Lägsta värderingen på tio år ger klippläge i Microsoft

Det gungar under Microsoft på börsen när rädslan sprider sig för en AI-apokalyps i mjukvarusektorn. Nu handlas jätten i paritet med övriga S&P 500, trots att bolaget är allt annat än genomsnittligt. Det är dags att plocka upp mjukvaruaktien, skriver Barron’s.

Marknaden missar att molnaffären inom affärsområdet Azure växer kraftigt, tack vare ökad efterfrågan från AI-bolag. Det är inte heller den enda krockkudden de har när framtiden för mjukvaruaffären ifrågasätts. Microsoft är den största ägaren i bolaget som blir viktigast i världen, nämligen Open AI, om utvecklingen fortsätter i samma spår.

Microsoft Stock Hasn’t Been This Cheap in a Decade. It’s Time to Buy.

Shares have been hammered by AI fears, but there’s a different story to be told: Microsoft has spent years preparing for this moment.

In the midst of the cloud’s emergence in 2011, venture capitalist Marc Andreessen famously declared that “software is eating the world.” Hardware was becoming commoditized and business software was taking over IT budgets.

Andreessen’s prescient call foreshadowed 15 years of transformation and arguably trillions in value creation. No legacy software company saw a bigger boost than Microsoft, which rode the cloud from stagnation to new heights.

But now it’s software—and Microsoft—getting served up on a platter, as artificial intelligence shifts priorities across the tech sector. While the iShares Semiconductor exchange-traded fund is up 10% this year, the iShares Expanded Tech-Software Sector ETF is down 20%.

Since peaking in July, Microsoft stock has fallen 28%, shedding $1 trillion in market value. For now, Microsoft and its software peers aren’t companies; they’re narratives of tech’s next generational disruption, all happening at blinding speed.

But there’s a different story to be told: Microsoft is ready for this moment.

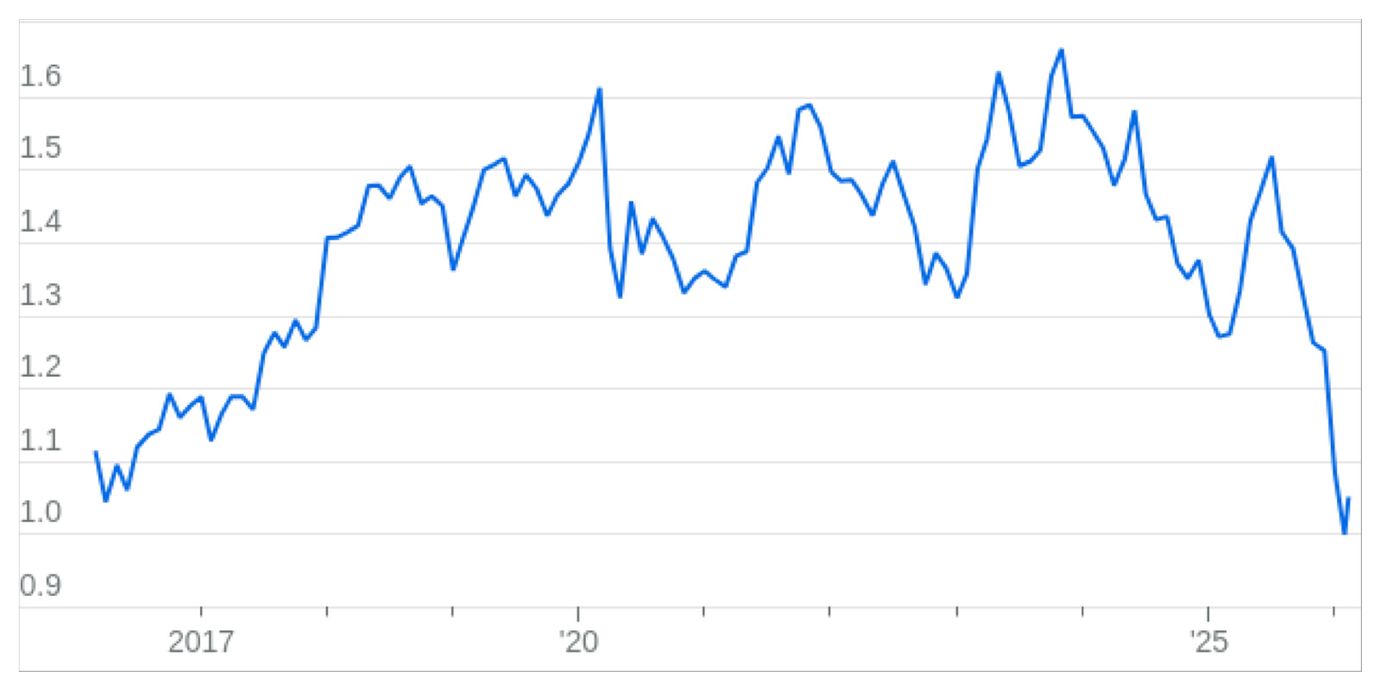

Microsoft looks cheap

Relative to the S&P 500 index, Microsoft's forward P/E is at its lowest point in a decade.

“If I look at Microsoft up and down the stack—not just Azure, but the data layer, the developer layer, application, security, even assets like LinkedIn and gaming—I think they could be beneficiaries from AI,” RBC analyst Rishi Jaluria says. “The stock is trading at a below-market multiple on earnings. So I put all those pieces together, and the stock does feel very undervalued to me.”

Effectively, investors can buy Microsoft stock at a valuation close to the overall S&P 500 index. Microsoft, though, is anything but ordinary.

The company is still poised to boost revenue 16%, to $328 billion, for the fiscal year that ends in June, according to Wall Street analysts. Earnings per share are forecast to rise 21%, to $16.48. But what the market may be missing most is the company’s AI hedge, perhaps the best in the business. That comes thanks to CEO Satya Nadella ’s prescient moves—cloud investments and his early backing of OpenAI.

And don’t count out what got Microsoft here in the first place: its software.

Apocalypse Now?

Microsoft’s products span tech categories and markets, from office productivity to enterprise resource planning to gaming consoles. The parts of the tech giant under direct threat from AI sit in the company’s Productivity & Business Processes segment. It contains Microsoft 365—formerly the Office productivity suite—other business software, and LinkedIn.

This remains the heart of Microsoft. In the first half of its fiscal 2026, Productivity & Business generated $67 billion in sales, 42% of the company’s revenue and over half its operating income. Segment sales grew by 16% from the year before, a strong showing from a mature business. The success helped propel Microsoft’s stock to a peak of $555 a share in July, giving the company a market value over $4 trillion.

But things started falling apart in the fall, as the market began paying more attention to AI’s threat to software—a selloff many began to call “The Software Apocalypse.” Today, the narrative around software sees Productivity & Business being pulled apart in several ways.

The worries stem from AI agents, software that sits on top of large language models, known as LLMs, and can accomplish a complex series of tasks from conversational commands. First to the scene last year were coding agents, which can write a large portion of the code for an application much faster than a human could. The cost per line of code has dropped significantly.

It opens up a huge set of questions for currently successful business software makers. If the cost of making finished software has declined rapidly, it removes a barrier for new competitors to enter the market. Customers could even decide to make their own custom software as a replacement.

The agent risk goes way beyond coding. Tools in a newer, more general category of so-called desktop agents have begun to gain traction among techies. These bots use LLMs to control a computer and could lead to many business functions now serviced by commercial software being replaced by agents operating on free, open-source alternatives.

Microsoft would see human users overwhelmed by machines. The subscription revenue model pioneered by cloud software would crumble, replaced by a consumption-based one that favors AI start-ups, chip companies, and cloud-computing hyperscalers. Microsoft’s staunch profit margin—the business software segment turns 82% of sales into gross profit—would have nowhere to go but down.

It’s the bearish scenario that Melius Research analyst Ben Reitzes envisioned in April 2024, when he wrote that “we could be in the midst of a generational shift where money flows out of expensive application software companies, and back into those who run the infrastructure that writes software.” Echoing Andreessen, he titled his note, “AI Is Eating Software.”

It’s the grim picture that has overtaken the market in recent months, leading to descriptions of a software apocalypse. But unlike its smaller peers, Microsoft is built to weather this storm.

Cushioned by the Cloud

Microsoft’s cloud business, mainly its Azure unit that rents out servers over the internet, is booming. Revenue grew nearly 40% in the second quarter, boosted by seemingly insatiable demand for AI computing. The company says growth could have been even faster if not for a shortage of data centers. This fiscal year, Microsoft will spend in excess of $100 billion on capital expenditures to try to increase that capacity.

Thanks to Azure, Microsoft’s Intelligent Cloud segment will soon overtake business software as Microsoft’s largest revenue source. But the sales growth will come with lower margins because nothing can match software for profitability.

At the end of the day, though, AI doesn’t work without the cloud because agents require vast computing resources. In other words, if the software apocalypse happens, Azure will thrive. Microsoft wins either way.

The AI hedge

Azure is the first hedge against software disruption, and it’s expensive. But Microsoft’s second hedge is looking increasingly cheap.

OpenAI was founded in 2015 as a nonprofit dedicated to bringing free and open-source AI models to the world. It struggled to raise enough money to pay for the significant cloud computing required to train AI models. In 2019, OpenAI created a novel entity that could accept equity funding but was overseen by the nonprofit’s board. Microsoft was the first in, with a $1 billion investment.

OpenAI used the money to build ChatGPT, and less than two months after its debut, Microsoft invested another $10 billion. Those deals were mostly comprised of Azure credits, meaning Microsoft was getting an early investment into the AI start-up, while also building its own cloud. Together, Azure and OpenAI learned how to build AI infrastructure at scale, giving Microsoft a key head start in the AI revolution.

In the end, Microsoft committed a total of $13 billion to OpenAI. As OpenAI has raised more funds, its value has soared. Earlier this year, OpenAI announced a $110 billion funding round that included Amazon.com, Nvidia, and SoftBank Group. The deal valued OpenAI at $840 billion. Microsoft’s stake has been diluted along the way, but it’s likely sitting on an OpenAI stake worth more than $200 billion.

If the AI revolution plays out to the current script, Microsoft would be the largest shareholder of the world’s most important company.

Software lives on

For Microsoft bears to be right, a lot will have to go wrong at the same time. First, OpenAI would have to lose its AI pole position. (That’s not impossible: The internet’s big winners were once expected to be AOL and Yahoo!) Second, Microsoft’s Azure would have to lose sway inside the industry. As of now, it’s the No. 2 cloud player behind Amazon’s AWS—and it’s growing at a faster clip.

Finally, AI would, in fact, need to eat software. There’s not much evidence of that happening. The early indication is that AI will work with business software and not replace it.

Anthropic, the leader of the agent movement, gave a business-focused presentation last month that highlighted the use of existing software. It pitched agents as assistants that were really good at using Excel, PowerPoint, and other Microsoft applications. The moment caused investors to rethink software’s demise. Since then, the iShares software ETF has recovered some of its losses, and Microsoft stock has risen 5%.

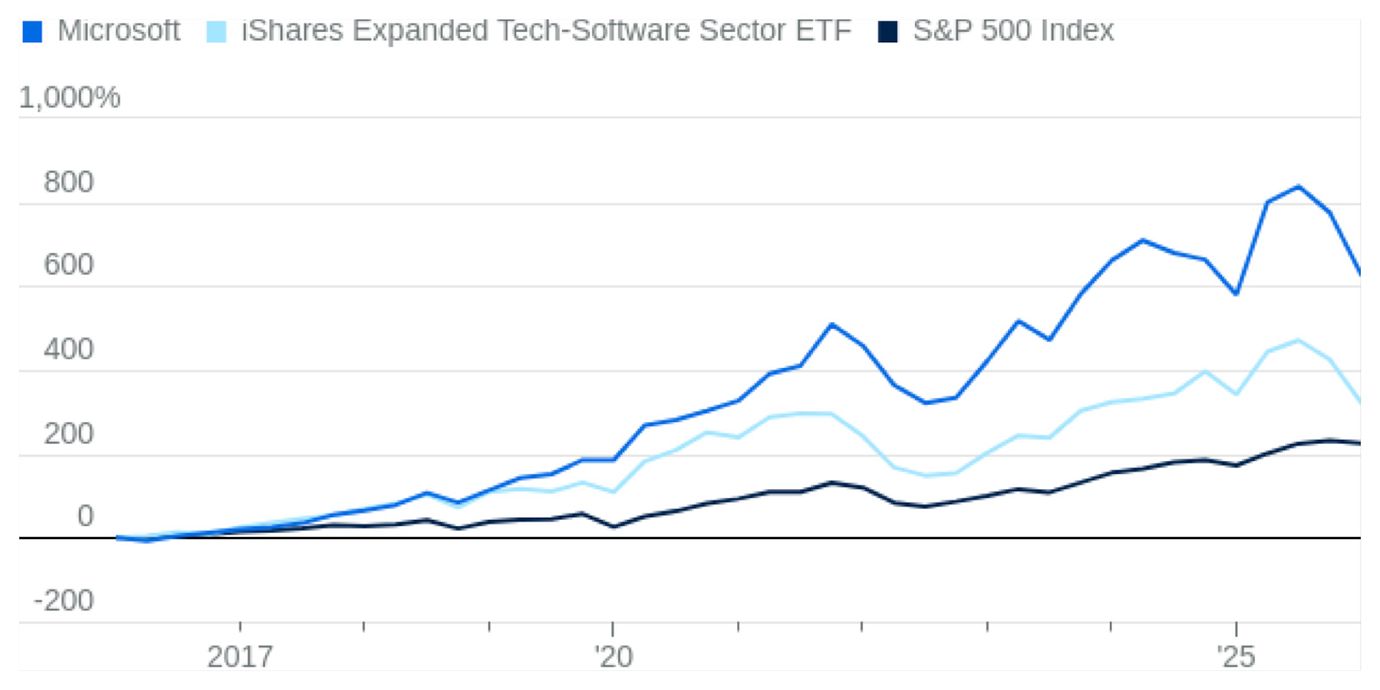

Microsoft’s Winning Decade

Over the past 10 years, Microsoft has easily outperformed not just the broad market but also its software peers.

Unlike the long-ago transition to the cloud, which undid many existing software firms, incumbents aren’t being complacent this time around. They’re acting as if their lives are at stake, and Microsoft is no exception.

The company has multiple AI initiatives across its business software, including its flagship product, a $30-a-month AI assistant for the Office apps named Microsoft 365 Copilot. It will soon add Agent 365, a platform for managing agents across an organization, and a new high-price bundle that combines all the AI services with Microsoft 365 and security services. Microsoft is doubling down on the subscription model.

After more than two years and a lot of hype, Microsoft 365 Copilot has 15 million paying users, 3% of its installed base. It’s a number that offers confirmation for both the bulls and bears. But in the long term, it may be irrelevant.

Microsoft always starts slowly and it isn’t much of an innovator. Instead, it just continuously iterates. “I was a Microsoft developer way back when,” says Jefferies software analyst Brent Thill. “The running joke in the community was, ‘The first product stinks, the second one’s better, and the third one’s where they get it right.’ ”

“It can take two to three years to build the software to make it stable,” Thill says. “It takes time to harden enterprise software.” At that point, Microsoft uses aggressive pricing and bundling, leveraging deep relationships with customers, to push it through multiple sales channels. In the end, Microsoft software and services bundles provide a lot of value, even as the price tag rises.

Says Charles Lamanna, Microsoft’s president for business apps, “What I tell my team: We need to build the best product at the best price, and we need to stay there for a long time. That’s how you are successful in this business.”

Microsoft’s five-decade history offers many examples of the slow-start pattern. Its Basic programming language and DOS operating system weren’t innovative in the market—but became standards. Word and Excel weren’t category leaders—until they were. Even Windows didn’t really change the world until the software’s fourth release. Microsoft was also late to cloud software, before doggedly making the pivot under CEO Nadella.

The only surprise now would be if Microsoft 365 Copilot were an instant hit. It may take a while for Microsoft to fully understand where its business software fits in the AI age, but it still has plenty of time, and it will find its footing.

Doing the Math

At the moment, the sentiment around Microsoft stock doesn’t add up. On the one hand, investors look at hundreds of billions of dollars in AI data-center capex from Microsoft—and the other hyperscalers—and see an investment bubble. On the other hand, they expect AI to be so powerful that it takes over all knowledge work, destroying the value of enterprise software.

Both can’t be true, and Microsoft is positioned to come out an AI winner in a range of scenarios, even if its software is challenged.

Reitzes, the Melius analyst who sees a rough road for software, recently downgraded Microsoft to Neutral, giving him a rare non-Buy rating on the stock. But much of the bear case may be priced in.

Microsoft’s stock trades at a forward price/earnings ratio of around 22, making it less prized than Coca-Cola, Home Depot, and Colgate-Palmolive. The last time Microsoft stock traded at this level, in January 2023, shares soared 73% over the next 12 months.

Relative to the S&P 500, Microsoft is the cheapest it has been in a decade.

At some point, Microsoft will stop being a narrative and start being a company again. When that happens, investors will rush to fix their math.