WSJ: Stjärnorna står rätt för tjurrally i bioteknikbolag

Efter flera år i skymundan, medan investerare jagat nästa stora trend inom AI och krypto, har bioteknik åter hamnat i fokus.

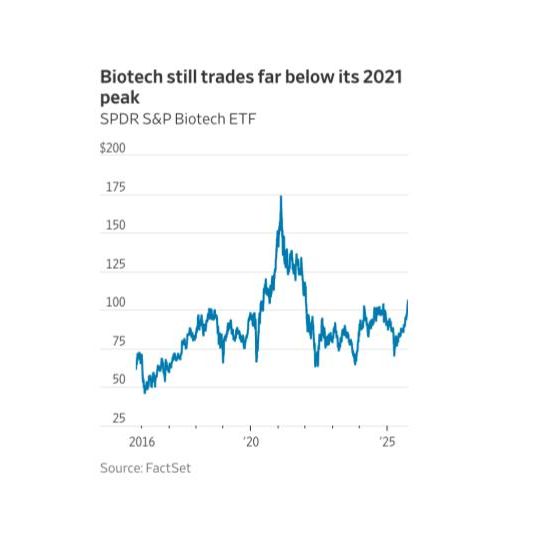

Flera faktorer pekar på att stjärnorna nu står rätt för ett tjurrally i sektorn: Dimman kring reglering tycks ha lättat, aktiviteten på M&A-marknaden har tagit fart och utrensningen av bolag som rusade under den mRNA-drivna bubblan 2020–2021 är i stort sett klar. Dessutom handlas sektorn omkring 40 procent under covidpandemins rekordnivåer.

Frågan är om uppgången signalerar en verklig återhämtning – eller bara ännu en kortvarig rekyl, skriver Wall Street Journal.

Why Biotech’s Rally Can Last This Time

The stars align for a bull run in the sector

After years on the sidelines while investors piled into the next big thing in AI or crypto, biotech is back in focus. The question is whether this rally marks a real recovery or just another short-lived bounce.

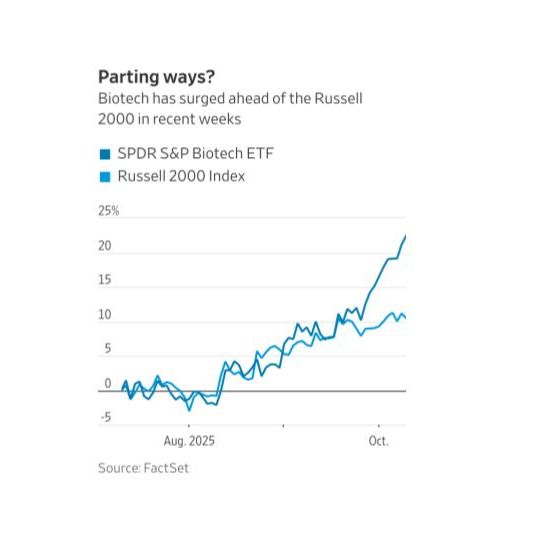

Despite its sharp rebound, the sector remains about 40% below its pandemic peak, leaving it as one of the few areas of the market that still looks reasonably priced. The SPDR S&P Biotech ETF has gained 19% in the past three months, handily beating the S&P 500’s 4% rise. That kind of outperformance has been rare lately.

Even after the rally, valuations remain grounded—the group is trading slightly below its historic average for the ratio of enterprise value to sales. Whether the run continues will depend on several factors: continued funding, a predictable regulatory environment, positive trial results, and steady deal activity. For once, those forces seem to be aligning.

The last thing I’d want to see as a public investor is too many IPOs happening too quickly. Slow and steady, with only quality coming in, is a good thing

Asad Haider, head of U.S. healthcare equity research at Goldman Sachs, notes that biotech had moved in lockstep with the Russell 2000 small-cap index for much of the year amid bets on the trajectory of interest rates. But that correlation has started to fade in recent weeks, with biotech surging ahead. That suggests there is more behind the rally than just hopes for lower rates.

First, some of the fog around regulation and politics has gradually lifted. After President Trump was elected, Health Secretary Robert F. Kennedy Jr. vaccine skepticism and his shake-up of federal health agencies initially rattled biotech stocks. Since April, says Daniel Lyons, a portfolio manager at Janus Henderson, investors have taken comfort from a steady drumbeat of Food and Drug Administration approvals, such as the recent green light for Insmed’s treatment for chronic lung disease.

Meanwhile, confidence has also improved for Big Pharma. Haider notes that in the two trading days in the wake of Trump’s recent drug-pricing deal with Pfizer, large drugmakers logged their biggest collective gain in 25 years. That kind of rebound matters: When pharma companies’ stocks rise, so does their appetite for acquisitions, which is the lifeblood of biotech.

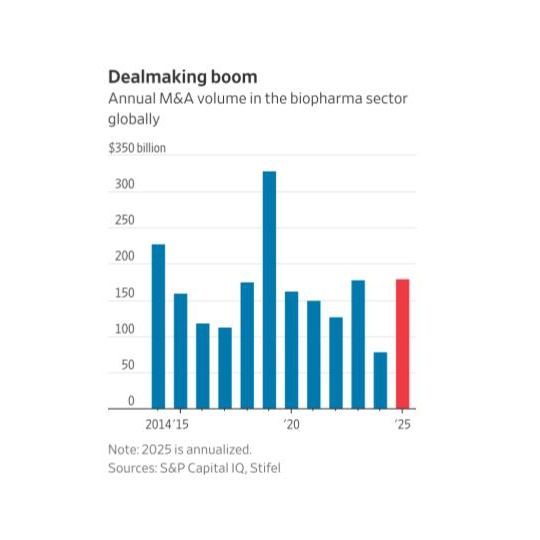

And deal activity has indeed accelerated. While there haven’t been any single transactions above $15 billion, global biotech M&A volume is on pace for its strongest year since 2019 at an annualized $179 billion, according to Stifel’s Tim Opler .

Recent examples include Pfizer’s purchase of Metsera and Novo Nordisk’s acquisition of Akero Therapeutics, both focused on the fast-growing cardiometabolic space. Proxy filings for the Metsera deal showed several suitors—evidence of just how hungry large drugmakers are for new pipelines as their big blockbusters lose patent protection.

Another tailwind is simple survivor bias. Most of the industry’s weakest players have finally been flushed out.

The ultralow-rate, mRNA-fueled bubble of 2020-2021 produced a wave of biotech initial public offerings—plenty of them questionable. In 2021 alone, 111 biotechs went public. Many had no viable products, but it took several years for them to close shop, merge or return capital.

Now, that shakeout seems largely complete. The number of listed biotechs trading below their cash balances has fallen from more than 200 in 2022-2023 to about 50 today, according to Stifel’s Opler.

There are other signs of discipline returning. Haider says layoffs across the sector in 2025 have already exceeded last year’s peak and are at the highest since Goldman started tracking the data. That is another sign, he says, “of the froth coming out the other side.”

The backdrop for science itself is also improving. Clinical results have been strong in areas investors had written off, such as gene editing and gene therapy, Lyons of Janus Henderson points out.

When uniQure announced a successful trial for the fatal neurological disorder known as Huntington’s disease, its stock shot up, lifting assets across the highly shorted sector. Those kinds of catalysts can create a virtuous cycle—squeezing short sellers and attracting fresh capital. Shares of uniQure, for instance, are up nearly 1,000% over the past 12 months.

Despite the surge in stock prices, brisk dealmaking and renewed access to capital, the IPO market remains subdued. Biotech companies are on pace to raise $2.6 billion from IPOs this year, compared with $27 billion in 2021, according to Stifel.

That restraint might actually be healthy. “The last thing I’d want to see as a public investor is too many IPOs happening too quickly,” says Jared Holz, a healthcare strategist at Mizuho. “Slow and steady, with only quality coming in, is a good thing.”

No one can time biotech’s daily fluctuations. But for the first time in a while, both the science and the sentiment are pointing the same way, and if the market keeps chasing affordable risk, the sector’s rebound may still have legs.