USA vill blåsa liv i IPO-boom med snabbare indexinträde

Börsoperatörer och finansmyndigheter i USA försöker blåsa liv i IPO-marknaden, skriver The Economist.

Genom lättare rapportkrav och snabbare inträde i stora index vill man locka snabbväxande jättar som Space X och Open AI. Förhoppningen är att vända en lång trend där allt fler storbolag har valt att förbli privata.

Kritiker varnar dock för att reformerna kan tvinga passiva fonder att köpa innan marknaden hunnit sätta ett rimligt pris.

The plan to make IPOs great again

America’s regulators and market operators are teaming up to rekindle public listings.

Anybody who has “not been through a public-company experience may think that being public is desirable. This is not so,” wrote Elon Musk to employees of SpaceX, his rocket company, in 2013. Mr Musk added that it might not go public “until Mars is secure”. Since then he seems to have softened his stance: SpaceX, which recently merged with xAI, his artificial-intelligence lab, is this year expected to list its shares in the largest initial public offering (IPO) of all time. The $75bn Mr Musk is reportedly seeking to raise, at a value for the company of $1.75trn, would be more than twice as much as the next-largest offering, of shares in Saudi Aramco in 2019.

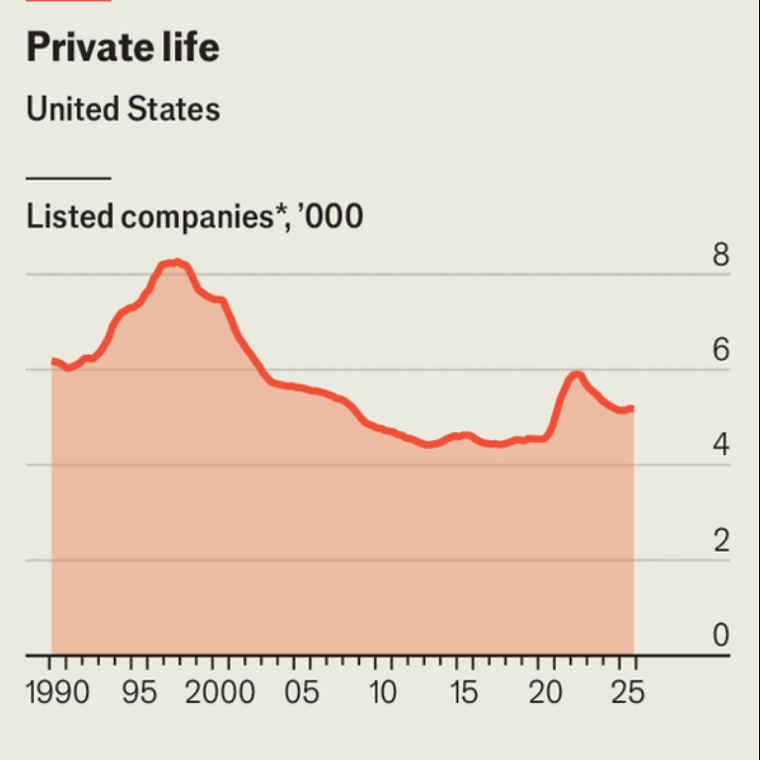

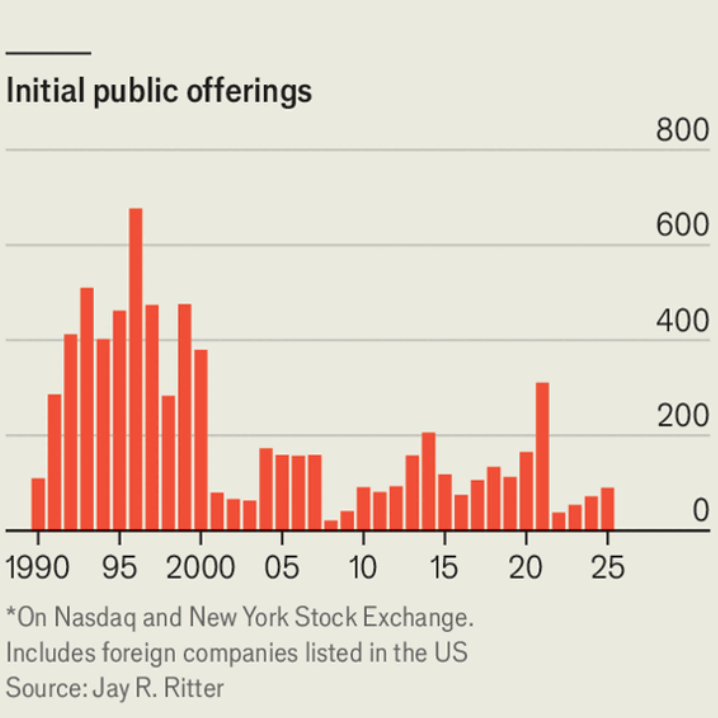

SpaceX may not be this year’s only mega-IPO; OpenAI and Anthropic, leading model-makers, are also said to be eyeing a listing. That will hearten those who have complained about the growing aversion of American companies to public markets. The number of businesses listed in America has fallen by more than a third since the mid-1990s as the cost of compliance has risen and private markets have expanded and matured (see chart). Buy-out barons have gobbled up many public companies, while startups have increasingly opted to remain in the hands of venture backers or else sell themselves to larger incumbents. Now, however, regulators and the companies that keep public markets running want to make IPOs great again.

In December Paul Atkins, head of the Securities and Exchange Commission (SEC), lamented that the diminution of public markets had “eroded American competitiveness, locked average investors out of some of the most dynamic companies and pushed entrepreneurs to seek capital elsewhere”. The SEC is pursuing several solutions, with a focus on reducing the regulatory burden of being a public company. It is currently drafting a proposal to allow listed firms to file reports twice a year rather than quarterly. It is also looking to reduce disclosure mandates such as those relating to climate change. And it wants to curb the power that proxy advisers, class-action litigants and other outsiders have over bosses.

Compilers of stock indices are also joining in the effort to revive interest in listings. They care because companies’ reluctance to go public undermines one of their main selling points: that their indices include the most important firms in the economy. According to S&P Global, which manages the S&P 500 and Dow Jones indices, the collective value of the ten largest venture-backed companies has increased by 1,500% over the past five years, to nearly $3trn. It and its competitors yearn to add these companies to their rolls.

The coming months will serve as a test of the balance of power between public markets and private firms

One proposal is to reduce the time businesses must wait after an IPO before they can be included in an index, known as the “seasoning” period, which at present usually ranges from three months to a year. That would bring forward billions of dollars’ worth of stock purchases by passive funds. Nasdaq is adopting a “fast-entry” period of 15 trading days for suspiciously SpaceX-shaped companies seeking admission to its Nasdaq 100 index; LSEG has suggested five trading days for entry to its Russell indices. Another carrot they are considering is reducing the percentage of shares companies must float before being eligible for index inclusion. S&P Global is reportedly weighing similar changes.

For Nasdaq, encouraging more companies to go public would be doubly sweet, since it also runs a stock exchange that rakes in fees when firms list (and annually thereafter). It is competing with the New York Stock Exchange to win the SpaceX listing, and Mr Musk has reportedly made early index inclusion a condition of gaining his favour.

The three mega-IPOs will also gladden those who want to see the wealth generated by AI spread more widely. Still, there may be losers from the changes. Consider the impact on passive funds. One purpose of the seasoning period is to allow the market to settle on a price for a firm’s shares before these investors must buy them; reducing that period may force the funds to buy overpriced shares. The problem may be compounded by the change to the free-float rules, which would mechanically raise demand from passive funds while keeping the supply of shares down, pushing up the price. Since 1980 all but one of the large firms that initially floated less than 5% of their stock underperformed the market over the next three years, according to data gathered by Jay Ritter of the University of Florida. Retail traders may also struggle to get their hands on the shares of the hottest companies.

The coming months will serve as a test of the balance of power between public markets and private firms. At present the latter seem to have the upper hand. Index operators in particular are “anxious to please without regard to potential consequences”, says Patrick Healy, who has negotiated IPO terms with them for many big companies. Still, there are limits to the sway of bosses such as Mr Musk, who need the vast pools of money available in public markets to fund their ambitions. After all, getting to Mars is not cheap.

© 2026 The Economist Newspaper Limited. All rights reserved.