Svårare klättring väntar på börsen – aktier ändå toppval

Tech är inte den enda sektorn där värderingarna dragit iväg efter börsrallyt som avslutade 2023. Med några få branscher undantagna överstiger P/E-talen på sektornivå medianvärdena sedan 1999, skriver The Wall Street Journal.

Börsutsikterna framåt ser kärvare ut och investerare kan inte förvänta sig samma resa som de senaste tio åren. Men aktier pekas ändå ut som förstahandsvalet för långsiktiga investerare.

Can Stocks Surpass 2022 Highs? Yes, but the Math Looks Scarier From There

Though the equity market faces a much improved outlook, high valuations imply lower long-term returns

How will stocks perform in 2024? The only honest answer to the obvious New Year’s question is that we don’t know, but we can have some idea how they might fare over the coming decade.

The stock market last year recouped almost all the losses it made in 2022. This makes sense: A strong U.S. economy dispelled recession fears and inflation turned out to be mostly transitory after all. But the result is that nothing in the market looks cheap right now.

Indeed, the richly valued technology stocks that led the way in 2023 haven’t done well in the first few days of 2024. Despite a strong rebound Monday, the so-called Magnificent Seven—Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla and Meta—are down 0.9% this year, compared with 0.1% for the S&P 500. Meanwhile, cheaper “value” stocks are up year to date.

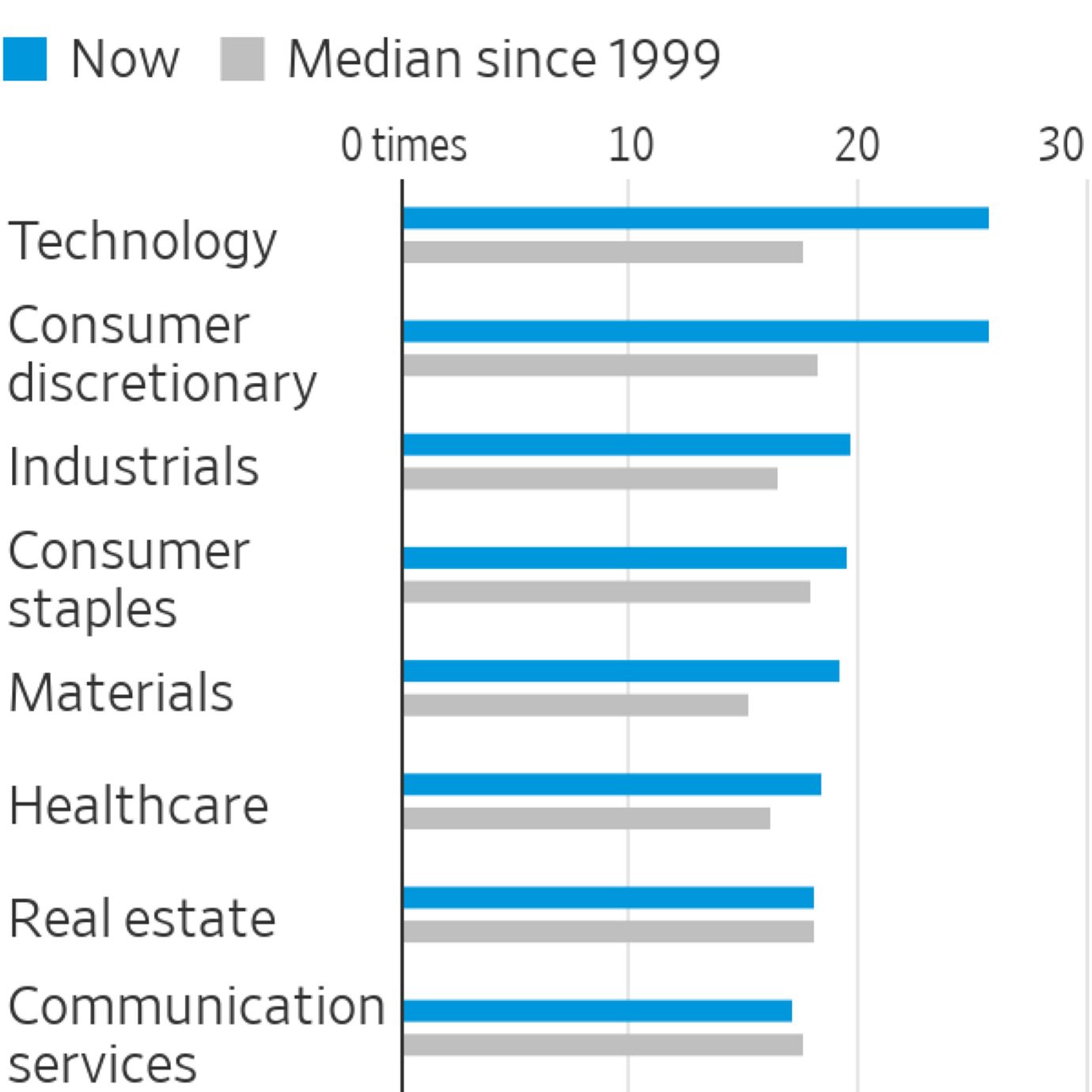

S&P Sectors, price/earnings ratio

Yet tech isn’t the only expensive sector. With the exception of energy, real estate and communication services, price/earnings ratios are above the historical median since 1999 across all S&P 500 industry groups.

The takeaway isn’t that a correction is necessarily coming, nor that 2024 will be a bad year for stocks or even the Magnificent Seven. Given how robust the economy is, the high-water mark reached by the S&P 500 on Jan. 3, 2022, may soon be surpassed. Valuations are notoriously bad at telling investors when they should sell equities.

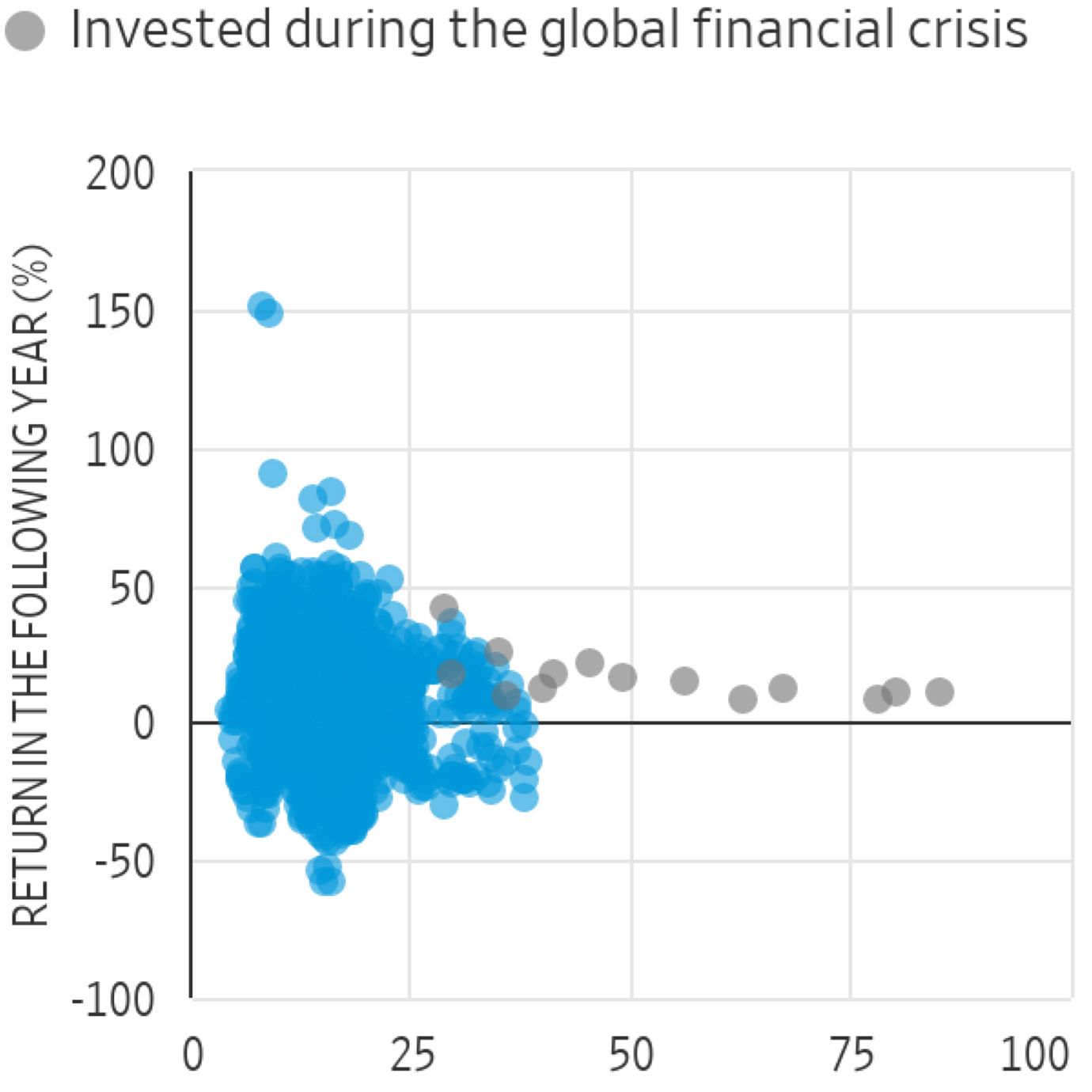

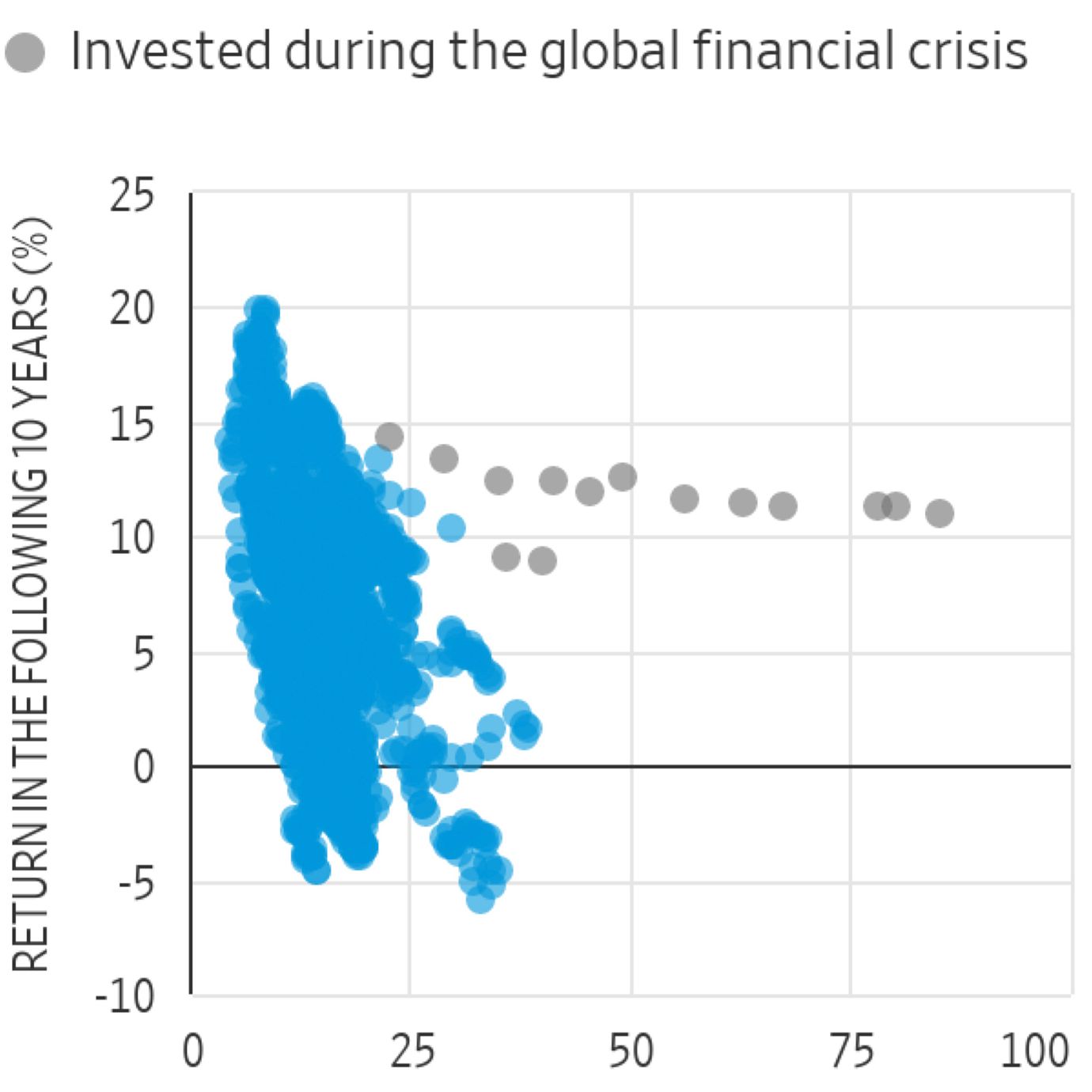

What price/earnings ratios are pretty good at predicting is the magnitude of long-term returns, as data collected by Yale University professor Robert Shiller for the U.S. stock market between 1871 and 2023 has shown.

Getting in at the start of an economic growth cycle usually leads to greater rewards. For example, investing in 1949 led to an inflation-adjusted annual compound return of around 19% over the following decade, as stock prices were late to catch up with a postwar surge in corporate profits. Similarly, those who scooped up dirt-cheap shares during the 1980 slump made 12% annual gains in the Ronald Reagan years. Conversely, purchasing overvalued equities in 1966 yielded a minus 0.4% annual return. Entering the market in years of mania, such as 1929 or 1999, led to big losses.

Valuations are a poor guide to where stocks will be in a year’s time...

...but a far better preditor of long-term returns

There are exceptions: Stocks did well following the 2008 financial crisis, because a colossal one-off drop in earnings misleadingly made valuations look expensive.

The difficulty of investing in 2024 is that the economy is technically emerging from a slowdown, but not really. The pandemic recession was deliberately engineered for health reasons, and the “stagflation” that was expected to follow it never happened. It is hard to know whether the global economy is at the start, the middle or the end of a cycle.

A parallel can be drawn with 2013, when a corporate upswing was also kicking off following an earnings rout. Investors who bought then saw the price of their stocks increase at a compound annual rate of 10% over the following decade, without adjusting for inflation. To deliver this, the broad S&P Composite 1500 had to go from trading at 17 times earnings to 23 times, as earnings only grew 8%.

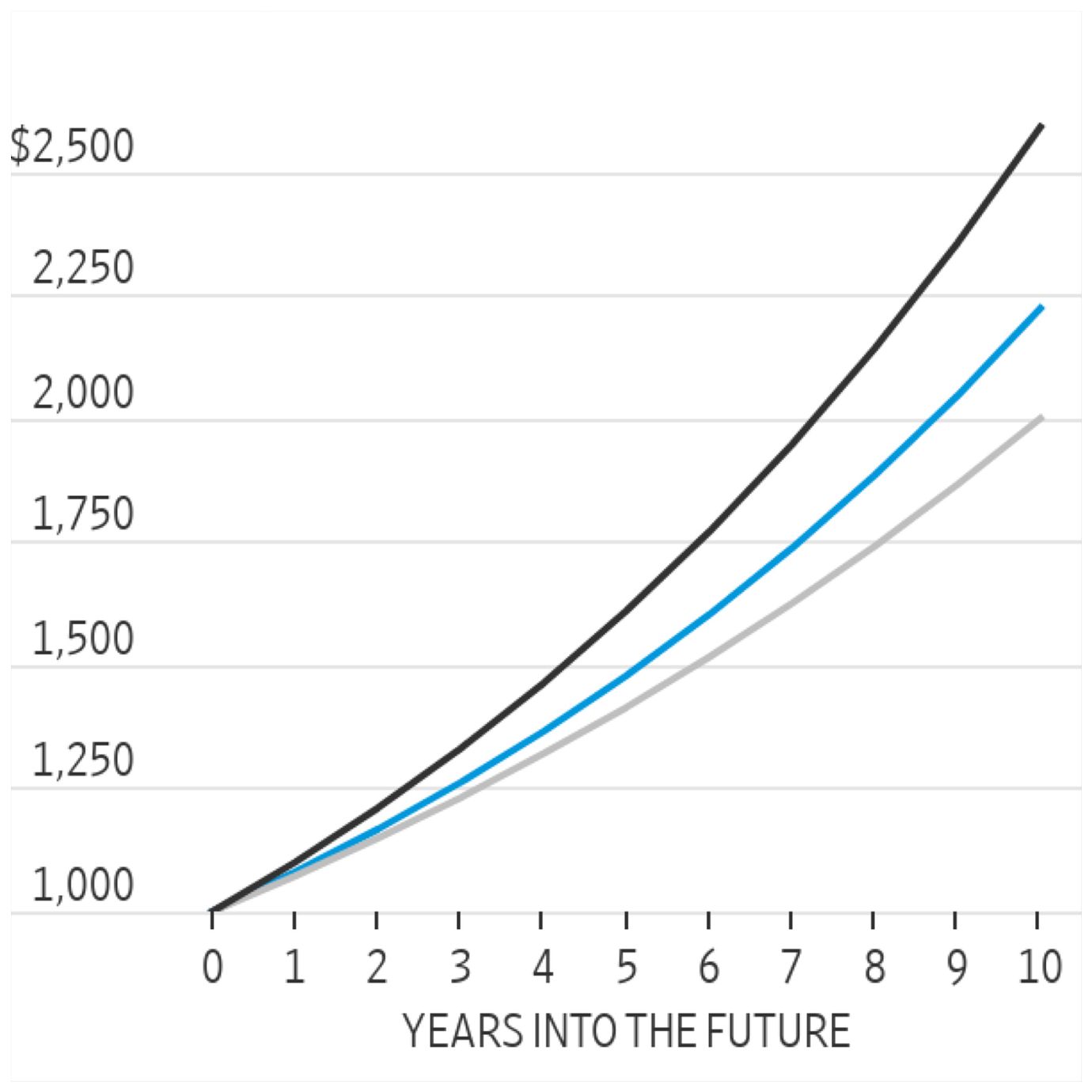

If you unvest $1,000 now, how much will you have in 10 years’ time?

Replicating this performance over the next 10 years would take valuations to a whopping 28 times. If earnings grow from their trough at the long-term historical average of 6%, valuations would have to climb to 32 times to achieve the same gains. History suggests they are much more likely to compress to around 21 times, which would imply an annual price return of 7% or less.

”Ultimately, stocks have no substitute in portfolios”

These are all benign scenarios that don’t involve market crashes. Yet the differences compound. Assuming 2% inflation, a household investing $1,000 now would expect to have $2,591 in “real” terms at the start of 2034 if stock prices and dividends rise as they did between 2013 and 2023. If markets instead perform in line with the average of the entire post-1871 period, the household would end up with just $2,000.

Ultimately, stocks have no substitute in portfolios. But savers should feel less excited about them than they have been over the past decade. It only takes some back-of-the-envelope math to understand why.