the seller to the customer, through ONDC a buyer can order groceries using digital payments service Paytm from a shop registered to a different app, such as Bitsila. A third app, like Dunzo, can deliver the order.

India argues that opening up the infrastructure behind ecommerce in this way will help check the power of Big Tech by limiting its ability to dictate terms, helping lower costs and grow the market. The traditional ecommerce model is “very one sided”, says Nitin Nair, an ONDC executive in Bangalore. ONDC will “make this a slightly more democratic process”.

An open-source ride-sharing app, Namma Yatri, also launched using ONDC in the city last year to connect drivers directly to customers without commissions.

“If things go to plan, it will be the next online revolution,” says Niyas MK, whose 100-year-old Bangalore-based grocery chain MK Retail recently started trialling ONDC. “I didn’t have much trust. But now I think it’s going to be the next big thing.”

Some critics are sceptical about India’s claims to be crafting a new model for digital business, however. Despite claiming to undermine monopolies, a few big names have managed to assert commanding positions in the digital sphere: PhonePe and Google Pay account for over 80 per cent share of UPI transactions between them, according to official data.

“If you look at UPI, the idea was this would prevent monopolies,” says the IFF’s Waghre. “But in terms of dominant apps, it’s a duopoly between Google Pay and PhonePe.”

Critics also argue that the success of these services is not simply the result of organic growth but of India using its regulatory clout to tilt the playing field in their favour. For example, the government subsidises merchants using UPI to promote its growth, which has eroded demand for cards from companies such as Visa and Mastercard. The value of debit card transactions fell more than 15 per cent in March from a year earlier, according to data from the Reserve Bank of India.

UPI’s “biggest impact comes when private players are able to leverage the stack on a non-discriminatory basis to deliver their services so consumers can choose the product that best suits their preferences,” says Alexander Slater, managing director of the US-India Business Council.

Access and privacy issues

Dileep Kumar’s shop in the rural area of Haidergarh, in India’s northern state Uttar Pradesh, is both a symbol of digital India’s reach and of its limitations.

From his small storefront, the 27-year-old earns Rs300 to Rs400 a day helping Indians without smartphones navigate the maze of online services that have become so central to their lives.

“Whether it’s a birth certificate or a death certificate, applying for jobs, or a soft copy of a photograph required for an online form, people come in for this,” Kumar says, as a female customer applies her thumbprint to a scanner to secure a payout from her bank account.

Kumar’s shop highlights how, even as digital services take off, poor internet access and skills mean that much of the population — particularly rural dwellers and women — is at risk of being left behind.

Fewer than half of India’s people are able to use the internet, according to the IMF, while only 15 per cent of rural households and 42 per cent of urban households have internet access. Of women who own a mobile phone, a third are not able to read text messages.

“The problem is that people are not educated. They don’t know how to do these things themselves,” says Kumar’s friend Pintu Singh, a 25-year-old farmer. “Everything is online so they have to do it. And if they can’t do it themselves, they have to get help, and they have to pay for it.”

The IMF’s Breuer says: “The big challenge here is dissemination of technology and to what extent will it reach the bottom half of the pyramid. To the extent that [digital public infrastructure] leads to productivity gains, you might have some inequality issues become even more exacerbated.”

Gaps in digital literacy were laid bare during the Covid pandemic, when fraudsters sold online loan schemes to Indians who had lost their jobs.

And regulatory oversight has also not kept up with the speed of India’s digital push. Tens of millions of Aadhaar records, for example, have allegedly been exposed in a string of data breaches. “The importance of privacy and security is very much an afterthought, rather than something that’s built into these projects,” says Udbhav Tiwari, head of global product policy at the Mozilla Foundation.

While the country has some data regulation, it lacks a comprehensive data protection bill despite years of discussion. A pending draft of the bill includes sweeping carve-outs for the authorities to snoop on citizens that critics warn risk turning India into a surveillance state.

“It’s about digitising our entire society,” says Srinivas Kodali, a digital rights activist who has petitioned India’s Supreme Court on cases related to Aadhaar. “And when your digital society’s entire basis is built on identity, you will not have privacy.”

For Pal, the fruit seller, adjusting to “Digital India” has not been easy, whatever the benefits. He is still paying off the debt he took out to buy his smartphone and is yet to fully grasp the UPI payments network, given that he struggles to read and write.

“It is a hassle for me to figure out the payment system, but I have no choice,” he says. “It works for me because I can’t afford to lose customers. You have to move with the times.”

©The Financial Times Limited 2023. All Rights Reserved. FT and Financial Times are trademarks of the Financial Times Ltd. Not to be redistributed, copied or modified in any way.