”Nvidias AI-dominans är ett tveeggat svärd”

Nvidia bryter återigen mot de ekonomiska naturlagarna, med tillväxtsiffror som får andra storbolags intäkter att blekna. Men den extrema framgången blottar också en lika stor sårbarhet, skriver Financial Times John Foley i en kommentar.

Chipjättens vd Jensen Huang menar att vår förståelse för AI:s potential bara är i sin linda.

Men om efterfrågan på datacenter viker, konkurrensen ökar eller investeringarna dämpas – då har Nvidia inget annat att luta sig mot, enligt Foley.

Nvidia’s AI supremacy is a weapon that cuts both ways

While the chipmaker is the big winner from the booming technology, it is singularly exposed to changing expectations.

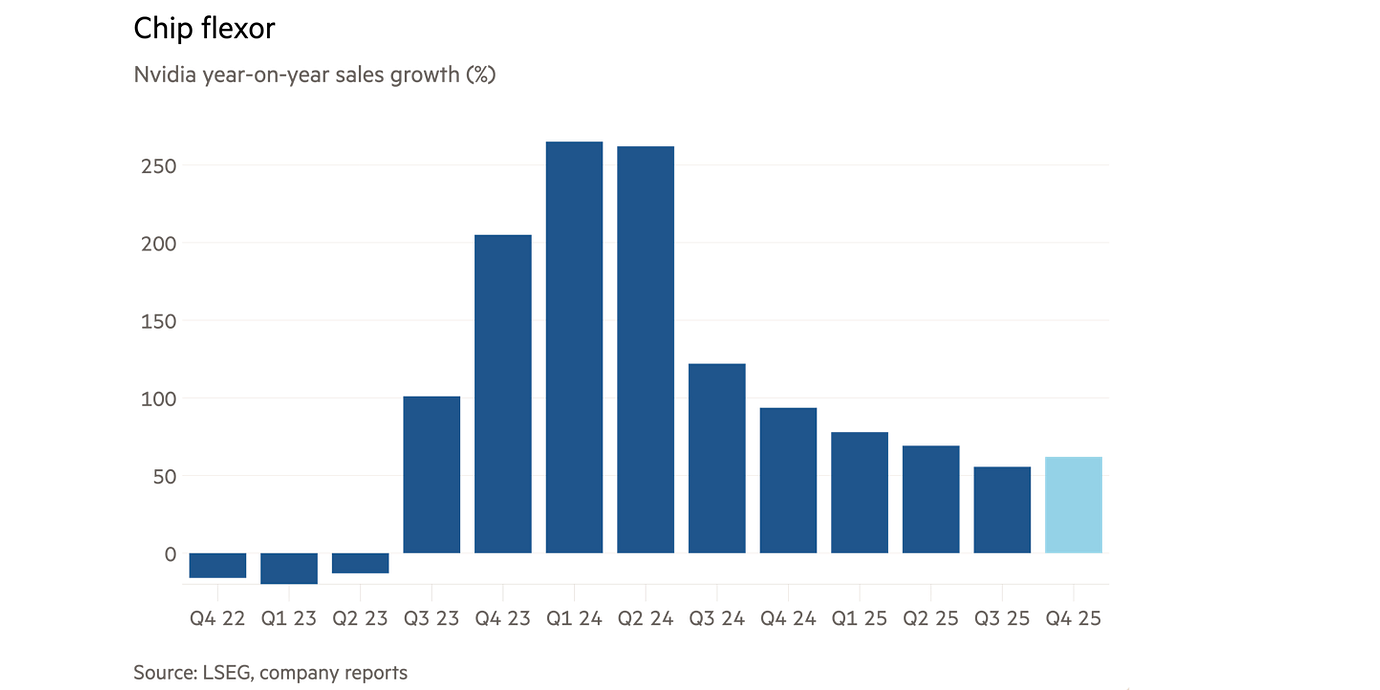

It’s hard to overstate how unlikely it is that a business with almost $200bn of annual revenue would grow at a rate of over 60 per cent. Yet such are the fantastical finances of Nvidia. The chipmaker that dominates artificial intelligence continued to break all the rules that apply to large companies with its quarterly earnings on Wednesday. Investors who try to predict how long this can persist do so at their peril.

In fairness, Nvidia’s freakish performance isn’t itself proof of a bubble

Nvidia is selling every piece of silicon it can make today, and piling up orders for those it plans to make tomorrow. Every indicator worth watching is therefore going up. The company breezed through analysts’ estimates of sales and profit in its latest quarter. Founder Jensen Huang had previously predicted $500bn of sales from Nvidia’s newer ranges of chips over 2025 and 2026; his finance chief now expects to beat that.

The numbers go from wild to ridiculous. The $73bn growth in Nvidia’s revenue over the past four quarters — just the growth, mind — is greater than an entire year’s revenue at Morgan Stanley or IBM. When Google’s top line was last increasing at the pace Nvidia’s is now, the search engine operator had a $150bn market capitalisation, whereas Nvidia’s is $4.5tn. Such momentum at such scale is unprecedented.

To some, this might seem like proof of a bubble. Huang acknowledged as much in a call with analysts on Wednesday. He doesn’t agree, naturally. Like many AI boosters, he argues that understanding of what AI can achieve is only in its infancy. As users experience the miracles of “agentic” and “physical” AI — the latter including robots and driverless cars — revenue will surely justify the trillions of dollars being invested now.

In fairness, Nvidia’s freakish performance isn’t itself proof of a bubble. Rather, it’s evidence that being a virtual monopoly pays. The company has a 90 per cent hold over the market for AI chips, and a 73 per cent gross profit margin, indicative of unearthly pricing power. Moreover, this is the kind of monopoly no antitrust regulator would ever want to hobble, because the entire developed world is now dependent on Nvidia’s chips.

Yet the very real demand for what Huang is selling does in no way prove that there isn’t a bubble. After all, Nvidia’s value really depends on what happens years from now, when supply and demand could look very different. How many data centres will still be being built 10 years hence? With whose chips? At what kind of profit margin? Estimates vary widely.

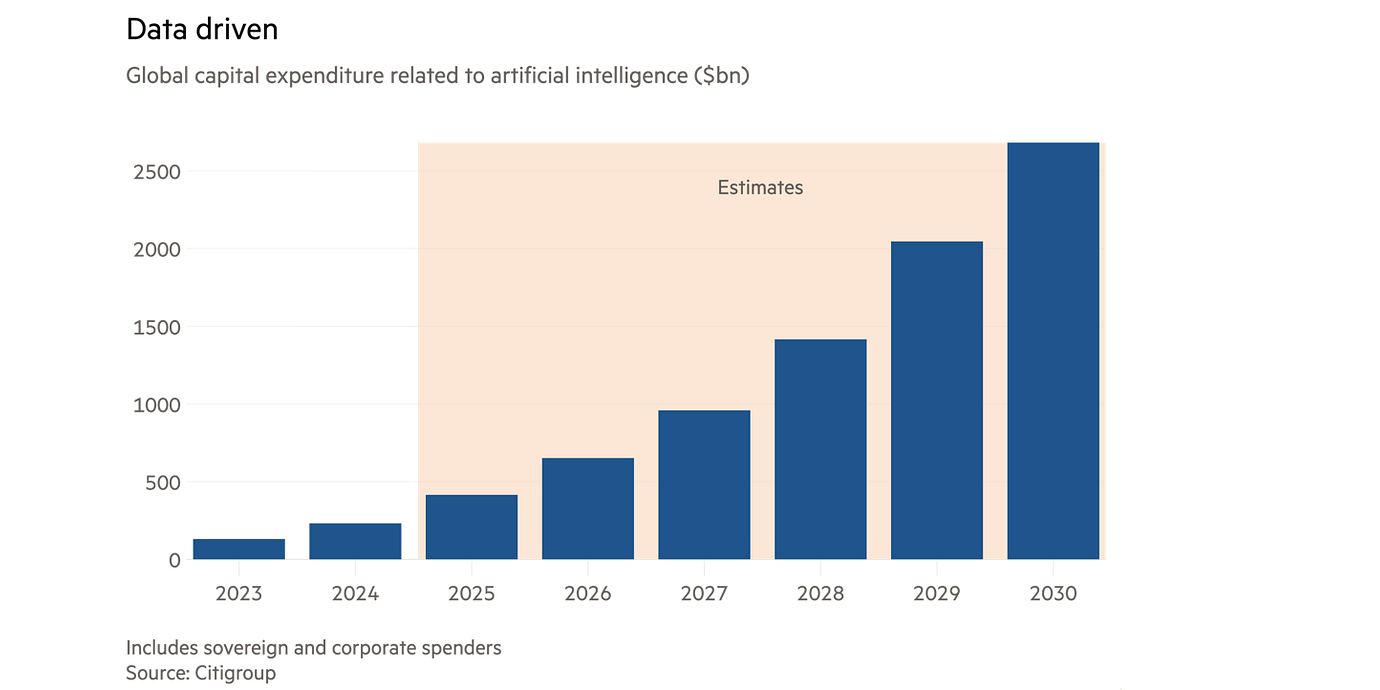

As an illustration, assume Nvidia gets about two-thirds of what it costs to build a data centre, as Huang claims, and protects its 90 per cent market share. Based on Citigroup’s generous estimate of $7.8tn of AI investment between now and 2030, that’s $4.6tn of total revenue. But use McKinsey’s less bullish estimate of $5.2tn of investment, and say Nvidia’s market share slips to 70 per cent, the lump of future revenue almost halves, to $2.4tn.

One thing that is certain: while Nvidia is the AI boom’s big winner, it is singularly exposed to changing expectations. That makes it different from, say, Microsoft or Google, or any other company operating in a more competitive part of the market. They can still be relative winners so long as they can win share from weaker rivals. Nvidia’s supremacy in chips means that if a correction does come, Huang has nowhere to hide.

©The Financial Times Limited 2025. All Rights Reserved. FT and Financial Times are trademarks of the Financial Times Ltd. Not to be redistributed, copied or modified in any way.