Barron’s: Pfizer, Amazon och 25 andra aktiefynd just nu

När det råder turbulens på börsen är det dags att fynda. Barron’s har bjudit in fyra investeringsexperter till ett djupgående rundabordssamtal, där de delar med sig av sina 27 bästa aktiekap just nu. Bland favoriterna finns e-handelsjätten Amazon och vaccinutvecklaren Pfizer, men också bolag verksamma inom elbilar, livsmedel och solenergi.

– Det finns inget enklare sätt att tjäna pengar än att köpa ett bra företag som pressas på grund av kortsiktiga problem, konstaterar David Giroux, investeringschef på T Rowe Price.

It’s Time to Bargain Hunt. 27 Picks to Beat the Stock Market From Barron’s Roundtable Experts.

“There is no easier way to make money in the market than to buy a great company under pressure due to short-term concerns.” So said the newest member of the Barron’s Roundtable, David Giroux of T. Rowe Price, at our annual gathering on Jan. 10, on Zoom. For better—and worse—there’s plenty to choose from these days, given a market selloff that has dragged the Nasdaq Composite into correction territory, and shows no sign of ending.

Lauren R Rublin, Barron’s, January 23 2022

In this week’s second 2022 Roundtable installment, Giroux highlights six stocks that, to his mind, have been unfairly punished. He’s joined by Gamco’s Mario Gabelli, Henry Ellenbogen of Durable Capital, and Abby Joseph Cohen, formerly of Goldman Sachs and now a professor of business at Columbia University’s Graduate School of Business, all of whom present their own best bets for the year ahead.

Consider these investment ideas the silver lining in the cloud that now darkens financial markets. The edited conversation below has the full details.

Barron’s: Mario, what appeals to you this year?

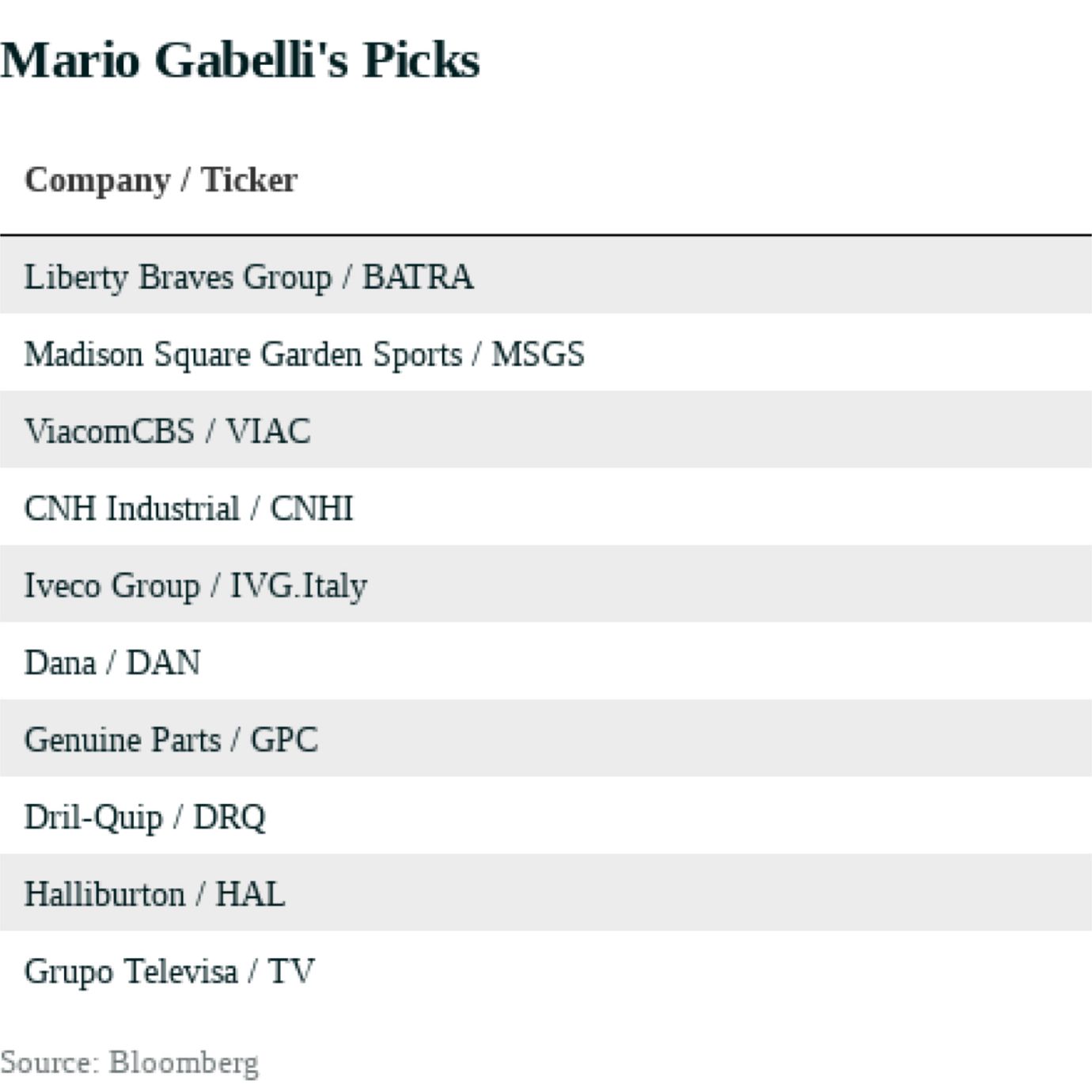

Mario Gabelli: I’ve been talking about the Atlanta Braves for a while. They won the World Series last year, an extraordinary turn of events. You can invest in the Braves through Liberty Braves Group [ticker: BATRA], a tracking stock controlled by John Malone’s Liberty Media. It trades for $28, and there are 60 million shares outstanding. The company also owns the land around Truist Park, where the Braves play in Atlanta.

We estimate the team and the land could be sold for around $40 a share, with $2.5 billion for the baseball team and $600 million for the real estate operation. The short-term opportunity for Liberty Braves is that Georgia is one of the few states that hasn’t legalized online gaming. If it does, that could be an incremental game changer for sports-related companies in Georgia. The short-term speed bump is centered on Major League Baseball and players’ union negotiations.

I’m always optimistic about the New York Knicks, and we still like Madison Square Garden Sports [MSGS], which is trading around $170 a share. When Jimmy Dolan [whose family controls the voting stock] finishes building the MSG Sphere in Las Vegas, we think he’ll sell Madison Square Garden Sports. The company could go for 20% to 25% more than the current share price in the next two years.

What else do you like?

Gabelli: ViacomCBS [VIAC] has 650 million shares outstanding, trading at $35 apiece. The company is controlled by National Amusements through the ownership of voting stock controlled by Shari Redstone. It is run by Bob Bakish.

ViacomCBS has approximately $12 billion of net debt, but is selling CBS Studios Center in Los Angeles. ViacomCBS has an equity market capitalization of $25 billion. This is a pittance, a morsel, for a larger company that wants to get into the content-creation business. The question is: What would motivate Shari Redstone to sell?

ViacomCBS could have revenue of around $30 billion this year. Ebitda [earnings before interest, taxes, depreciation, and amortization] is about $5 billion. If I were to advise Bob Bakish on what to tell Shari, I’d say spin off the TV stations. There are many ways to monetize the value of ViacomCBS.

He’d be happy to hear from you.

Gabelli: Shifting gears, rising crop prices are providing a tailwind to farm-equipment companies. CNH Industrial [CNHI] trades around $16. It recently spun off Iveco Group [IVG.Italy], a truck and powertrain manufacturer that I’m also recommending. Agriculture accounts for about $16 billion of CNH’s revenue, and construction machinery, about $3.5 billion. It will benefit from the passage of the infrastructure bill. Finance operations contribute another billion dollars in revenue. We see earnings accelerating over the next two years, from $1 to $1.30-$1.40 a share.

CNH holders got one share of Iveco for every five shares of CNH. Iveco is selling for around 10 euros [$11.34] and has about 270 million shares. It has about $1 billion of cash. Exor [EXO.Italy], the Agnelli family’s holding company, owns 25% to 30% of the stock. Iveco has an 8% market share in European Class 8 trucks and a 17% to 20% share of the bus market in Europe.

In the U.S., there are one million cars in inventory on dealer lots, down from three million typically. Prices are going up. The rental-car companies and the fleet buyers will have to replenish their fleets at some point. As a consequence, light-vehicle production will have to rise in excess of sales for the next two years to normalize cars on dealer lots. This benefits suppliers of original equipment components and systems.

We like Genuine Parts [GPC] and Dana [DAN]. Both companies have 144 million shares outstanding. I wouldn’t have mentioned Dana, although the CEO has done a good job, and free cash flow is going to surge. They’re going to earn $3.50 to $4 a share in free cash flow over the next two years, compared with supply- chain-affected cash flow of $90 million or so in 2021. But Carl Icahn knocked on Dana’s door about a year ago and got two seats on the board in an agreement last week [Jan. 7]. His ownership stake is limited to 20%. Icahn has complemented the work accomplished thus far by CEO Jim Kamsickas, as Dana utilizes the cash flow from its core driveline business to position the company for the next-generation vehicle electrification technologies.

”Next, we need to focus on the Earth and its climate”

Why do you like Genuine Parts?

Gabelli: The company benefits from inflation. If there are 270 million cars on the road and the average age is just under 13 years, they will need repairs. The price of auto parts has been relatively flat for the past 10 to 15 years. Genuine sells $13 billion a year of auto parts. If its price for the auto parts it sells goes up 3% or 4% and mix and gross margins are relatively constant, it will have higher revenue to cover more controllable selling, general, and administrative expenses. The same is true for AutoZone [AZO] and O’Reilly Automotive [ORLY]. The difference is that Genuine uses LIFO [last in, first out] accounting for its U.S. auto-parts business. The use of LIFO defers payment of taxes on profits bolstered by inflation, as the low cost attached to inventory is kept on the books.

Earlier this month, Genuine bought Kaman Distribution Group, which sells industrial and automation parts. This business should help add automation to its operations. We think Genuine Parts could earn $7.50 a share this year, compared with $6.70 in 2021, and over $8 in 2023. The stock is at $138.

Next, we need to focus on the Earth and its climate. In the short term, we need to have adequate natural-gas and oil reserves to meet demand. Current estimates for global consumption are 100.6 million barrels of oil a day, and global production is 100 million barrels a day. About 10% of the supply that has to be replaced yearly reflects declining production rates. Since the industry has underspent for the past five years, capital spending has to catch up. Global exploration-and-production capital expenditures for this year are projected to be around $355 billion, up 18% from 2021, but still down from peak spending of nearly $710 billion in 2014.

What are your energy plays?

Gabelli: I am recommending Dril-Quip [DRQ] and Halliburton [HAL].

Dril-Quip has 35 million shares. At $22, down from $60 a share, it has a market cap of $770 million and no debt, plus $10 a share in cash. It makes wellheads and other products for offshore wells, and a shallow-water wellhead that has potential for carbon capture and sequestration. Expect to see higher offshore activity in 2022; Drip-Quip will benefit. The company should report losses for 2021 and 2022, but will enjoy a surge to $2 per share in earnings 24 months from now.

Halliburton has 890 million shares outstanding. At $26, it has a market cap of $23 billion and $6.5 billion of net debt. Industry capacity has finally been rationalized, so with higher activity levels this year, Halliburton can push through higher pricing and generate more free cash flow. It is focused on reducing debt and improving its financial flexibility. I look for earnings of $2 a share for 2023, up 25% from $1.60 this year.

Lastly, Grupo Televisa [TV] serves the Hispanic market. The stock trades for $10, and the company has 560 million shares. Grupo Televisa has been in front of the Federal Communications Commission for about nine months seeking approval for the merger of its content operations into U.S.-based Spanish-language programmer Univision. Grupo Televisa will own 45% of Univision if the merger goes through. You can buy Televisa’s Mexican cable and satellite business for six times Ebitda, and get 45% of Univision, which is likely to go public within a year, for free.

Thanks, Mario. Now, let’s hear from Henry.

Henry Ellenbogen: I look to invest in companies with a strong core business that have executed well and demonstrated an ability to invest in their next growth application. If you aren’t both executing and investing for the future, you are moving backward. Second, these companies have good cultures. Their CEOs exemplify what we think of as an ownership mentality. Third, we believe these companies will benefit from what the world is going to look like postpandemic.

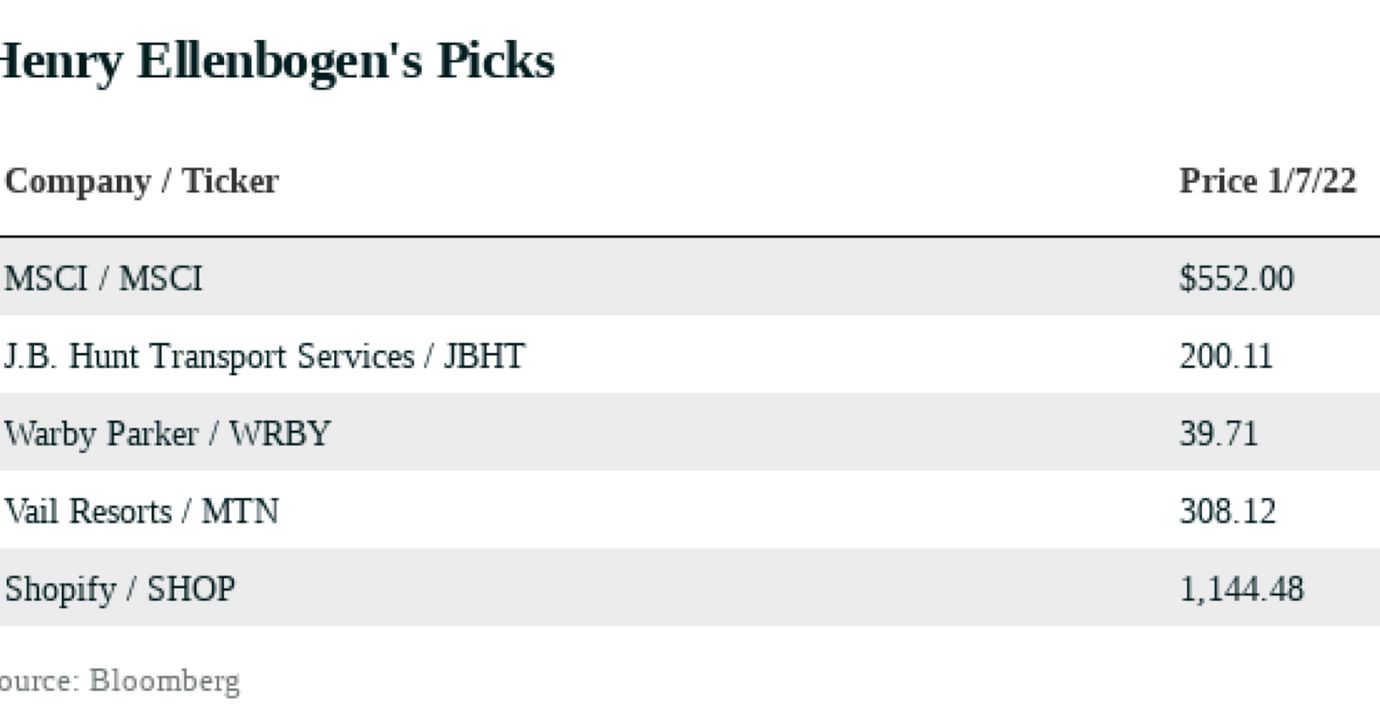

MSCI [MSCI] has been public since 2007, and the stock has compounded at well above 20% a year since its initial public offering. MSCI’s primary business is the creation of stock indexes that have become standards for measuring global equity performance. Its indexes also determine holdings of exchange-traded funds representing $1 trillion of assets under management.

Over the past 12 years, MSCI has also built a leading ESG [environmental, social, and governance] and climate franchise that includes research to assess a company’s ESG impact, tools to measure portfolio exposure to climate risk, and indexes based on ESG factors. ESG and climate risk are increasingly important factors in driving investment decisions. MSCI’s revenue from its ESG and climate business segment is now 6% of the total and growing at 50%-plus rates.

What is the outlook for the rest of the business?

Ellenbogen: The traditional global index and research business is another 60% of revenue, and growing annually by double digits. Both segments (traditional market-weighted and ESG) benefit from the continuing trend toward investing through ETFs, which are an inexpensive way to express investment views. ETF assets under management account for roughly 15% of industry assets and will continue to gain share. Investors increasingly talk about double-bottom-line investing. MSCI offers an example, as its ESG and climate franchise, and its ETF business, both will continue to gain share. ESG ETFs accounted for roughly 20% of ETF inflows in 2021. In Europe, ESG ETFs represented roughly 50% of ETF inflows. MSCI indexes have about a 70% share of ESG and climate-related indexes’ assets under management.

MSCI’s CEO, Henry Fernandez, embodies an ownership mind-set. He has been CEO of MSCI since before its spinout from Morgan Stanley [MS]. We think MSCI can earn roughly $17 a share in 2023 and that the stock can compound in line with high-teens earnings growth.

Todd Ahlsten: We own S&P Global [SPGI]. Can you unpack the margin opportunity for MSCI?

Ellenbogen: S&P is a terrific franchise. MSCI is much more of a pure play on index creation, and has had a significant head start in ESG and climate risk. Because MSCI is investing so aggressively in this segment, we don’t see a lot of margin expansion. But we encourage that investment.

My second pick is J.B. Hunt Transport Services [JBHT]. For any company in transportation or supply-chain logistics, 2021 was a true test of operating ability. J.B. Hunt exemplifies excellence. It has built two market-leading segments: intermodal and dedicated contract services, or DCS. The company also offers brokerage services. Underlying these businesses is a terrific culture.

We are particularly excited about DCS, which contributes $2.6 billion of revenue and is 30% of Ebit [earnings before interest and taxes]. J.B. Hunt provides outsourced transportation ownership and management of truck fleets, and focuses on companies with five to 25 trucks. It estimates it can save customers 10%, versus internal solutions. It is the only scaled player in this segment. Its DCS business has a customer-retention rate of 98%.

J.B. Hunt is also the No. 1 player in handling intermodal freight [freight carried by rail and truck], with a 40% market share. Intermodal accounts for about 60% of Ebit. Historically, this segment has grown at double GDP [gross domestic product]. The intermodal segment has had an inconsistent financial profile in recent years, but some of the headwinds have reverted, and rail service should continue to improve. Intermodal could be a double-digit growth segment for the next several years.

J.B. Hunt started investing aggressively in digital brokerage in 2018. It can now offer customers a full service between its own and third-party assets. We see J.B. Hunt earning about $10 a share in 2023, and believe the stock will trade at 25 times earnings.

”The result is an attractive retail industry that sees consistent price inflation”

Scott Black: More than 60,000 truckers have resigned in the past five years. Is J.B. Hunt having trouble finding drivers?

Ellenbogen: One reason the DCS business saw 20% growth last year is because small and midsize companies are having trouble finding and retaining drivers. These companies are increasingly converting their fleets to J.B. Hunt’s DCS business. One of J.B. Hunt’s core competencies is recruiting, training, and retaining drivers, and its retention rate widened relative to the industry last year.

Moving on, 2021 saw about 300 traditional IPOs. About two-thirds of the IPOs ended the year below their offering price. Warby Parker [WRBY], my next pick, stands out to us. It was founded in 2010 and came public last year. It is run by two exceptional founders/co-CEOs, Neil Blumenthal and David Gilboa. We have known the company well since 2014.

Warby is an omnichannel retailer selling eye-care, including glasses and contact lenses. The U.S. market for glasses, lenses, and eye exams is about $35 billion, and has seen consistent growth driven by two things. One is the strain of digital devices on the eyes, and the aging of the population, which requires more glasses. Second, the industry’s structure has been codified as a two-step distribution model due to EssilorLuxottica’s [ESLOY] consolidation of the market and the lobbying efforts of optometrists. The result is an attractive retail industry that sees consistent price inflation. Warby’s direct-to-the-consumer model allows it to sell glasses at roughly half the price of its relevant competitors. The growth is just getting started.

We estimate Warby will report about $550 million in 2021 revenue. Its market share is less than 2%. In the next three years, we see 30% annual growth, driven by the addition of 20% more stores a year and same-store sales growth of close to double digits. The company is free-cash-flow positive. Physical retail accounts for about 60% of sales, and online, 40%. Strong unit economics are going to improve because Warby is adding optometrists to its stores. Historically, customers have had to bring in third-party prescriptions. The company has 160 stores and could grow to more than 600 stores. Warby Parker could sell at 30 to 35 times Ebitda, resulting in a stock price of about $79 in two years, up from less than $40 today.

I first mentioned my next two picks at the 2018 Roundtable. The best companies execute on their core business and also invest in additional growth. Vail Resorts [MTN] is an example. I talked earlier today about two pandemic-related changes that are here to stay: Many knowledge workers can now work remotely, and the U.S. population is undergoing a migration. Many people are heading to the mountain states. Vail benefits from these trends, and from declining supply. There are 15% fewer ski resorts in the U.S. today than in 1990.

There are about 10.5 million Americans who ski, and they ski, on average, five to six times a year. As people have more flexibility, the number of high-quality ski days could more than double. Vail transformed the industry by lowering the cost of a season pass. A second company, Alterra, also reduced the cost of its season pass and created a competitive environment for a few years. Last year, Vail announced it was reducing its season pass by 20%, but Alterra didn’t follow suit because it doesn’t own many of the mountains on its pass.

The last part of our thesis is Vail’s management team. Former CEO Rob Katz became executive chairman last year, and Kirsten Lynch, who built the company’s world-class direct-marketing capabilities and turned Vail into a data-networking company, became CEO. We think she will continue to do an excellent job.

Tell us about Vail’s valuation.

Assuming no change to industry growth, Vail can support midteens cash-flow growth. In that case, free cash flow should total about $19 a share in 2023. If the stock trades at around 20 to 25 times free cash flow, that gets you a $400 to $450 stock. If our demand-growth thesis works out, free cash flow will be closer to $21 a share and the stock could trade for 25 to 30 times free cash flow. That implies a price of $525 to $600.

David Giroux: Can you talk about the outlook for capital allocation? Is there still a lot of opportunity for acquisitions?

Ellenbogen: The capital-allocation story isn’t as strong as in the past, as fewer big assets are independent. But when Vail buys something unique, it not only makes the asset more valuable, but the asset also makes the company more valuable. In December, it bought Seven Springs in Pennsylvania for $125 million. We like the deal.

In the period between Delta and Omicron, we got a glimpse of a normal future. In third-quarter 2021 earnings, you can see the underlying growth power of many companies. Shopify [SHOP] distinguished itself in this environment. It’s two-year compounded growth rate was 70%. In 2018, I pitched Shopify as an early-stage growth company with the potential to be much larger. At that time, U.S. e-commerce was a $500 billion business, growing 14% a year. Amazon.com [AMZN] had a 32% share, and Shopify had only 3%. Four years later, e-commerce has grown to $900 billion. Amazon has gained nine share points and Shopify has gained eight, so it now has about 11.5% of the market. We believe Shopify will truly become a platform company.

Meaning what, in this case?

Ellenbogen: Increasingly, e-commerce companies are switching their internal or third-party platforms to Shopify. The company is highly profitable while also growing rapidly. Shopify has transitioned from an e-commerce seller service to an omnichannel company. Its GMV [gross merchandise value] in the third quarter of 2021 was up 35%. We estimate that Amazon’s U.S. GMV was up 11%. Shopify’s POS [point of sale] system has more than doubled its addressable market in the U.S. Thirty percent of its revenue this year will be outside of North America.

Increasingly, e-commerce isn’t happening on websites. It is happening on social-media sites, such as Facebook, Instagram, and TikTok. Shopify has become the platform that social-media influencers use to serve their customers. This could become a major growth driver in the next couple of years.

Shopify’s take rate is only 160 basis points [1.6%]. New product offerings will allow Shopify’s revenue to grow much faster than GMV. One example is Shopify Payment, Shopify’s answer to PayPal [PYPL]. PayPal has been around for more than 20 years. It had 400 million users in the latest quarter. Shopify Pay had 120 million. PayPal’s valuation is 50% higher than Shopify’s. Shopify could have close to $4 billion in revenue in 2024. It is scaling toward long-term margins of 40% to 45%. We believe it should trade at 30 to 40 times underlying Ebit, resulting in a price target of $1,350 to $2,000, compared with a recent $1,144.

Last year, you recommended Vroom and Boston Beer. Both stocks did poorly. What should investors do now?

Ellenbogen: I would hold on, for different reasons. Although Boston Beer gained share last year in the hard seltzer category, the category didn’t grow as we expected. Long term, this has been an excellent company, driven by a culture of innovation and strong channel distribution. We see some interesting innovations coming.

I pitched Vroom as an early-stage growth company that we thought could be a strong No. 2 to Carvana [CVNA] as an e-commerce platform for used cars. Vroom had inconsistent execution and has improved its management team. Although 2022 is likely to be a tough year in the used-car market, the stock has an attractive valuation, and we believe there is room for multiple players.

Thanks, Henry. David, you’re next.

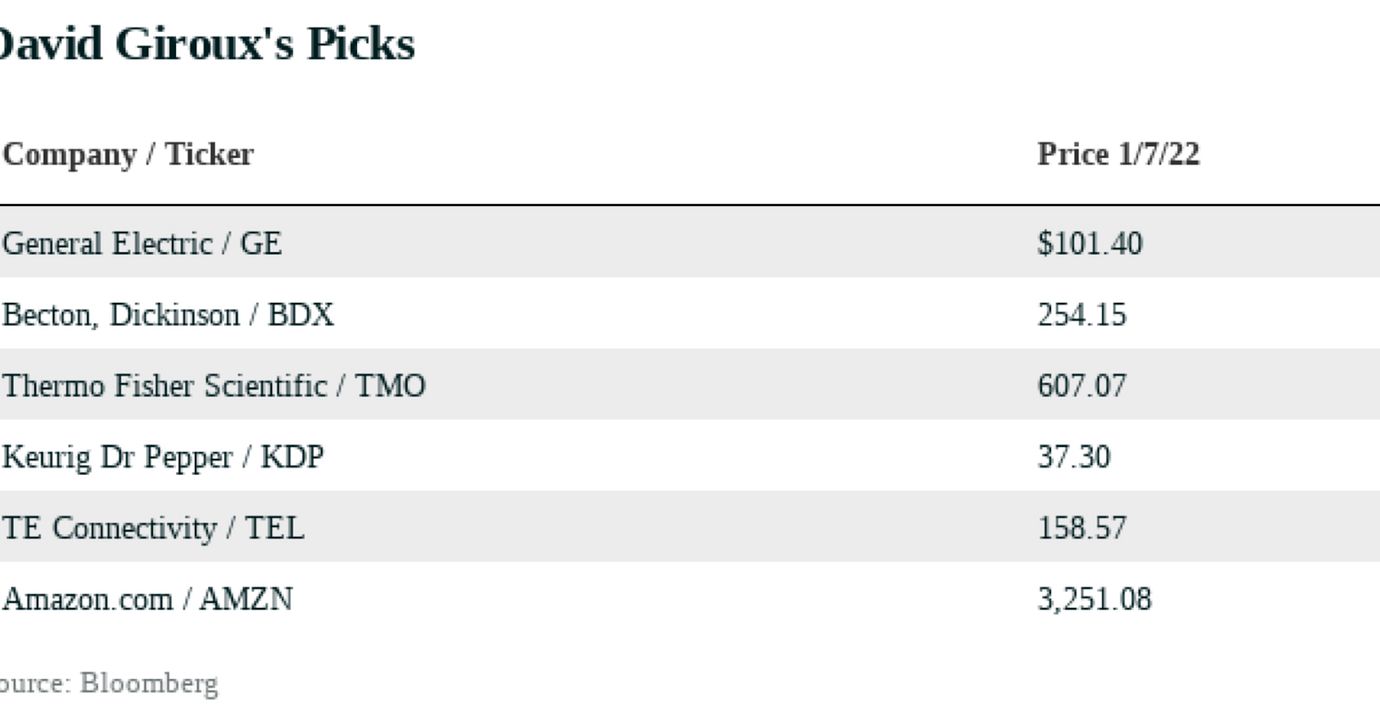

Giroux: We look for companies that deploy capital well, generate lots of free cash flow, and have strong management teams. We like stocks that are out of favor due to short-term concerns. I began following General Electric [GE] in 2003 when it was the largest company in the S&P 500 index. By 2018, the company wasn’t even in the top 50. A big reason was poor capital allocation. GE has struggled because of the impact of Covid on its largest business, aerospace. That has obscured a powerful turnaround, a vastly improved balance sheet, and massive simplification of the business.

GE’s aerospace business tends to grow faster than most industrials. In 2024, as in 2019, we expect 90% of the segment’s earnings to come from less-cyclical aftermarket and military profits. GE Aerospace is a market-share gainer. It has a much healthier engine-installed base than peers.

Where should GE Aerospace trade today, or in a couple of years? The average industrial conglomerate is trading for 24 times the next 12 months’ earnings. The median is at 22 times. I always underwrite a conservative case, so let’s say the business can trade for 23 times $4.50 a share in future earnings. That gives you a value of $103 a share. But it could easily trade for 25 times $5 a share in earnings, and be valued at $125.

GE is planning to spin off its healthcare and energy businesses in the next two years. How do you value them?

Giroux: The healthcare business is improving, relative to several years ago. Margins are higher, and the management is stronger. The business could see 10% earnings-per-share growth, with strong margin growth for the next five years.

For every dollar of net income, GE’s healthcare unit generates more than a dollar of free cash flow. Most medical-device and capital-equipment companies have 60% to 80% free-cash-flow conversion. The unit’s high-quality earnings could support a higher multiple. Long term, the business will acquire businesses with faster growth and higher recurring revenue. Organic growth should be 4% to 5%. We think the spun-off healthcare business will trade around 20 times earnings of $2.22 a share in 2024, yielding a $44 value in two years.

People aren’t paying enough attention to the power and renewables business. We think it will earn about $1.80 a share in 2024, and trade for 15 times that. The multiple assumes the power business is worth five times Ebitda, and the renewables business, 14 times Ebitda. That gets you to about $27 a share. Combine the value of GE’s businesses, back out $15 a share of pension deficit and long-term-care-insurance future cash outflows at the end of 2023, and the sum of the parts could be $160 a share in two years, reflecting 60% upside.

My next pick, Becton, Dickinson [BDX], was a blue-chip healthcare stock a few years ago. Earnings grew about 10% a year. The stock traded at a 15% to 20% premium to the market.

Then what happened?

Giroux: Becton acquired C.R. Bard in 2017 for $24 billion and levered up about 4.5 times. But the wheels came off for other reasons, including foreign-exchange issues and some dilutive divestitures. In the past two years, surgical volumes have been hurt due to Covid. Becton had to take its Alaris infusion pump off the market in February 2020 due to required remediation. Its diabetes business declined. Because of the leverage, it couldn’t grow through bolt-on acquisitions. We recently re-engaged with the stock.

Becton is spinning off the diabetes business, which should push the organic growth rate closer to 6%. Leverage has fallen to 2.6 times, and it is doing more M&A. We expect the Alaris pump to be back on the market at the end of this year, which probably adds about $300 million of high-margin revenue in fiscal 2023 and ’24. And if Covid becomes more endemic, Bard’s core surgical-products business can return to 6% organic growth.

We see Becton’s profit margins expanding, which will support double-digit earnings growth. The stock, at $255, looks cheap on a price to free cash flow and earnings basis relative to the market and peers. Sentiment is bad, which I like, and backward-looking. The core business could earn $17 a share in fiscal 2026, and the stock could compound at a 13% to 15% annual rate in the next five years.

Todd recommended Danaher [in the first Roundtable issue]. It is a great company, but I am recommending Thermo Fisher Scientific [TMO]. Two megatrends are driving life-sciences companies. The first is the move from small-molecule drugs to more biologics [drugs made from biological materials] and the growth of gene therapy and mRNA. All require intensive use of life-sciences tools, and are in an early stage. Second, small biotech and pharma companies are taking share from larger companies, and they tend to outsource more services and production, which benefits Thermo. The stock has sold off on the misguided view that the company won’t do as well if Covid becomes more endemic.

What don’t the skeptics see?

Giroux: Thermo has said it expects to earn $31 to $32 a share in 2025. Prepandemic, the market perceived Thermo as a company with organic revenue growth of 6%. It traded at a 125% premium to the market. Today, due to acquisitions and internal investment and a shift to faster-growing businesses, it is capable of 8% organic growth per year, and midteens growth in earnings per share. Yet it is trading around a 23% premium to the market. Thermo’s earnings are growing at twice the market’s organic growth rate, and the company has below-average cyclicality. Outside of large-cap tech, very few companies have this sort of profile. Plus, Thermo has one of the best CEOs I have encountered. We think the stock could gain a high-20s multiple and has 50% upside over the next three years.

Keurig Dr Pepper [KDP] is my favorite consumer staple. It was created by the 2018 merger of Keurig Green Mountain and Dr Pepper Snapple Group. Despite higher inflation, it has met or beat the financial targets set at the time of the merger. KDP has some of the best brands in carbonated soft drinks.

The coffee business is one of the fastest-growing in consumer staples. Former Keurig management had a flawed strategy of keeping coffee-pod prices artificially high and keeping Keurig a closed platform. The new management team took prices down, removed costs, and signed long-term agreements to manufacture pods for other coffee companies. Lower pod prices have driven consumer adoption. In 2015, about 22 million people were using the Keurig system. Now there are 33 million users.

Abby Joseph Cohen: There is an expectation on the part of commodity producers that coffee prices are going to move notably higher this year. What is the potential impact on KDP?

Giroux: They don’t buy coffee for partners; they package it in the pods. Higher prices won’t hurt their profit margins. As for demand, the average pod price is below 50 cents now, so if it goes up a few cents, that is still a better deal than buying coffee at Starbucks [SBUX].

KDP basically has the same algorithm as Coca-Cola [KO] and PepsiCo [PEP], with mid-single digit revenue growth that translates into high-single digit EPS instead of profit growth. Yet, it trades for a 10% to 15% discount to Coke and Pepsi. Free-cash-flow conversion of 100%-plus is much better than at Coke and Pepsi, and unlike those companies, KPD has excellent capital allocation.

KDP has four areas of optionality. The company has a $53 billion market cap and should be added to the S&P 500 within the next two years. Also, a joint venture between KDP and Pepsi on the distribution of carbonated soft drinks would benefit shareholders of both. Third, more Keurig coffee systems will be connected to the internet in time, allowing for more automated ordering. That would create more value for the ecosystem and potentially a new revenue source for KDP. Finally, KDP has $4 billion of excess capital it can deploy in the next three to four years. We expect the stock to rise 30% in the next two years.

”There is no easier way to make money in the market than to buy a great company under pressure due to short-term concerns”

TE Connectivity [TEL] is a great way to play the growth of electric vehicles. About 50% of its business is in the transportation segment, and the majority of that is highly proprietary connectors for the automotive market. TE’s content per vehicle is roughly two times more for EVs than internal-combustion vehicles. If you believe the industry’s bullish projections, their content per vehicle could accelerate beyond a current 5% to 6% growth rate. In the next decade, autonomous driving could provide another boost to the business.

TE has exited the more-volatile, lower-margin connector business for mobile phones and sold its undersea-cable business. They’ve built a fast-growing sensor business, a medical business, and a high-end connector business focused on the cloud. They also have a growing connector business focused on renewables.

Margins have improved, along with free-cash conversion, which is now around 100%. TE used to trade at about a 10% discount to the market. Today, it trades at about a 5% discount, based on fiscal 2023 estimated earnings. But the business is so much better today than five or 10 years ago. TE’s closest peer, Amphenol [APH] trades for 28 times 2023 estimates, while TE has a multiple of 19. We think TE will earn $9 a share in fiscal 2024 and trade at 23 times earnings, giving the stock 30% upside, dividends included, over two years.

As for my last pick, there is no easier way to make money in the market than to buy a great company under pressure due to short-term concerns.

There are plenty these days.

Amazon.com has dramatically lagged other big tech stocks and the market in the past year. Its core retail business is facing difficult comparisons postpandemic. First-quarter revenue and profit expectations may be too high, and comps won’t get easier until the third quarter. Also, retail margins have disappointed. Amazon’s retail business is trading in line with Walmart [WMT] on an enterprise value to sales basis, based on 2023 numbers. If you were to separate out the high-multiple and high-growth advertising business, you could argue that you were paying negative value for the retail segment. The margin disappointment relates to the magnitude of square-footage additions in the past two years. When expansion slows, margins will expand again.

The market is so fixated on retail that it has missed the value of Amazon Web Services, or AWS, which is conservatively worth 12 times sales, or $1.15 trillion, based on 2023 estimates. We expect this business to grow revenue by $14 billion to $15 billion in 2021, a 30% increase. Given 10% to 15% of TAM [total addressable market] penetration by AWS and cloud-computing companies, there is a long runway for growth. We think Amazon’s stock could double in four years, assuming a multiple of 10 times sales for AWS and 35 times normalized earnings for the retail and advertising business, based on 2027 estimates.

Thank you, David. Abby, you’re up.

Cohen: The market’s gains, particularly until last year’s third quarter, were concentrated in specific sectors. Performance was also concentrated in the U.S., which dramatically outperformed other equity markets over the past several years. As we discussed earlier, inflation has become an issue, and interest rates are going to rise, which has an impact on stock and fixed-income selection, not just asset allocation. There is a presumption behind a lot of asset-allocation decisions, and products such as target-date funds, that returns will remain what they historically have been. I’m not picking on target-date funds. I am only suggesting that it is important to look at the valuation of assets at the time an investor buys in. I worry that there could be a reckoning in 2022 if interest rates rise; holders of fixed-income mutual funds might be surprised to learn that they could lose money in what they thought was a safe investment.

The equity market will see increased volatility this year. With the global economy growing, equities will notably outperform fixed income, although I don’t think equities will have a good year. P/E ratios will compress. We are beginning to see more careful attention paid to stock selection.

That’s a perfect segue to picks.

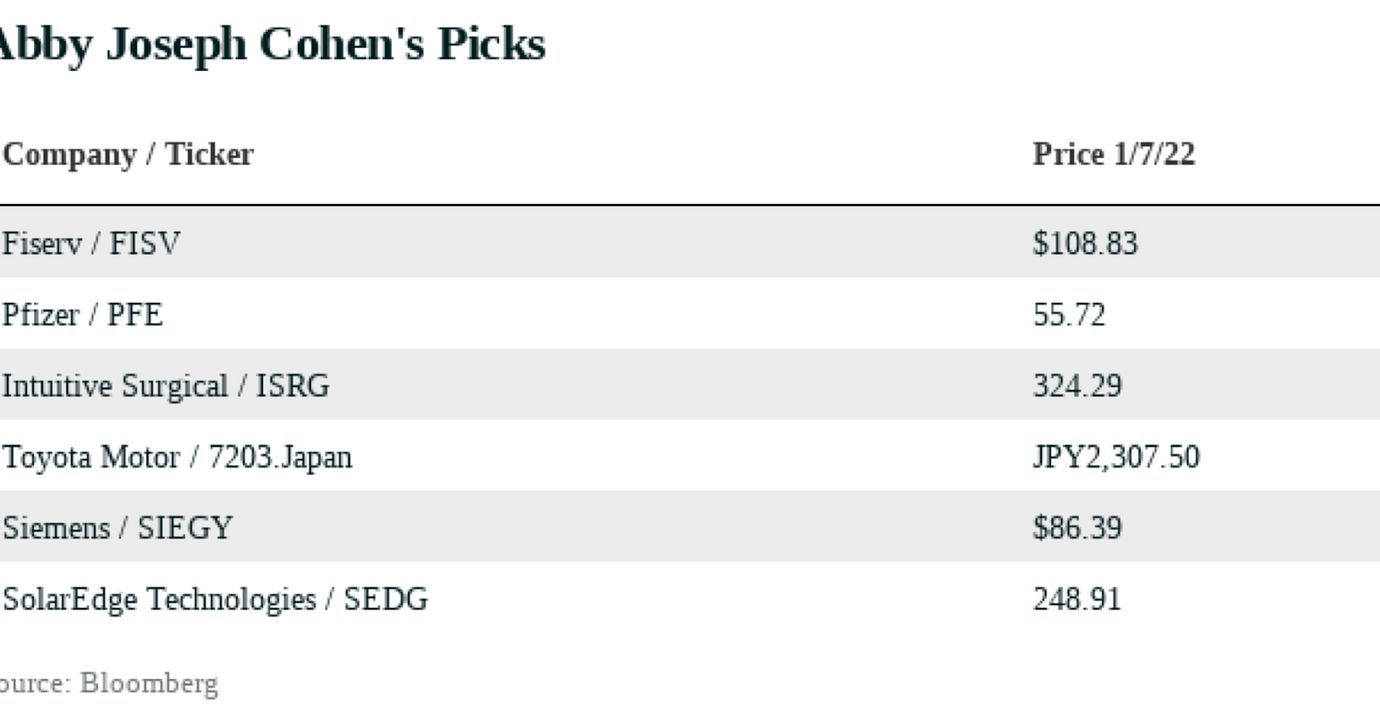

Cohen: I, too, am recommending Fiserv [FISV], as did Todd [in the first Roundtable issue]. When investors look for sectors that underperformed in the past year or two, and which might perform better in a rising-rate environment, financial services will be in that category. Fiserv is a well-established payments processor. Investors haven’t been enthusiastic about it because they have been focused on newer fintech companies. Also, Fiserv had made an acquisition, Clover, that wasn’t yet fully integrated

into their operations. The stock fell 11% last year, which makes the valuation more appealing. Earnings are likely to grow around 10%, with revenue growth a little lower. It’s a cash generator, and can buy back shares or make an acquisition. It trades for about 18 times earnings.

Pfizer [PFE] underperformed the pharmaceuticals sector for many years. Then the pandemic hit, and Pfizer and its partner BioNTech [BNTX] developed a successful Covid-19 vaccine, garnering much attention from investors. The shares rose 50% or so in the past 12 months, and are now trading around $56. While last year’s vaccine sales surge might not be repeated in 2022, a regime change in drug development has occurred at Pfizer that will bring continued benefits. For example, the company reported in December that its initial data on Paxlovid showed it is 90% effective in reducing Covid-related hospitalizations among those with the virus. The drug may be a game changer in turning Covid from pandemic to endemic, and Pfizer announced a large increase in 2022 production.

Pfizer also announced agreements with two smaller biotech companies, BioNTech and Beam Therapeutics [BEAM], to continue development of messenger RNA vaccines and other approaches to treating disease. Pfizer has the distribution and manufacturing capability, and mRNA technology has many uses. Additionally, the company expects to have an Omicron-specific vaccine available, likely in March. It may not be needed. But the fact that Pfizer has developed and produced this in short order, and will have it ready for distribution, tells you something about the way the company conducts itself. Pfizer has also been a leader in providing vaccine doses for use outside the U.S. and other developed economies. The big global health challenge in 2022 will be distributing vaccines in poor countries.

Based on consensus estimates, Pfizer is trading for about eight times this year’s expected earnings. It has a dividend yield approaching 3%. Cash flow can support a 3% yield and a planned 25% to 30% increase in research-and-development spending this year.

What else intrigues you?

Cohen: Intuitive Surgical’s [ISRG] stock made a low of $227 in the past 12 months, and a high of $370. It was recently $326. Intuitive is well-known for the da Vinci system used in robotic surgeries. Many procedures were delayed during the pandemic due to overworked hospital staff and facilities, and the business hasn’t fully recovered to pre-Covid levels. The stock’s performance could improve this year as surgeries increase; there is a backlog in demand. In addition, the company is introducing a new multiport robot that is even more capable than prior machines. It also has some new diagnostics systems. Intuitive has strong cash flow and no long-term debt. The stock isn’t cheap: It is trading for about 50 times this year’s expected earnings. Return on equity is around 17%. Postpandemic, the company can do well.

My next two picks are repeats from the 2021 Midyear Roundtable. The stocks did well late last year, as investors began to look for non-U.S. growth opportunities. I expect that to continue. Like many traditional car companies, Toyota Motor [7203.Japan] didn’t get a lot of respect from investors in recent years, given the enthusiasm for Tesla and some other EV-focused entities. Last year, auto makers dealt with supply-chain problems and a shortage of semiconductor chips. This year will be a catch-up year for global auto production.

Although stocks like Tesla may continue to benefit from optimism around EV adoption, I expect there will be increasing attention on established auto makers with the capital structure, longevity, manufacturing expertise, and brand loyalty to have success in this area. Toyota produced about 10 million vehicles last year, and sold 2.3 million in the U.S. Tesla had a great year; it sold around 900,000 cars globally. It will take time for EV adoption to become widespread. Toyota is developing EVs, and is No. 1 in hybrid vehicles using gasoline and battery power. This is important because charging stations aren’t widespread. The stock sells for about 10.5 times earnings for the fiscal year ending in March 2023 and has a projected yield of 3%. Return on equity is about 12%.

What else do you still like?

Cohen: Siemens [SIEGY] is the largest industrial manufacturing company in Europe. It focuses on electrical engineering products for the energy and healthcare markets, among others. Medical equipment and infrastructure accounts for 40% to 50% of sales. Siemens is also a leader in making electrical systems for so-called sustainable buildings. Its products are used in smart infrastructure. It is involved in cleaner transport and is a major producer of rolling stock—equipment for commuter rails and freight systems.

Industrial companies should do well in an environment of economic growth and moderate rises in inflation and interest rates, and the company scores well based on ESG metrics. Also, for the first time in recent memory, growth is better in Europe than the U.S.

The European Central Bank won’t be as anxious as the Fed to start raising interest rates this year

I expect U.S. GDP to grow by about 3% this year. Growth in Europe might be somewhat faster than that. Fiscal policy is still supportive in Europe, and Germany’s new government has indicated it wants to support capital spending, including in “green” categories in which Siemens operates. Also, the European Central Bank won’t be as anxious as the Fed to start raising interest rates this year. Siemens trades for 18 times consensus estimated earnings for the fiscal year ending next September, and 16 times fiscal 2023 estimates. It yields 3.4%.

My last pick, SolarEdge Technologies [SEDG], builds photovoltaic systems and solar inverters. It is known mainly for residential work. It is getting more attention now for its energy-storage backup systems, the value of which has become more obvious in recent climate disasters. It is also developing battery chargers for electric vehicles, and larger-scale inverters that can be used by utility companies. SolarEdge stock was down almost 30% in the past 12 months, amid worries about competition and the company’s ability to make some of these new products. The stock is trading for 34 times consensus earnings estimates for 2022. Gross margins are about 32%; the cost of goods sold has been rising, but not as rapidly as revenue. SolarEdge continues to spend heavily on R&D.

Thank you, Abby.