Trump är inte den första ledare som velat tygla Fed

Flera amerikanska presidenter har genom historien försökt påverka Federal Reserve för att styra landets penningpolitik i sin egen politiska riktning – ibland med allvarliga konsekvenser.

Nu vill Donald Trump, republikanernas presidentkandidat, ta det ett steg längre genom att kräva ökad presidentkontroll över centralbanken.

Det förnyade trycket på Feds oberoende skapar osäkerhet inför framtiden och kan bli ett hett samtalsämne vid centralbankskonferensen i Jackson Hole, skriver Barron’s.

Donald Trump Isn’t the First President in History to Want to Rein in the Fed

When the world’s central bankers gather later this month for their annual symposium in Jackson Hole, Wyo., the topic of discussion will be “Reassessing the Effectiveness and Transmission of Monetary Policy.”

In light of recent developments, they might consider changing the theme to “Reassessing and Defending the Independence of Central Banking.”

Former President Donald Trump, now the Republican nominee, has called for more presidential control over monetary policy, threatening the autonomy that central bankers have fought for since the Fed’s 1913 founding.

Richard Nixon famously bullied Arthur Burns, but presidents including Warren Harding, Harry Truman, and Ronald Reagan all pressured the Fed to go their way.

With the prospect of more potential showdowns looming, it’s worth taking a look at how presidents and central bankers have wrestled over the years, and how it has affected monetary policy, for better or worse.

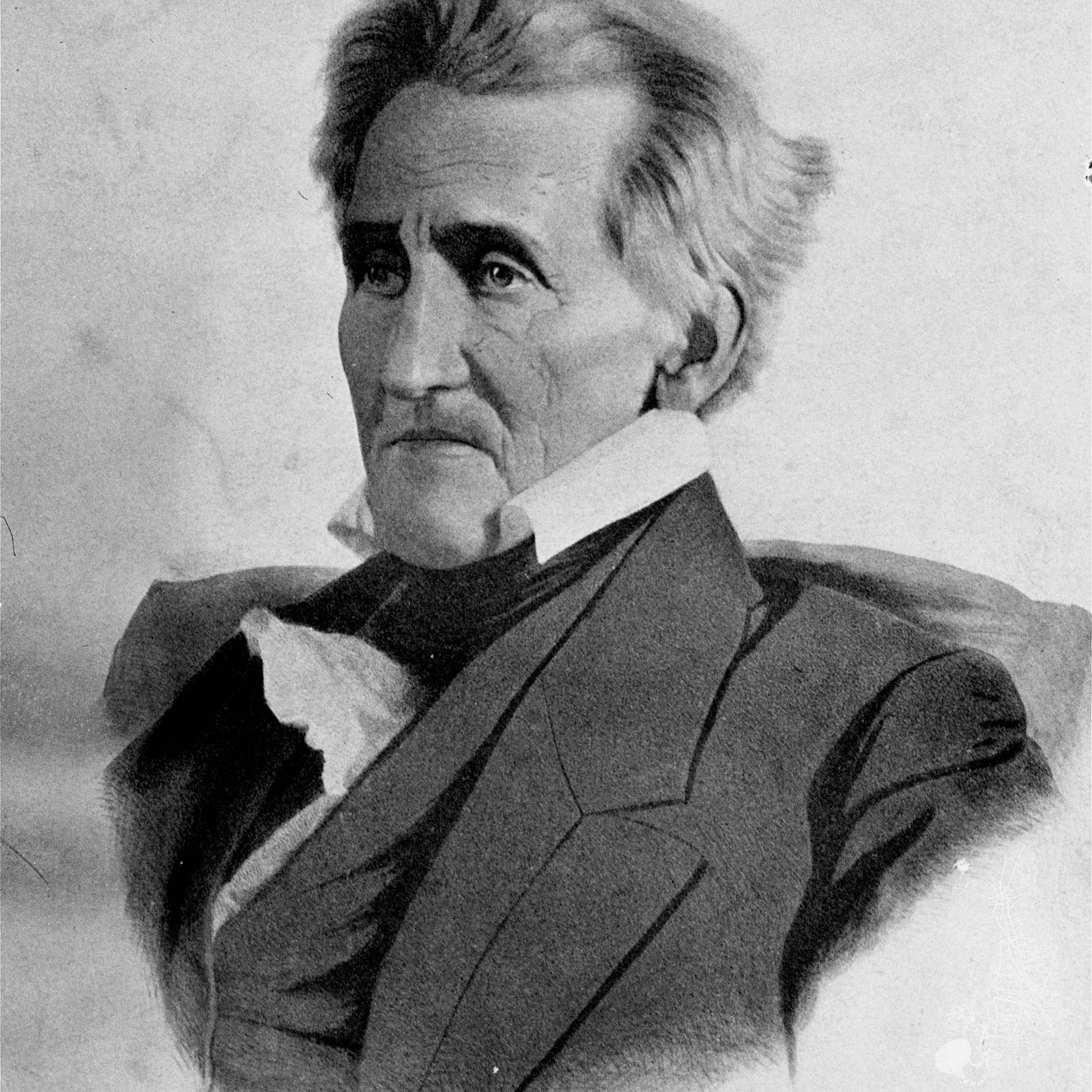

America had lived without a central bank since 1836. That’s when President Andrew Jackson quashed the previous one, calling it “unauthorized by the Constitution, subversive of the rights of the States, and dangerous to the liberties of the people.”

Such beliefs—still echoing today—held sway until a series of financial shocks culminated in the Panic of 1907, which required a federal bailout from financier John Pierpont Morgan. An embarrassed Congress went to work, and President Woodrow Wilson signed the Federal Reserve Act of 1913.

Independence wasn’t part of the deal. The Treasury secretary was an ex officio member and the de facto chairman of the Federal Reserve Board, putting it directly under the president’s thumb.

Taking office during the 1921 recession, Harding declared America a “business country,” and Treasury Secretary Andrew Mellon—the millionaire banker who would serve 11 years under three presidents—installed a low-interest-rate regime at the Fed.

The 1920s were soon roaring on easy money. Too late did the Fed realize that it had also unleashed reckless speculation. Rate increases in 1928 failed to slow speculators, but they did hobble business activity.

It all came together in the Crash of October 1929. Then the Fed stood by as banks across the country failed, even though stopping panics as lender of last resort was its reason for being.

“The Fed’s failure to preserve either monetary or financial stability made the Great Depression much worse than it might otherwise have been,” former Fed Chairman Ben Bernanke writes in 21st Century Monetary Policy.

The Banking Act of 1935 removed the Treasury secretary from the Federal Reserve Board, but it didn’t stop presidential hectoring.

Rates were kept low through World War II and its aftermath to finance war debt. But this stoked inflation, which reached 21% in February 1951. The Fed wanted to raise rates. Truman objected, and summoned the Federal Open Market Committee to a White House meeting.

Next day, Truman publicly thanked the FOMC “for their expression of full cooperation given to me yesterday,” implying that they’d agreed to keep rates low.

The day after that, the FOMC denied giving any assurances.

“The fat was in the fire,” wrote FOMC member and its former chairman, Marriner Eccles.

Truman blinked, and the Treasury-Fed Accord of 1951 gave the central bank “the freedom to set policy to advance broad economic goals rather than serving the Treasury’s financing needs,” writes Bernanke.

A couple of decades later, this accord offered Arthur Burns little cover as President Richard Nixon’s Fed chief.

Nixon had other ideas. He wanted easy money to boost the economy for his 1972 re-election campaign.

With prices soaring and Americans worried, Burns assured Congress in February 1970 that he’d keep credit tight, lest “we lose the battle against inflation.”

Fed freedom isn’t constitutionally guaranteed. It’s more a matter of convention

Under Nixon’s haranguing—“as he spoke,” Burns wrote of one encounter, “his features became twisted and what I saw was uncontrolled cruelty”—the Fed chairman fell in line. By January 1972, he had lowered the discount rate to 4.5% from the 6% he inherited.

Nixon got his economic boom and won re-election. But the U.S. got another decade of double-digit inflation.

In 1979, Paul Volcker became Fed chairman with a mission to slow inflation, whatever the cost. He tightened the money supply until the Fed-funds rate approached 20%, while the unemployment rate surpassed 10%.

In the summer of 1984, Reagan—seeking re-election—invited Volcker to the White House. Chief of Staff James Baker joined them.

“[Reagan] didn’t say a word,” Volcker wrote. “Instead, Baker delivered a message: ‘The president is ordering you not to raise interest rates before the election.’”

Volcker’s moment of truth had come. He could cave, as Burns had to Nixon. Or he could stand up for Fed independence, as Eccles’ FOMC had with Truman.

“I walked out without saying a word,” Volcker wrote.

The Fed has maintained its independence ever since. Now, Trump is pushing for “at least [a] say” in Fed policy, perhaps as an ex officio FOMC member. The Heritage Foundation’s Project 2025 policy paper calls for ending the Fed’s role as lender of last resort, even abolishing it entirely.

To be sure, Vice President Kamala Harris, the Democratic presidential nominee, said she wouldn’t interfere in Fed decisions. And, outside conservative circles, there seems little political support for challenging the central bank’s autonomy.

Still, Fed freedom isn’t constitutionally guaranteed. It’s more a matter of convention, depending on a president who respects the central bank’s independence and a chairman willing to stand up for it.

What happens if Trump, or another president, gives a Fed chairman a direct order? That’s likely to be a theme of discussion on the sidelines at Jackson Hole.