Världens äldsta bank till salu – ingen vill köpa

Följetongen kring världens äldsta bank, Monte dei Paschi di Siena, har varit en riktig långkörare på den italienska finansscenen. Nu hoppas premiärminister Georgia Meloni få vara den som lyckas med det som alla hennes föregångare misslyckats med, nämligen att sälja det upprustade bankvraket, skriver Bloomberg Businessweek.

Problemet? Det finns inga italienska köpare som verkar intresserade.

A Plan to Rewrite the Ending of Italy’s Monte Paschi Saga

The government aims to sell the bank to a rival of similar size, but so far no one seems interested.

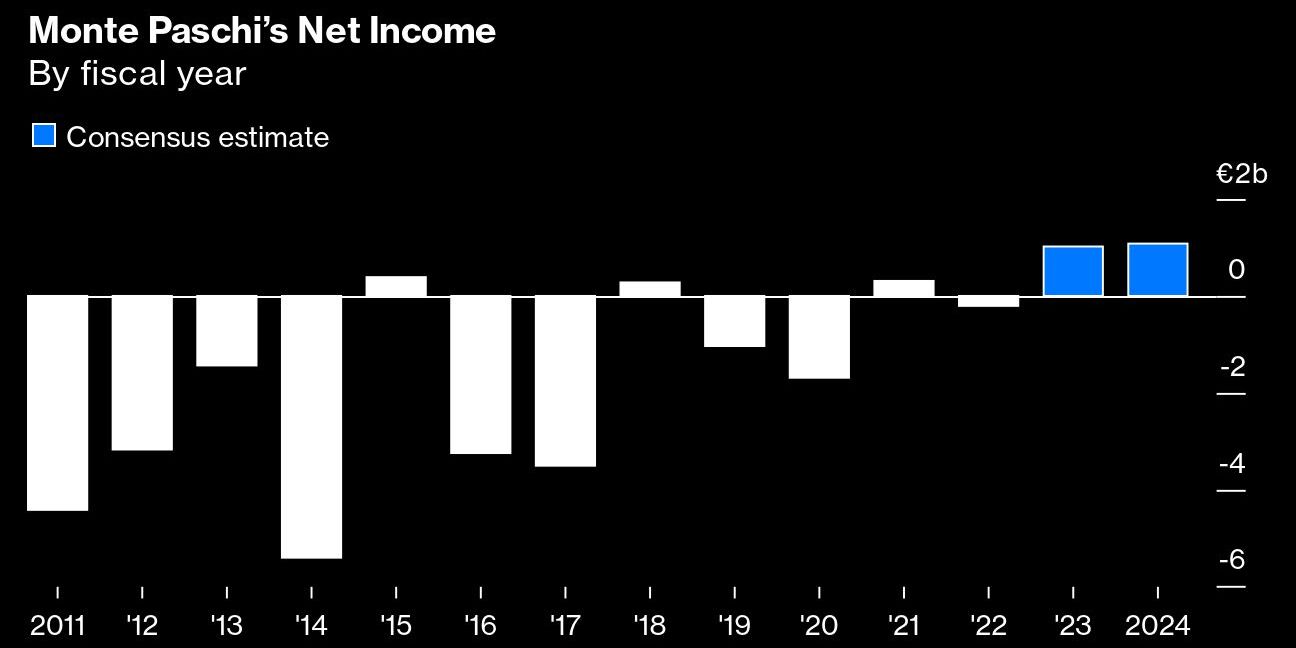

Banca Monte dei Paschi di Siena SpA is the longest-running soap opera of Italian finance. Tracing its roots to 1472 as a funder of agricultural and commercial activity in the Republic of Siena, the bank later expanded throughout the peninsula. Fast forward a few centuries, and Paschi had grown into one of Italy’s biggest lenders by the time an ambitious expansion just before the 2008 financial crisis set the stage for tragedy. With Paschi reeling from billions in losses after pricey deals, top managers engaged in actions that would see them tangled up in years of legal proceedings. In 2017 the state took a controlling stake in the bank.

Now, Italy’s government aims to rewrite the ending by merging Paschi with a rival, which would create the country’s third-biggest lender while giving Prime Minister Giorgia Meloni bragging rights for fixing a seemingly endless problem that various predecessors had failed to resolve.

The plan is missing just one crucial detail: a buyer.

”The economic environment is deteriorating, and there are few peers that can afford an all-cash deal”

The government has no formal power to force any other lender to purchase its 64% stake in Paschi. Although the bank seems to be on stable footing, its scandal-ridden past—and the €18 billion ($19 billion) in fresh funds it’s burned through during the past 15 years—makes it a tough sell. “I don’t see room for a sale of Monte Paschi in the short term,” says Massimiliano Romano, a partner at consulting firm Concentric. “The economic environment is deteriorating, and there are few peers that can afford an all-cash deal.”

Meloni’s administration has put its hopes on rivals of a similar scale. The plan for offloading Paschi would keep what’s considered the world’s oldest bank under domestic ownership while complying with European Union regulators, who allowed the nationalization on the condition that Paschi be reprivatized, with an initial deadline of 2021 that was extended to 2024.

Paschi is in much better shape than just a few years ago. A rebuilding strategy led by Chief Executive Officer Luigi Lovaglio and soaring lending income on the back of interest-rate increases have put the bank on track to post annual profit of more than €1 billion for the first time since 2007. There’s been “flawless execution of the turnaround,” says Filippo Alloatti, head of financials at London investment firm Federated Hermes Ltd. “Now is the time to push for reprivatization.”

As an interim step, the government is planning to offer as much as 15% of Paschi in a smaller placement and is seeking advisers for the sale, according to people with knowledge of the matter, who asked to remain anonymous discussing private negotiations. That would buy the government time and show it’s committed to complying with the EU rules while making the remaining stake less expensive for any potential partner, the people say.

Among Italian banks, the universe of potential acquirers of the scale the government envisions pretty much boils down to two, and neither appears eager to get into bed with Paschi. The first is Milan-based Banco BPM SpA, which sends out a statement saying it’s not interested in any acquisitions every time speculation about a possible tieup with Paschi surfaces. That’s at least in part because Banco BPM’s bosses fret that any affiliation with the once-troubled lender will take a bite out of the share price, says Vincenzo Longo, a strategist at IG Markets Ltd. “Paschi still carries a stigma, so shareholders may be upset if they think the bank is considering a deal,” Longo says.

“Paschi still carries a stigma, so shareholders may be upset if they think the bank is considering a deal”

The other candidate, Modena-based BPER Banca SpA, hasn’t said whether it might step up, but it’s still digesting a complex merger with Banca Carige SpA that it completed last year. And its main investor, Unipol Gruppo SpA, recently doubled its stake in Banca Popolare di Sondrio, fueling speculation that that lender, not Paschi, will be BPER’s next target. Unipol and BPER declined to comment.

Either candidate would find it difficult to pay the whole Paschi purchase price in cash. The alternative—swapping some of the buyer’s stock for shares in the target—would turn the government into an owner of the acquiring company. Neither bank would likely welcome state ownership, and since the state would effectively still own part of Paschi, such a deal would risk violating the exit pledge.

A government plan to merge Paschi with another lender two years ago ended in embarrassment for then-Prime Minister Mario Draghi when UniCredit SpA walked away from the talks. Foreign banks with large operations in Italy, such as Credit Agricole SA and BNP Paribas SA, have more cash in hand and could probably afford a takeover. But selling a company as important as Paschi to a foreign lender would appear to go against the nationalist leanings of the current government.

Paschi was first bailed out in 2009, after a disastrously timed deal plunged it into chaos when the financial crisis hit. In the following decade it piled up more than €20 billion in losses as it burned through the cash that shareholders and taxpayers kept shoveling into it through various financing rounds. In 2019, Paschi managers were convicted of colluding with bankers from Deutsche Bank AG and Nomura Holdings Inc. to hide losses by using complex derivatives trades, but that conviction was overturned last year, with an appeals court ruling there was no grounds for a trial. Prosecutors are appealing the ruling.

The deadline imposed by the EU doesn’t help, as potential buyers may prefer to wait for the deadline to approach—increasing the government’s desperation to cut a deal and allowing a buyer to extract more favorable terms. “It looks like an uphill struggle,” says Francesco Galietti, founder of Rome political risk consultant Policy Sonar. “With the clock ticking, the government will need to keep sweetening the offer if it hopes to complete a sale.”

For more articles like this please visit us at bloomberg.com