Kris på Kinas bomarknad hotar mål om ekonomisk dominans

Medan världens blickar riktas mot nedstängningarna i Kina och dess effekt på världsekonomin pågår en sannolikt allvarligare kris. Bostadsförsäljningen har dalat konstant i nästan ett år och kan tynga Kinas tillväxt betydligt under de närmsta decenniet, skriver Bloomberg.

För att minska risken för bostadsbubblor har regimen försökt svalka byggandet och hålla tillbaka de växande bolånen. Men åtgärderna kan ha varit för långtgående. Utan en stark bostadsmarknad kan det bli svårt för Kina att utmana USA om att bli världens största ekonomi, skriver tidningen.

China’s Property Slump Is a Bigger Threat Than Its Lockdowns

The worst decline on record could hold growth below 4% for the rest of the decade.

By Tom Hancock and Emma Dong, Bloomberg Businessweek

22 June 2022

While global attention is focused on the economic impact of coronavirus lockdowns in Shanghai and Beijing, the slump in China’s housing market is likely to have even more profound implications.

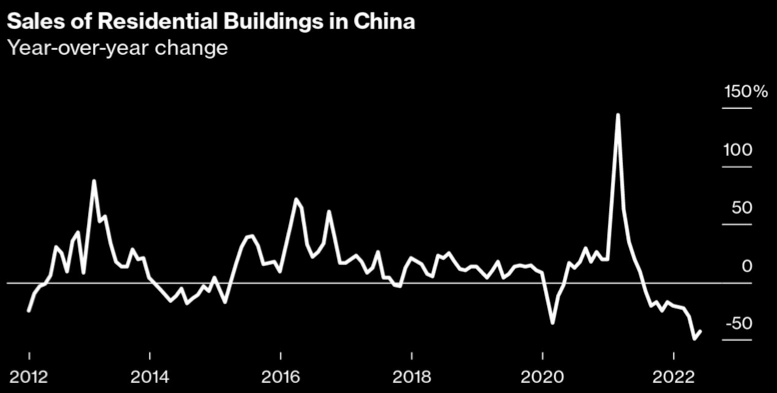

An official index that tracks apartment and house sales has posted year-on-year declines for 11 months straight—a record since China created a private property market in the 1990s. With demand for services and commodities generated by housing construction and sales accounting for about 20% of gross domestic product, that represents a big drag on growth this year.

“This is the worst property downturn on record,” says Lu Ting, chief China economist at Nomura Holdings Inc. The length of the drop exceeds those in 2008 and 2014 that reverberated through global commodity markets by curbing Chinese demand for imported steel and copper.

The slump began last year as Beijing took steps to slow the growth of mortgages and funding for property developers as part of an effort to tame bubbly prices and reduce financial risks. President Xi Jinping is sticking to his tough stance, which some economists argue could bring forward a historic peak in property construction and ensure China’s GDP growth rates average less than 4% over the rest of the decade.

“This is the worst property downturn on record”

The pace of China’s housing sales declines were expected to improve marginally this year as local governments relaxed curbs in the interest of supporting growth. But because of lockdowns in Shanghai and dozens of other cities since March, this year’s drops are actually bigger than in 2021. Even though many of the country’s largest cities loosened restrictions on home purchases in recent months and China’s central bank cut mortgage rates by a record amount in May, sales in major cities declined over 40% from the previous May as lockdowns closed businesses and joblessness spiked.

“Employment has to recover to increase demand,” says Iris Pang, China economist at ING Groep NV. “This depends very much on the chance of lockdowns in the future.” She doesn’t expect a rebound in sales until 2023.

Xi and the Communist Party leadership haven’t softened their stance on housing, a departure from previous economic downturns when property was used as a stimulus. At an April meeting, the party’s top decision-makers repeated that housing was “not for speculation,” the slogan associated with financial tightening aimed at the sector. “This time it’s different, as Beijing has attached national strategic importance to reining in property bubbles,” says Nomura’s Lu.

The property market pain is expected to crimp China’s growth by 1.4 percentage points this year, which is just 0.2 percentage point less than the impact of policies to control Covid-19, according to Goldman Sachs Group Inc. economists. That puts the official 2022 GDP growth goal of about 5.5% out of reach. Some economists think getting to 3% will be a struggle.

China’s financial regulators have focused on making sure defaults by cash-strapped developers don’t lead to a wider financial crisis, and mortgage rates set in Beijing have stayed well above levels seen following the 2014 slump. Central government officials “don’t want to take the blame if things get out of control again,” says Chen Long, an economist at Beijing-based consulting firm Plenum.

Despite steep declines in sales and construction, prices haven’t fallen as much as in previous downturns because there’s less excess supply of housing, giving officials more room to maintain tight policies without enraging Chinese households, most of whose wealth is tied up in property. But the slump has fundamentally altered China’s business world. Real estate tycoons, for decades among the nation’s most successful business owners, as May 31 have lost a combined $65 billion from their net worth since 2020, according to the Bloomberg Billionaires Index. State-owned property developers are playing a bigger role in construction, including buying unfinished projects from the private sector to placate angry homebuyers.

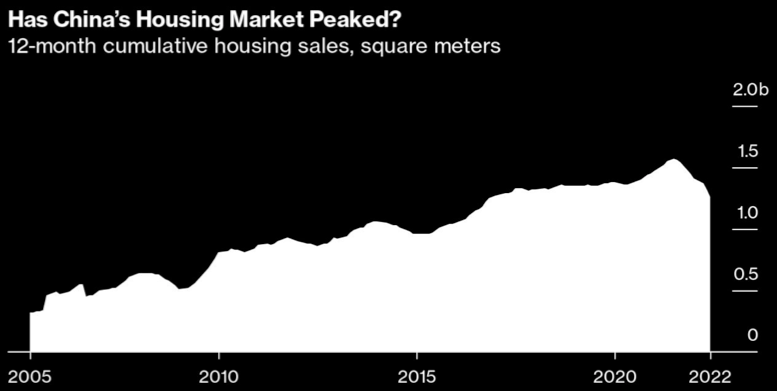

Some analysts expect housing sales to return to modest levels of growth toward the end of the year, as cities further relax mortgage and other policies. Even so, Rosealea Yao of Gavekal Dragonomics expects housing sales to decline more than 10% this year from 2021. More important, she thinks they may never recover to levels seen in the last two years. “The consumption of steel and other construction materials is likely to mirror that of housing sales, plateauing and then declining from their historic peaks,” she says.

“Slowing growth would make clear that China cannot really establish a meaningful economic lead over the US”

Even if Beijing wanted a construction boom, the fundamentals aren’t there. China’s massive urbanization process is maturing: Population growth in towns and cities dipped below 1% last year for the first time since 1996. In more developed provinces such as Guangdong in the south, about 75% of the population is urban—not far off the US rate of 83%.

Investment in housing accounts for about 11% of China’s GDP, and that will fall closer to 7% by 2030, according to a study by the Lowy Institute, a think tank in Sydney. Other kinds of investment such as infrastructure and factory construction won’t expand fast enough to fill the gap created by shrinking spending on apartment building, it argues.

The Lowy study concludes that even if China can avoid a financial crisis from the housing decline, lower investment will drag overall GDP growth to an average of about 4% for the rest of this decade. “Slowing growth would make clear that China cannot really establish a meaningful economic lead over the US. It has important implications for perceptions about where the world is headed,” says Roland Rajah, Lowy’s chief economist.

For more articles like this please visit us at bloomberg.com