Revansch för ”Afrikas Amazon” – men Temu och Shein oroar

E-handelsbolaget Jumia har gått från börshajp till krisfall – men nu hoppas vd Francis Dufay på revansch. Efter år av förluster har det nigerianska bolaget skurit bort allt från matleveranser till närvaro i flera länder och kraftigt sänkt sina kostnader.

– Något fundamentalt behövde förändras i strategin, säger Dufay till Financial Times.

Aktien har stigit 120 procent i år – men bolagets kassareserv räcker bara till två års förväntade förluster. Dessutom pressas Jumia av kinesiska lågprisutmanare som Temu och Shein.

Is there a future for the ‘Amazon of Africa’?

Six years after a high-profile listing, Jumia is still trying to prove that it can be a profitable business rather than a relic of the cheap money era.

Hailed a decade ago as “the Amazon of Africa”, ecommerce group Jumia still tries to exude the air of breezy tech optimism that marked its early years.

“100% Africa, 100% internet,” the company’s website boasts.

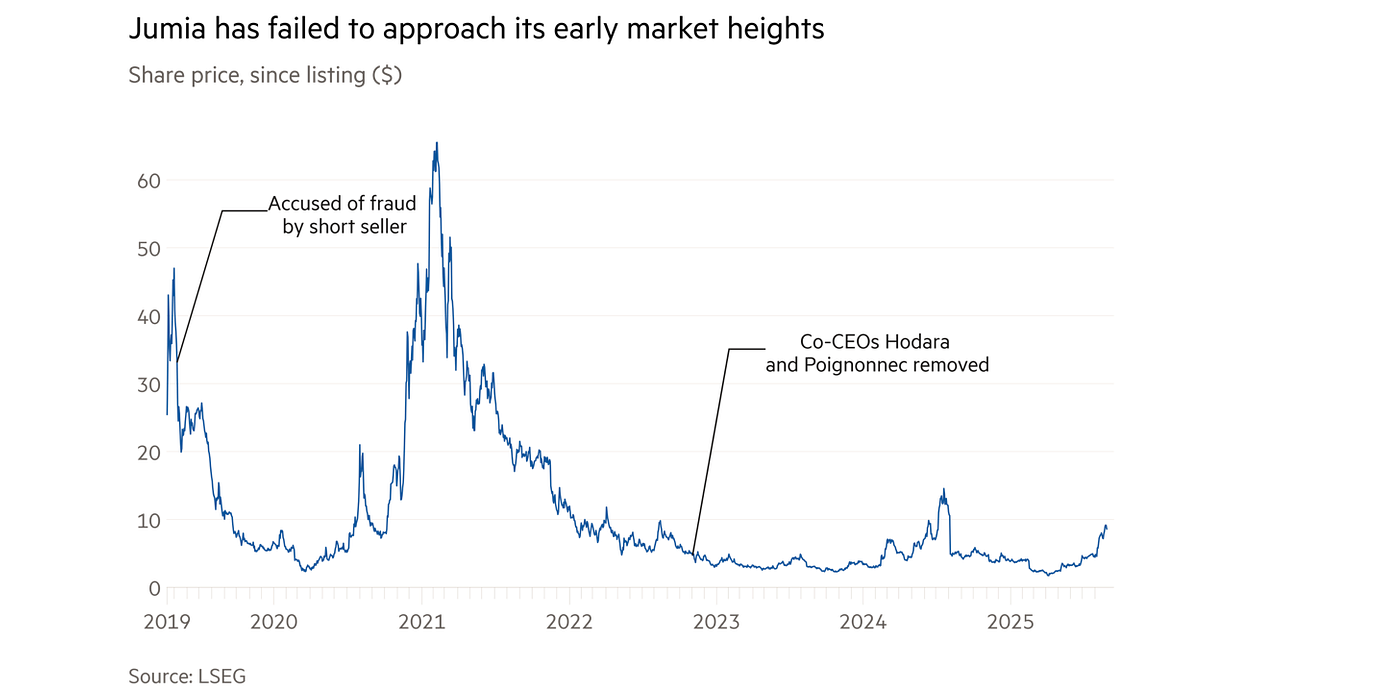

Yet since its much-heralded 2019 listing on the New York Stock Exchange — when it was the largest African IPO outside the energy sector — Jumia has lurched from one crisis to another as it has struggled with the glare of the public markets.

By November 2022, Jumia was losing money hand over fist and its share price had fallen about 70 per cent since its listing as concerns mounted over whether it would ever make a profit. Francis Dufay, a former McKinsey consultant originally from France, was promoted to take over running the company and given an explicit goal of “setting the business on a clear path to profitability”.

Since taking the helm, Dufay, who has been with the group since 2014, has helped to stabilise the situation. Losses have narrowed — Jumia recorded an operating loss of $16.5mn in its most recent results, down 18 per cent year on year. The company now hopes to achieve profitability by 2027.

“You cannot serve cash conscious customers who are probably the poorest middle class on earth . . . and have a level of general and administrative expenditure of a luxury goods company,” Dufay says about the post-IPO model. He adds: “Something fundamental had to change in the strategy.”

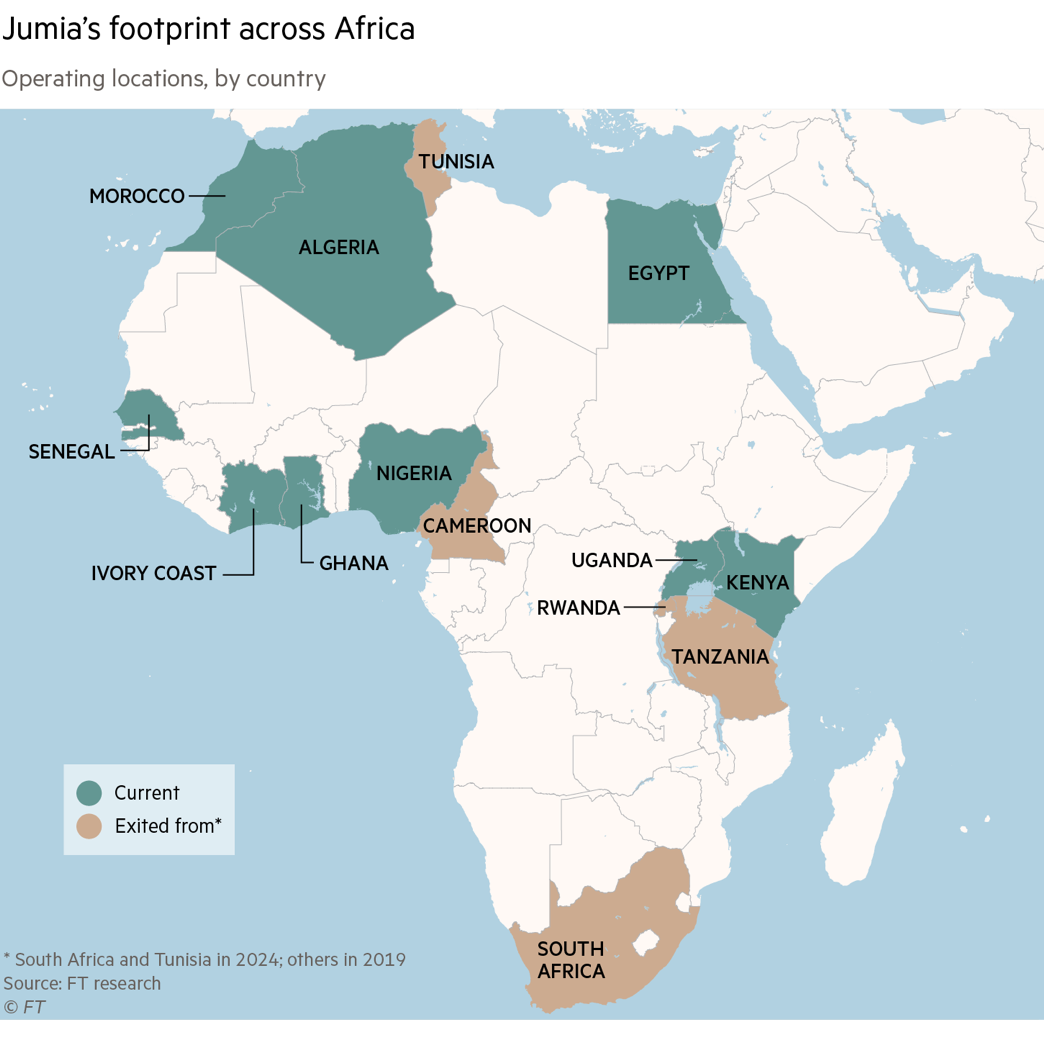

Jumia has slimmed down its footprint from 14 countries when it went public to nine. It has closed its food and grocery delivery business and closed its logistics business in all but two countries. Marketing spend is now a quarter of what it was.

Yet while the new Jumia may be a much leaner operation, it is not yet clear if it can become a robust, profitable business under its new model. The company’s cash level is equivalent to only two years of the expected loss for 2025, underlining the need for it to quickly stem losses.

Although Jumia says that it does not need to raise capital before it reaches profitability, this has led to speculation about possible takeovers or a deal to take the company private. Axian Telecom, the pan-African group, now owns nearly 10 per cent of shares in Jumia and has raised $600mn in debt in June for regional expansion.

For all the signs of progress, which have seen its shares rise 120 per cent this year, the core question remains. Is Jumia a company that tried to do too much too fast but which is now on the right track? Or is it a relic of an era of cheap money and tech utopianism when investors believed that you could simply transplant a model from developed countries on to one of the world’s poorest regions?

“For now, the trajectory is positive, but the journey is far from over”

“When you’re bleeding profusely, the first thing to do is to stop the bleeding — not mop up the floor,” says Emeka Ajene, a tech entrepreneur and founder of Afridigest, a media and strategic intelligence firm. Jumia’s board “finally stopped the bleeding” with the departure of Jeremy Hodara and Sacha Poignonnec, who ran the company before Dufay.

Ajene says the company has a 70 per cent chance of hitting its 2027 profitability target. “That’s a dramatic improvement from the near-zero probability I would have assigned to the old Jumia under previous leadership just a few years ago,” he adds. “For now, the trajectory is positive, but the journey is far from over.”

Even Dufay acknowledges the difficult reality that has confronted Jumia’s optimistic initial plans.

“This is what happens to a lot of western companies coming to Africa,” he says. “You dream of a certain type of market and sell beautiful things. But the truth is that the market is what it is and you have to adapt to that market.”

Jumia was founded in Nigeria in 2012 promising to revolutionise how more than 1bn Africans shop.

Rising internet connectivity and the widespread use of mobile phones fed into the theory that Africans were on track to join the rest of the world in the ecommerce boom.

Investors loved the straightforward “X for Y” pitch, says Eghosa Omoigui, a veteran investor in African start-ups through EchoVC Partners, a technology venture capital firm that he founded. The idea of an “Amazon for Africa” was hard to resist and investors wanted to get in on the ground floor at a time when enterprises promising versions of US start-ups were flourishing in other developing markets, Omoigui adds.

In a post-2008 era of low interest rates, western investors were on the hunt for frontier markets where they hoped to earn outsized returns.

Jumia was a beneficiary of this freewheeling era. It was initially backed by Rocket Internet, the German investment company that has been an early supporter of “clone” start-ups. Jumia was lavishly funded in the seven years before it went public, raising more than $800mn from Rocket and other blue-chip investors including Goldman Sachs, French groups Orange and Pernod Ricard, and South African telecoms company MTN. This amount of financing is still unprecedented for an African start-up.

With its huge financial backing, Jumia sought to attract talent from elite institutions. As well as Dufay, former chief executives and co-founders Hodara and Poignonnec also came from McKinsey.

“We were building an ecommerce and logistics business all at once. It’s a challenge that maybe people did not realise beforehand”

Kwehnui Tawah was a trader at Goldman when he swapped New York for Nairobi in early 2018, convinced he was joining a company poised to do something “transformative” for Africa. Tawah, who now runs his own ecommerce business in Kenya, recalls a company brimming with people with “high intellectual horsepower” and with a “good budget and big ambitions for what we wanted to do”.

The other prong of Jumia’s strategy was rapid expansion across the continent. From Nigeria, Jumia had reached an additional 13 countries by the time of its listing in 2019, with separate businesses in food and grocery delivery, travel booking and others as it tried to be all things to all people.

According to former Jumia insiders, this was largely driven by some of its outside investors, which prioritised scale at the companies it backed. In Jumia’s case, expanding across Africa was part of its bid to show it was “pan-African”.

“It was tough to keep a cool head in those times when money was for free and everyone was looking for the next Alibaba and there was a fear of missing out on the market,” says Dufay.

He adds that the decision to keep operating in South Africa and Tunisia, which Jumia eventually exited last year, had been “purely emotional” given the “time and attention” that had to be dedicated to them.

This scattergun approach meant that Jumia was competing in several businesses other than ecommerce, such as food delivery, which require large amounts of capital.

“Ecommerce requires focus to execute,” says one former senior executive. “And we did not have that because we grew very fast and couldn’t concentrate on everything.”

Jumia has faced a whole series of infrastructure problems in its ecommerce operation.

In many of the markets where it operates, such as Nigeria and Ivory Coast, some streets are still without formal addresses. In some cases, delivery drivers have to call recipients who describe how to find them, usually by using landmarks in the neighbourhood.

“We were building an ecommerce and logistics business all at once,” says the former executive. “It’s a challenge that maybe people did not realise beforehand.”

Omoigui, the veteran investor, says Jumia and its backers should have realised earlier that ecommerce on the continent was not as straightforward as importing a model from the west.

“If people had done the work and understood the local context, they would have known that Africa is not homogenous by any stretch,” says Omoigui.

Perhaps Jumia’s biggest problem has been that its most important bet has yet to pay off

Each market had its own peculiarities, he adds. In Nigeria, for instance, the company had to introduce a pay-on-delivery model, where customers would give cash or a card payment to the courier at the recipient’s doorstep, because the payment infrastructure was lacking in the early days. The result was that consumers could simply reject items they did not like.

In some countries, people created multiple accounts to take advantage of bonuses Jumia gave new customers, which meant the company was spending and losing a lot of money to attract and retain customers.

Geographic diversification did not bring as many advantages as was initially hoped. According to Tawah, the former Wall Street trader who worked for Jumia in Kenya, the company has benefited from being in multiple countries as a hedge against currency fluctuations but the number of countries they went to “did not make sense”.

“They were trying to do too many verticals at the same time using the same tech, HR, finance and investment for all of these things,” he says. “The young businesses got starved out. If you didn’t know the right person to talk to, your project died.”

Perhaps Jumia’s biggest problem has been that its most important bet has yet to pay off. In its filing to the US Securities and Exchange Commission, Jumia cited research showing that there were 399mn mobile internet users in Africa in 2017. With that number rising, so the theory went, more Africans would increasingly use online shopping.

Yet while more Africans are connected to the internet now than ever, ecommerce makes up only a small fraction of retail in Africa — even accounting for less traditional channels such as Facebook and Instagram, where many on the continent make purchases online. That is partly because people in the markets served by Jumia have simply not become “more affluent”, as the company had hoped.

Economic conditions have been tough in many of the countries in which it operates. In Nigeria, one of Jumia’s biggest markets, poverty levels have increased since Jumia’s 2019 listing, while Ghana has seen a default and Egypt was forced to sign a deal with the IMF in 2022.

The pandemic, which was a boon for ecommerce in Europe, North America and China, did little to improve Jumia’s fortunes. Unlike those regions, most African countries did not have extensive lockdowns that could have prompted a shift in consumer behaviour as the majority of people did not have jobs that allowed them to work from home.

Most of Jumia’s early backers have either exited their stake in the company entirely or pared down significantly. South Africa’s MTN sold off the entirety of its holdings in October 2020, months after Rocket, Jumia’s early backer, did the same. Baillie Gifford, once its largest institutional investor, sold off what was left of its position in May.

Jumia’s race to profitability is complicated by the entrance of Chinese low-cost giants Temu and Shein into Africa

After a rally in its share price, the market capitalisation finally crawled back above $1bn in August, although this is far off an early 2021 peak of over $5.8bn. Jumia remains a minnow compared to other companies that scaled up profitable ecommerce empires in tough emerging markets. Singapore’s Sea Ltd, owner of Shopee, south-east Asia’s largest ecommerce platform, has a market value close to $110bn: that of Mercado Libre, the Latin America-spanning online marketplace, is about $125bn.

Dufay says he is enthused by the fact that Axian, the pan-African telecoms group that operates in nine countries across the continent and has a fintech and consumer credit business, took a major in the company stake just as Baillie Gifford was jumping ship. Last week Hassanein Hiridjee, chief executive of Axian, joined the Jumia board.

The biggest source of optimism is the company’s modestly improving financial results. Its second-quarter earnings showed a 25 per cent increase in revenue to $45.6mn, and a 6 per cent growth year on year in gross merchandise value (total sales) to $180.2mn.

It has lowered its guidance for full-year pre-tax losses to between $45mn to $50mn, from the $50mn to $55mn losses it was forecasting earlier this year. That compares to losses of $206mn in 2022 and $97.6mn last year. The company has $98.3mn of cash, according to its most recent results.

“We are planning the business to not raise additional capital,” the company says. “We have sufficient cash to operate the business and turn profitable by 2027, which is what we project.”

Jumia’s race to profitability is complicated by the entrance of Chinese low-cost giants Temu and Shein into Africa, although Jumia executives are confident they can withstand the competition from their better-funded rivals.

Temu and Shein offer aggressive discounts to attract price-conscious customers and have steadily cut down their shipping times to improve delivery. Although Jumia delivers faster than its competitors, Temu in particular offers discounts as high as 50 per cent, which means customers are content to wait for an extra week at those prices.

“All the long-term trends of demographics, internet usage and improvement of infrastructure are in favour of ecommerce”

Ajene, of Afridigest, says he is encouraged by Jumia’s unit economics that allows it to serve its customers “sustainably”. But the question remains whether the company can “continue to execute with precision and reignite growth in customers and orders without commensurate spending” — all while competing against Temu and Shein.

Dufay says Jumia now acknowledges the booming affluent middle class hoped for in the past is unlikely to take shape in the coming years. Instead, the company has recalibrated its expectations and is now “proud” to serve Africa’s “real middle class”, which as he described it are people earning between $200 and $300 a month.

He says the new strategy, of focusing on what Jumia calls “entry-level and affordable” sales, will be a robust market over the next two decades.

“All the long-term trends of demographics, internet usage and improvement of infrastructure are in favour of ecommerce,” he insists. “But we also know it’s unlikely that people [will] get much richer tomorrow morning.”

Additional reporting by Joseph Cotterill in London

©The Financial Times Limited 2025. All Rights Reserved. FT and Financial Times are trademarks of the Financial Times Ltd. Not to be redistributed, copied or modified in any way.