Mjukvaruaktier i fritt fall – därför kan marknaden ha fel

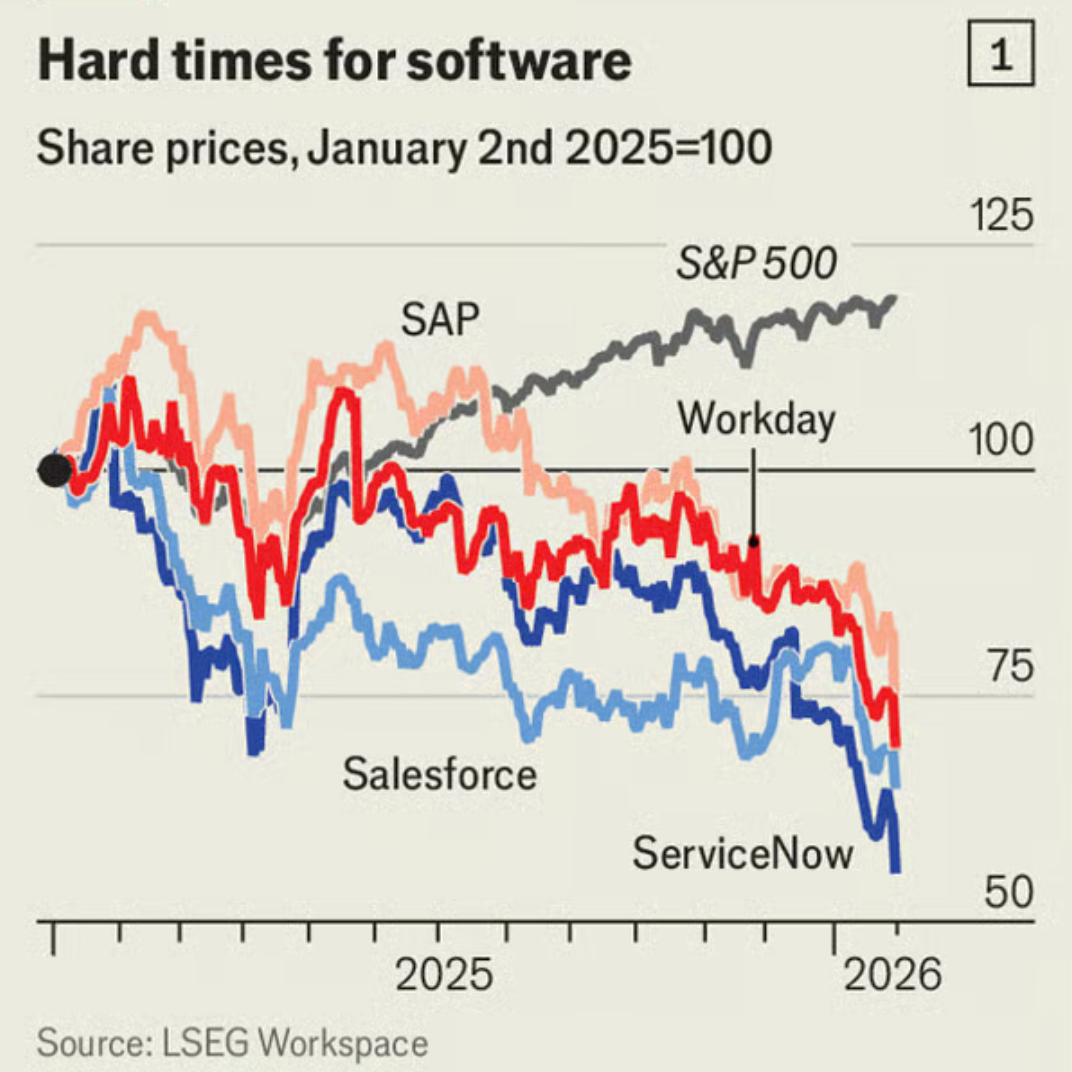

Mjukvaruaktier, som SAP och Salesforce, har fallit på börsen efter signaler om lägre tillväxt i år. Raset har drivits av oro för att AI ska göra etablerade affärssystem överflödiga. Men rädslan är överdriven, skriver The Economist.

Den viktigaste förklaringen till avmattningen är i stället ett svagare konjunkturläge efter pandemin, med högre räntor och minskade it-investeringar.

På sikt kan AI snarare gynna stora mjukvarubolag genom lägre utvecklingskostnader och ökad efterfrågan, menar tidningen.

Why software stocks are getting pummelled

Are investors overestimating the risk from AI?

It was a bloodbath. On January 29th SAP, whose applications are widely used to manage everything from inventory to payroll, said during an earnings call that it expected a “slight deceleration” in its cloud-based software business in 2026. Its share price plummeted by 15%. That of ServiceNow, whose tools help businesses automate various tasks, dropped by 13%, even though in the latest quarter its revenue grew faster than analysts had expected. Even software companies that released no news suffered, with Salesforce down by 7% and Workday by 8% (see chart 1).

The carnage reflects growing nervousness over the future of the software industry in the age of artificial intelligence. The value of listed American enterprise-software companies is down by 10% over the past year. After a period of blistering revenue growth, their momentum has slowed sharply. Yet investors risk misdiagnosing the industry’s troubles.

The main reason behind the revenue slowdown is the economy. During the pandemic, business spending on software soared. Low interest rates allowed companies to borrow heavily to fund investments in new systems. With workers and consumers stuck at home, many bosses felt they had to improve their digital offerings. After the pandemic, higher rates and a surge in uncertainty trimmed such spending. Official data from America suggest that annual growth in business-software investment fell from 12% in 2021-22 to 8% in 2024.

But could an AI upheaval be just around the corner? Pundits have focused on two threats. The first is from AI coding tools. Anthropic’s Claude Code and OpenAI’s Codex, among others, help programmers to write code far more quickly. “Vibe coding” startups, such as Lovable and Base44, allow even laymen to make software by giving chatbots simple instructions. The fear is that these tools are allowing companies to create much of the software they need themselves. The other threat is that AI-native enterprise-software startups—such as Attio, which sells customer-management tools, or Glean, which offers a product that allows companies to perform advanced searches on their internal data—will steal business from the incumbents.

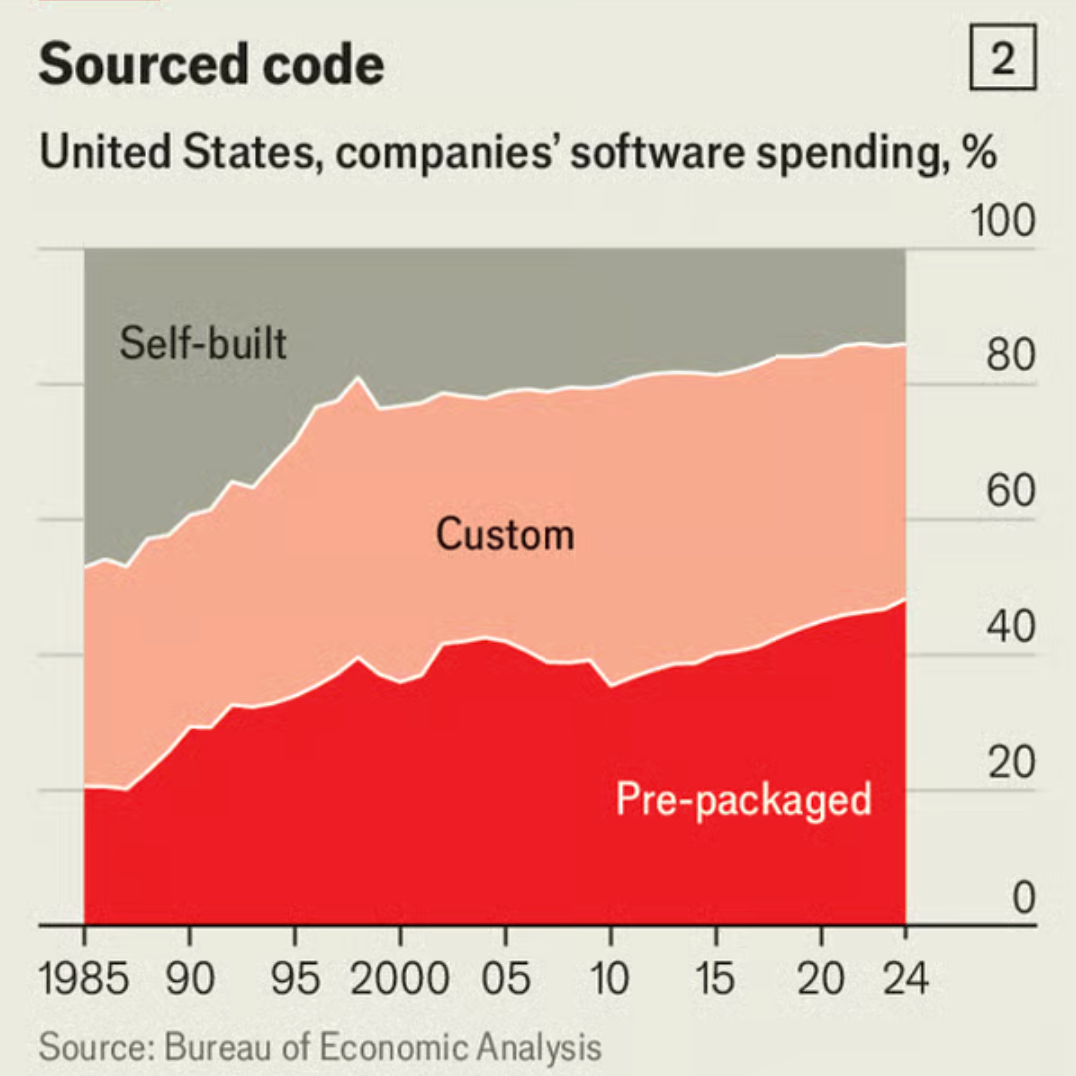

Consider these risks in turn. For most companies, building software is a distraction from their core business. The trend for decades has been in the opposite direction. In the mid-1990s American firms kept about 30% of their software investment in-house; the figure today is half that (see chart 2). The typical large company now has subscriptions to hundreds of programs. Even OpenAI uses Slack, a messaging service owned by Salesforce.

There is little reason to think AI will reverse the trend. Partly that is because the technology still has its limitations. AI-generated code is often less elegant, less parsimonious and thus less effective. Call it “slopware”. Andrej Karpathy, a former head of AI at Tesla, recently lamented that the models make “subtle conceptual errors that a slightly sloppy, hasty junior [developer] might do”. The boss of a big consultancy adds that the technology tends to be more useful when writing brand new software, and less so when working with a company’s existing systems.

Of course, AI will continue to improve. But it is also likely to get more expensive. At present Silicon Valley heavily subsidises its price. That cannot last for ever. OpenAI expects to burn $17bn in cash this year. Microsoft’s share price took a beating last week as investors winced at its enormous spending on the data centres underpinning the technology. Eventually these companies will need to demonstrate a return on all that investment, which is bound to mean higher prices.

Software may eventually eat the world, but so far it has only nibbled around the edges at most companies

When that happens, dedicated software companies will have an advantage. That is partly for the simple reason that they can spread the cost of developing a program over their many customers. But it is also because they are better at using AI to write code. A recent paper by Fiona Chen and James Stratton of Harvard University examined the productivity of programmers using AI, and found that it resulted in an increase in output (measured by the number of tasks completed) only for those at companies selling software.

What of the software industry’s AI-native rivals? Here, too, the fear of disruption may be overblown. Incumbent software providers have been investing heavily to embed AI features in their products. To speed the effort, they have been on a dealmaking spree. Acquisitions last year included Workday’s purchase of Sana Labs, a Swedish AI startup, and ServiceNow’s purchase of MoveWorks, another AI company. The software giants have deep pockets to fund more investments: together Salesforce, SAP, ServiceNow and Workday generated almost $30bn in free cashflow last year. Their products are also sticky, because it is expensive and risky for large companies to switch software, and the companies can use their scale to quickly gather feedback on new AI features.

Indeed, AI may well turn out to be a blessing for incumbent software companies—at least big ones with cash to invest in it. Even if the price of accessing AI goes up, the technology should still bring down the cost of developing software over time. That could lead to more, not less, spending on software, as companies use it to replace tasks still done by humans.

Whether that happens depends on software’s price elasticity. Evidence on this is limited but suggestive. A paper published by the Bank of France finds that such spending is reasonably elastic. In our analysis of official data on American business-software investment, we similarly find that a 10% decline in software prices is associated with a 20% rise in spending. Software may eventually eat the world, but so far it has only nibbled around the edges at most companies. It could soon take a much bigger bite.

© 2026 The Economist Newspaper Limited. All rights reserved.