Tuffaste utmaningen sedan starten – men Amazons aktie kan mer än fördubblas

Amazon genomgår sin största prövning sedan grundaren Jeff Bezos började sälja böcker från sitt hus för 30 år sedan. För första gången finns det en risk att omsättningen minskar, skriver Barron’s.

Men trots svåra tider för affärerna är det ett misstag att döma ut Amazon. Med ett konkurrenskraftigt mediebolag, annonsintäkter på 40 miljarder dollar om året och en växande molntjänst är utsikterna goda.

Bolaget är visserligen svårvärderat på grund av sin spretiga verksamhet men aktien har potential att dubblas i värde, kanske till och med tredubblas, skriver tidningen.

Amazon Stock Has Gotten Crushed. There’s a Case It Could Double, or Even Triple, From Here.

For investors, it’s time to refocus—Amazon shares have never looked more attractive.

By Eric J. Savitz

Barron's, 22 July 2022

Amazon.com has reported earnings about 100 times since it went public in 1997. Every one of those quarterly reports has shown a growing company, despite plenty of ups and downs in the economy—and the internet. Amazon’s worst quarter came in September 2001, when the internet bubble was blowing apart. Even then, revenue grew slightly from a year earlier. Now, though, Amazon’s streak may be coming to an end.

When Amazon (ticker: AMZN) reports second-quarter earnings on July 28, Wall Street analysts expect revenue growth of just 5%. That’s a tepid number by Amazon standards, and if things are just slightly worse than expected, revenue could actually decline. It would be a telling moment, with Amazon facing its greatest set of challenges since founder Jeff Bezos began selling books out of his house almost 30 years ago.

The company’s longtime advantage in e-commerce has arguably become a weakness, with physical stores enjoying a post-Covid renaissance. Elevated fuel costs, meanwhile, are crimping Amazon’s profits, with the cost of deliveries and returns on the rise.

Amazon’s profit margins have never been rich, but analysts forecast a razor-thin 1.8% operating margin in the second quarter. After years of giving Amazon a pass on profits, investors have grown impatient. Since peaking last July, the stock is down 33% to a recent $125, shedding more than $600 billion in market value. Seen through the e-commerce lens, Amazon is one more struggling tech company.

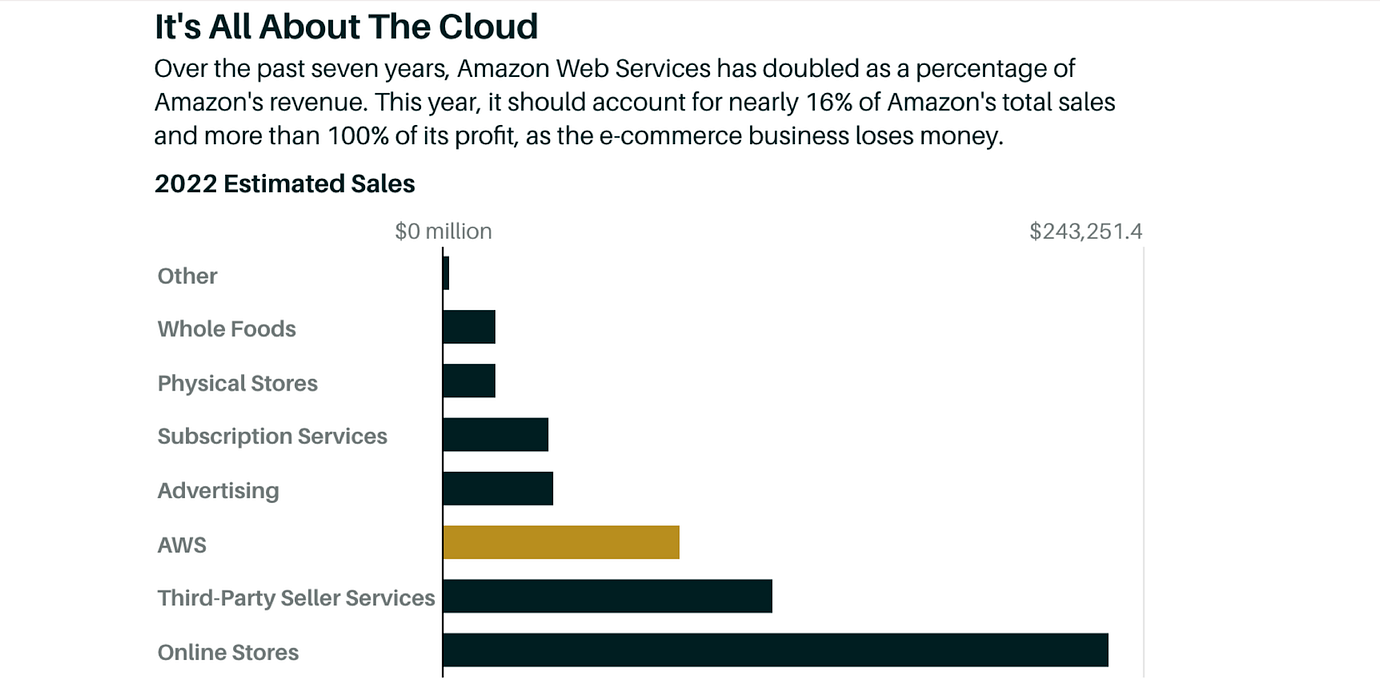

And yet none of that should matter. Investors’ preoccupation with Amazon’s retail operations overlooks the company’s transformation. This year, the Amazon Web Services cloud business will be about 15% of the company’s total revenue but more than 100% of its profits. Before, during, and after pandemic lockdowns, AWS revenue grew at a 30%-plus quarterly clip. In the long term, those trends should continue.

Meanwhile, Amazon has an advertising business that has annualized revenue of close to $40 billion. That’s nearly four times the size of Twitter (TWTR) and Snap (SNAP) combined. And it’s a media company that now controls the rights to a weekly National Football League game, a package that was once exclusive to broadcast giants Comcast (CMCSA), Fox (FOXA), Paramount Global (PARA), and Walt Disney (DIS) . There’s also a growing logistics operation that increasingly rivals FedEx (FDX) and United Parcel Service (UPS).

The challenge for investors is that the sprawling operation has made Amazon difficult to value. It’s worth the effort—Amazon shares have rarely been more attractive. The stock could double, or triple, over the next few years. Yes, the latest quarter will be bad. But the future couldn’t be brighter.

Gene Munster, a portfolio manager at Loup Ventures, says his firm has been adding to its Amazon position. While Munster concedes that investors are concerned about e-commerce profitability in the short run, he’s convinced that in the long run, “no one is going to compete with Amazon” in online shopping. Munster figures that AWS and the ad business together will generate $45 billion in operating income this year. Value that at 25 times earnings, says Munster, and you get $1.1 trillion, which is just about the company’s current total market value. That means investors are currently getting everything else free: online stores, Prime, logistics, Whole Foods Market, and a host of other businesses that Amazon has acquired over the years.

“It’s hard not to like Amazon at this valuation”

To be sure, Amazon continues to face bad publicity. The company is pushing back against unions trying to organize Amazon workers, a difficult balance for a company that claims to be Earth’s best employer. The company is also dealing with a newly empowered Federal Trade Commission led by Chair Lina Khan, who once wrote in the Yale Law Review that Amazon’s dominant market position was clear evidence that U.S. antitrust laws weren’t effectively regulating the U.S. internet sector. Amazon is sure to face intense government scrutiny for future acquisitions. And it could be forced to make concessions to the government.

For now, though, Amazon is still finding ways to grow through deals. Just this past week, the company agreed to buy One Medical, an owner of membership-based healthcare clinics, for $3.9 billion.

There’s also a chance the slowing economy could weigh on AWS sales for the next few quarters. For this year, Wall Street currently expects total Amazon revenue of $520 billion, up 11%, with profits of 56 cents a share, down from $3.24 a year earlier.

But to Amazon bulls, the issues plaguing the company are fleeting and priced in. While the economy could fall into recession later this year or in 2023, that recession won’t be permanent. Meanwhile, the e-commerce market continues to expand, and Amazon’s slice of the pie remains vast, at about 40%. There’s still room for additional market share gains, too.

The company’s advertising business, meanwhile, is on the rise. Given Apple’s (AAPL) tough stance on sharing information about consumer activity on the iPhone, advertisers are looking beyond Meta Platforms’ (META) Facebook, Alphabet’s (GOOGL) YouTube, and Snap for places to spend their ad dollars. Many ad buyers are turning to options where consumer buying intent is clear on the surface. Meta has to infer what you might want to buy; in Amazon’s case, consumers type their exact shopping interests into a search box. In a marketplace crowded with consumer choice, Amazon’s ad market is a gold mine.

And then there’s Amazon Web Services, the company’s mammoth cloud-computing platform. Since the company began breaking out results for AWS in 2015, the business has accounted for more than half of Amazon’s operating profits, including almost 75% of the total in 2021. In 2022, with e-commerce operations likely to lose money, AWS is forecast to constitute 150% of Amazon’s operating income.

With revenue close to $82 billion, AWS is one of the world’s largest software and services companies—bigger than Oracle (ORCL), IBM (IBM), or SAP (SAP), and more than twice the size of Salesforce (CRM), the largest of the so-called software-as-a-service companies. And AWS is going to get a lot bigger. It’s no wonder that when Bezos chose to step down as CEO in 2021, he chose as his successor AWS architect Andy Jassy. (Amazon declined to make Jassy or any other executives available for this story, citing the quiet period ahead of earnings.)

One of Wall Street’s favorite strategies for assessing corporate value is a “sum of the parts” approach: Make a list of what the company owns, put a value on each part, then add it all up.

For some of Amazon’s businesses, appropriate comparisons are hard to find. There are no pure-play public cloud stocks that look anything like AWS; its primary rivals—Microsoft (MSFT) Azure and Google Cloud—are likewise buried inside large businesses. Amazon’s ad business is valuable, but it’s linked to the core e-commerce business and therefore defies an easy value.

Then there’s Amazon Prime, which includes a Netflix-like video streaming service plus a Spotify-like music service. There are other businesses hidden in the company’s financials, including the videogame streaming service Twitch, the audiobook company Audible, the podcasting producer Wondery, and autonomous-vehicle maker Zoox, just to name a few.

In reporting this story, Barron’s found at least four different attempts by Wall Street analysts to suss out the company’s true value. They involve different parts, different metrics, and varying conclusions. The only consistent theme? Amazon’s parts add up to a lot more than its current market value.

Let’s start with the entertainment-focused approach from Needham analyst Laura Martin. In her view, a large part of Amazon’s value comes from its media businesses. She values Amazon Prime Video, Amazon Music, Twitch, and advertising at more than $500 billion. She values AWS at $650 billion. Those two numbers give you $1.15 trillion, or roughly Amazon’s current market value. That doesn’t include e-commerce, which Martin’s calculations currently ignore.

Truist internet analyst Youssef Squali has a different approach. He puts a value of more than $500 billion on Amazon’s “third-party retail” services business, which includes logistics and other services provided to millions of sellers. He adds $172 billion for “first party” retail—Amazon-branded goods, including electronics like Fire TVs and Kindles, plus thousands of AmazonBasics products. He values the company’s subscription business—basically Prime—at a little over $100 billion. Then, he values AWS at $867 billion, using a multiple of 30 times estimated pretax earnings for 2022. (Salesforce, which is growing more slowly than AWS, trades at roughly 30 times pretax earnings.) Ultimately, Squali comes up with an Amazon value of $1.7 trillion.

J.P. Morgan analyst Doug Anmuth takes the simplest view—dividing Amazon into two pieces. He pegs the value of AWS at 20 times his estimate of $52 billion in 2023 earnings before interest, taxes, depreciation, and amortization, or Ebitda, which comes to just over $1 trillion. For the retail business, he applies a multiple of 1.25 times his estimated gross merchandise value for 2023, which comes to just over $950 billion. Anmuth notes that Walmart (WMT) trades at about one times GMV, while Amazon’s retail business has “meaningfully higher” growth, meriting a higher multiple. For Anmuth, that’s a total Amazon value of $2 trillion.

The most aggressive sum-of-the-parts model comes from Redburn Research analyst Alex Haissl. In June, Haissl concluded that AWS is worth $3 trillion, based on growth expectations that are well above current Wall Street estimates. His view is that Amazon trades like a retail stock, which is inconsistent with the overwhelming importance of AWS to the business.

To be conservative, Haissl uses two-thirds of his $3 trillion AWS estimate in his sum-of-the-parts calculation. He then adds in contributions from each of the other business lines broken out in the company’s income statements—online stores, physical stores, third-party seller services, subscriptions, and advertising. His estimated total value: $2.8 trillion. Haissl’s target would make Amazon the world’s most valuable company, eclipsing Apple, which is currently worth $2.5 trillion, and Saudi Aramco (2222.Saudi Arabia), at $2.3 trillion. Haissl has a price target of $270 for Amazon shares, the highest on the Street.

Investors have long speculated about an AWS spinoff as one way to unlock more of Amazon’s cloud value. But AWS chief Adam Selipsky said earlier this year that Amazon has no plans to break up the business. CEO Jassy’s recent appointment after he spent years building AWS is also a strong indication that Amazon sees the cloud as the company’s future.

Haissl writes that spinning out AWS “may not be on the table for now,” but could happen down the road as the cloud unit continues to grow.

Haissl’s analysis—and why he argues that Amazon is so undervalued—requires a deep appreciation of Amazon’s cloud.

While AWS generally gets lumped in with Microsoft Azure and Google Cloud, the three services have varying strengths. Haissl, who also recently picked up coverage of Microsoft with a Buy rating, writes that Azure’s strength, predictably enough, is running Microsoft’s own software. Google Cloud has particular prowess in machine learning and artificial intelligence. But Haissl views AWS as the strongest cloud provider overall, with a platform that includes raw data storage, database software, applications, and analytics. Among other things, he thinks that AWS offers the most cost-efficient data-storage option—and some of the most powerful software tools for generating value from the internet’s trove of data.

Clouds start with a central storage service known as a “data lake,” which includes information in its rawest form. On top of that data lake are various connected services that make the raw data more valuable. Amazon offers more than 200 such applications, Haissl notes.

In Amazon’s case, its data lake is known as S3. Launched on Pi Day—March 14, 2006, S3 is shorthand for Simple Storage Service. The idea behind S3 is to provide a low-cost way to store data in bulk. It’s a digital version of a self-storage unit. And it has been a spectacular success, arguably the most successful single thing Amazon has ever created.

“Once they move into the next phase of technology adoption, there will be a data multiplier effect”

On S3’s 15th anniversary last year, AWS Chief Evangelist Jeff Barr wrote in a blog post that S3 now contains more than 100 trillion data objects—more than 13,000 for every human on the planet, “or 50 objects for every one of the roughly two trillion galaxies in the universe.” Haissl expects S3 to continue growing at a significant rate—he projects that it will expand revenue at better than 40% a year through 2030, with object growth over that span of nearly 60%. Haissl thinks S3 alone is worth $1.5 trillion, more than Amazon’s current market value, and estimates that S3 will account for 20% of AWS revenue this year—and close to 50% in 2030.

“Organizations are still at the beginning of implementing modern architectures and applying more-advanced technologies such as machine learning,” he wrote in late June. “Once they move into the next phase of technology adoption, there will be a data multiplier effect.”

Haissl argues that the storage efficiencies offered by S3 make AWS a cheaper cloud-computing option than rival offerings. As cloud computing takes a larger share of overall information technology budgets, he says customers will grow increasingly cost conscious.

Gartner estimates that the global market for public cloud services is now nearly $500 billion, growing to almost $600 billion next year. Synergy Research Group reports that AWS controls a third of the global market for cloud infrastructure. That’s 50% more than Azure, and more than triple the size of Google Cloud. All three are gaining market share from smaller players.

Success in the cloud can’t change a difficult near-term environment for Amazon’s retail business, but those issues are transient. “It will take time before costs and working-capital dynamics normalize after an extraordinary period, but from our perspective there are no structural issues in the business,” Haissl says. He thinks this recent quarter will mark the low point for Amazon’s retail arm.

Meanwhile, AWS will continue its ascent. And, at some point, retail will start growing again. By the time that happens, Amazon’s stock will already be headed to the clouds.