Köp distributör av Ozempic – rusar i tysthet

Läkemedelsleverantören McKesson är en storspelare i sin nisch, som många investerare helt har missat. Det kan visa sig vara ett stort misstag att ignorera aktien, skriver Barron’s i en köprekommendation. Med tanke på de höga tillväxttalen ser aktien billig ut, även efter en kursuppgång på drygt 20 procent hittills i år.

Bolaget tjänar pengar på att distribuera läkemedel från jättar som Pfizer, Eli Lilly och Novo Nordisk, och rider därmed på deras framgångar. Trots den enkla affärsmodellen – köpa läkemedel för leverans till apotek – drar McKesson fördelar av inträdesbarriärer på marknaden i form av hårda regleringar. Det hindrar Fedex och andra fraktjättar från att göra insteg på marknaden.

Buy McKesson Stock. Ozempic Can Lift Drug Distributors Too.

Drug distributor McKesson may be the largest U.S. company that investors have never heard of. Overlooking its stock could be a big mistake.

Just what is McKesson (ticker: MCK)? It isn’t a pharmacy benefit manager like Cigna Group’s (CI) Express Scripts or UnitedHealth Group’s (UNH) OptumRx, though it is often confused with one. And it doesn’t develop and manufacture the drugs that people need, like Pfizer (PFE), Merck (MRK), or Eli Lilly (LLY). Instead, McKesson makes its money by delivering medicines to pharmacies and hospitals, and it does enough of it to have become the ninth-largest U.S. company based on revenue. Even the stock’s rally—it has gained 22% this year—hasn’t brought it much attention.

It should. From its steady-Eddie cash flows to the potential boost it might get from delivering Novo Nordisk’s (NVO) Ozempic and other weight-loss drugs, the Irving, Texas-based McKesson looks poised to keep the gains coming—all while providing a service that millions of people can’t live without.

“McKesson is showing healthy growth for a company of its size, helped by very targeted investments and strong client relationships,” says Jefferies analyst Brian Tanquilut. “That makes it a compelling fundamental story.”

McKesson’s business is relatively simple. It buys drugs from manufacturers and then distributes them to pharmacies. These include mom-and-pop shops and, increasingly, big national chains such as Walmart WMT) and CVS Health (CVS), which are among its largest clients. Yet it’s a difficult-to-replicate logistics business—one not easily done by United Parcel Service (UPS) or FedEx (FDX), given the need to securely handle medications that are tightly regulated by the government and to transport them on strict deadlines in conditions that keep them potent.

It’s a growing business, too. According to the Centers for Disease Control and Prevention, nearly half of all Americans used at least one prescription drug in the past month, while nearly a quarter used three or more. The arrival of Lilly’s Mounjaro and Novo Nordisk’s Ozempic should provide a growth kicker for McKesson, which shares the business with Cardinal Health (CAH) and Cencora (COR), formerly AmerisourceBergen, in a virtual triopoly.

“The distribution structure [that McKesson and peers] have is very difficult to replicate. That’s evident in their return on equity and return on invested capital,” says Chris Conway, senior portfolio manager at GYL Financial Synergies. “These are generally solid businesses.”

McKesson, in particular, has made great strides since the Covid pandemic. Before then, the stock was hampered by worries about government drug price regulation, high executive pay, unknown opioid liability. Those issues are now behind it. Its well-compensated CEO, John Hammergren, retired in 2019 and was replaced by Brian Tyler.

In 2022, the company and its peers were part of a settlement with multiple state and local governments that had brought lawsuits against pharmaceutical distributors for their alleged role in the opioid crisis. McKesson’s $7.4 billion portion will be paid out over nearly two decades, lessening the financial impact. In addition, at the moment Congress is much more focused on other issues beyond drug pricing, from the wars in Ukraine and Israel to intraparty disagreements.

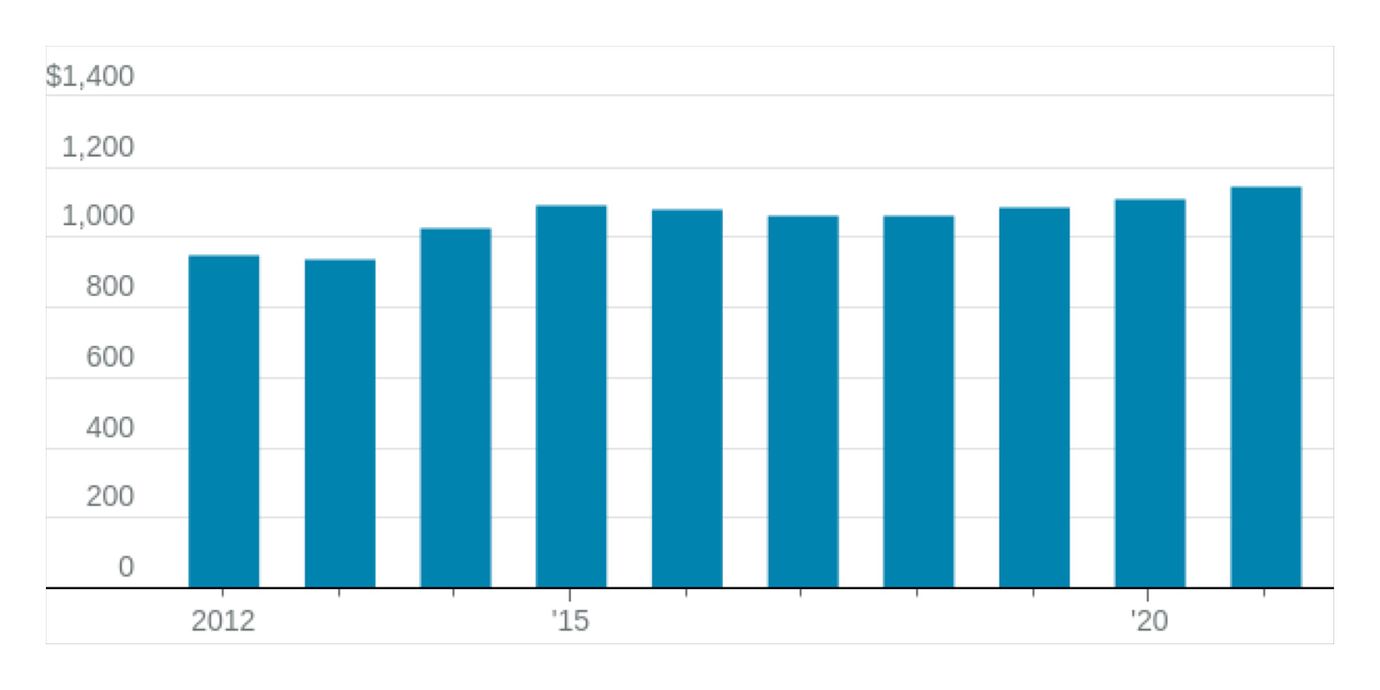

A healthy outlook

Spending on prescriptions has marched steadily higher as an aging population takes more medication for chronic conditions.

Now, McKesson’s core distribution business is back to delivering low-single digit operating profit growth, with sales expected to grow 10%, to $304 billion, in fiscal 2024, and earnings growing 4.8%, to $27.20 a share, then jumping to 13.4% in fiscal 2025 to $30.84 a share.

McKesson’s business is still relatively low margin—gross margins have averaged just 4.8% over the past half-decade and have held relatively steady in recent years—but low margin doesn’t mean low cash: In its most recent fiscal year, ended on March 31, it generated more than $5 billion in cash flow from operations. That money is being spent well: In August, the company announced a new, $6 billion share-repurchase plan, bringing its total authorization to nearly $9 billion, while profits are still climbing even without the pandemic bump.

Noah Hamman, founder and CEO of AdvisorShares, calls McKesson a two-fer, citing its strong performance and its plans to buy back shares.

Despite the buybacks, its balance sheet remains “pristine,” says Jefferies’ Tanquilut. At the end of June, the company had net debt of about $3 billion, roughly $800 million less than three years ago. He thinks the shares should trade at $510, 12% above Wednesday’s close of $456.66.

Tanquilut is bullish on McKesson over Cardinal and Cencora because of its higher growth rate: He pegs it at 12% to 14% over the next few years, a figure he thinks will be industry-leading. That makes the shares’ valuation—at 15.6 times forward earnings—attractive, despite being above the company’s five-year average of 11.1 times. “The stock is cheap, given how other stocks in the S&P 500 index with a similar growth rate are trading,” he notes.

That’s also much cheaper than the makers of glucagon-like peptide-1, or GLP-1, products for diabetes or weight loss, even though McKesson is likely to benefit if there is a bump in prescriptions for Ozempic, Wegovy, or Mounjaro. Any increase in prescriptions means more medications shipped through McKesson’s system, and their high price tags add to the company’s top line, a boost that Cardinal and Cencora have highlighted, as well.

And that would be just one more way for McKesson stock to keep delivering.