Sagan om självbetalande skattesänkningar lever vidare

Donald Trump har lovat att sänka skatterna om han blir president, och att dessa skattesänkningarna ska betala sig själva. Löftet är inte nytt utan har upprepats av alla republikanska presidenter sedan Ronald Reagan, skriver Bloomberg.

Logiken är att när skattebördan minskar blomstrar företagen, produktiviteten ökar och därmed statens intäkter. Problemet är att den slutsatsen är felaktig, enligt nyhetsbyrån.

Reagans skattesänkning 1981 minskade den federala budgeten med 9 procent och George Bush lämnade efter sig det största underskottet i USA:s historia efter sina skattesänkningar.

Tax Cuts Pay for Themselves and Other Fairy Tales

Historian Rick Perlstein on how a crackpot idea that took root in the Republican Party in the 1980s is getting a second wind under Trump.

During Donald Trump’s 90-minute presidential nomination acceptance speech at the Republican National Convention in July, the falsehoods flew so fast and thick that the most important fact-checking site didn’t even notice one of the most outrageous ones—maybe because his party has been repeating it for so long that it’s simply taken for granted.

Buried 4,023 words into the 12,187-word address was the statement that after he signed the Tax Cuts and Jobs Act into law in 2017, the federal government “took in more revenues the following year than we did when the tax rate was much higher.” In fact, federal revenue remained level in nominal terms, and as a percentage of gross domestic product—the relevant measure—it fell a full percentage point. A 2018 analysis by the nonpartisan Congressional Budget Office estimated that the TCJA would end up costing the US Department of the Treasury $1.9 trillion over 10 years.

Never mind the numbers. Trump’s bunkum repeated an article of right-wing faith: Federal tax cuts “pay for themselves,” because decreased tax burdens unshackle the economy to be radically more productive. This is no more true today than it was when Ronald Reagan first started making the claim shortly before he first ran for president.

The story of how the crackpot idea took root in the Republican Party—and endures despite being debunked by reality time and time again—makes for an important lesson. Fantastical promises of impossible miracles have always structured the political appeal of American conservatism, which its latest Trumpian incarnation has only amped up.

The story starts in the 1970s with the trauma of “stagflation.” Prior to its emergence, economics policy was believed to possess the power to sculpt the economy like lumps of clay. But the simultaneous occurrence of stagnant economic growth and inflation—a theoretically impossible combination according to the regnant Keynesianism of the day—reduced the profession “to offering blathering and gibberish in lieu of analysis,” recalled Reagan’s budget director, David Stockman.

Into this intellectual vacuum poured conservative economists, armed with panaceas. Some were the most distinguished practitioners in the field: Nobel laureate Milton Friedman, with his theory of “monetarism,” that inflation could be corralled and economic growth reignited just by controlling the size of the money supply; Robert Lucas, another Nobel Prize winner, with a sophisticated mathematical explanation about why government intervention in the economy was ultimately futile; and the “new public finance” school of Harvard’s Martin Feldstein.

Some of the others, to put it mildly, were not.

These were the figures who prevailed in the contest of ideas

One of the architects of what came to be called “supply-side theory,” Wall Street Journal editorial-page editor Robert Bartley, had no economics training at all. Neither did his star “theorist,” Jude Wanniski, a WSJ editorial writer who claimed to have picked up the basics of the dismal science as a habitué of Las Vegas blackjack tables. The presence on the team of Robert Mundell lent a misleading air of intellectual gravitas to the project. His work on international currencies during the 1960s would later win him a Nobel. But by the time Mundell hooked up with the supply-side gang, he’d long since beaten a retreat from the field’s mainstream to argue ideas—which Friedman called “sheer quackery”—at conferences he put on at his villa in the Italian countryside.

And remarkably, these were the figures who prevailed in the contest of ideas. Perhaps it was because the theory they peddled was so simple to explain to policymakers. The non-peer-reviewed paper by which Wanniski introduced it to the world contained no formal models or data, merely a series of just-so stories about everyone, from the author of the Federalist Papers to Roman emperors and babies in their cribs.

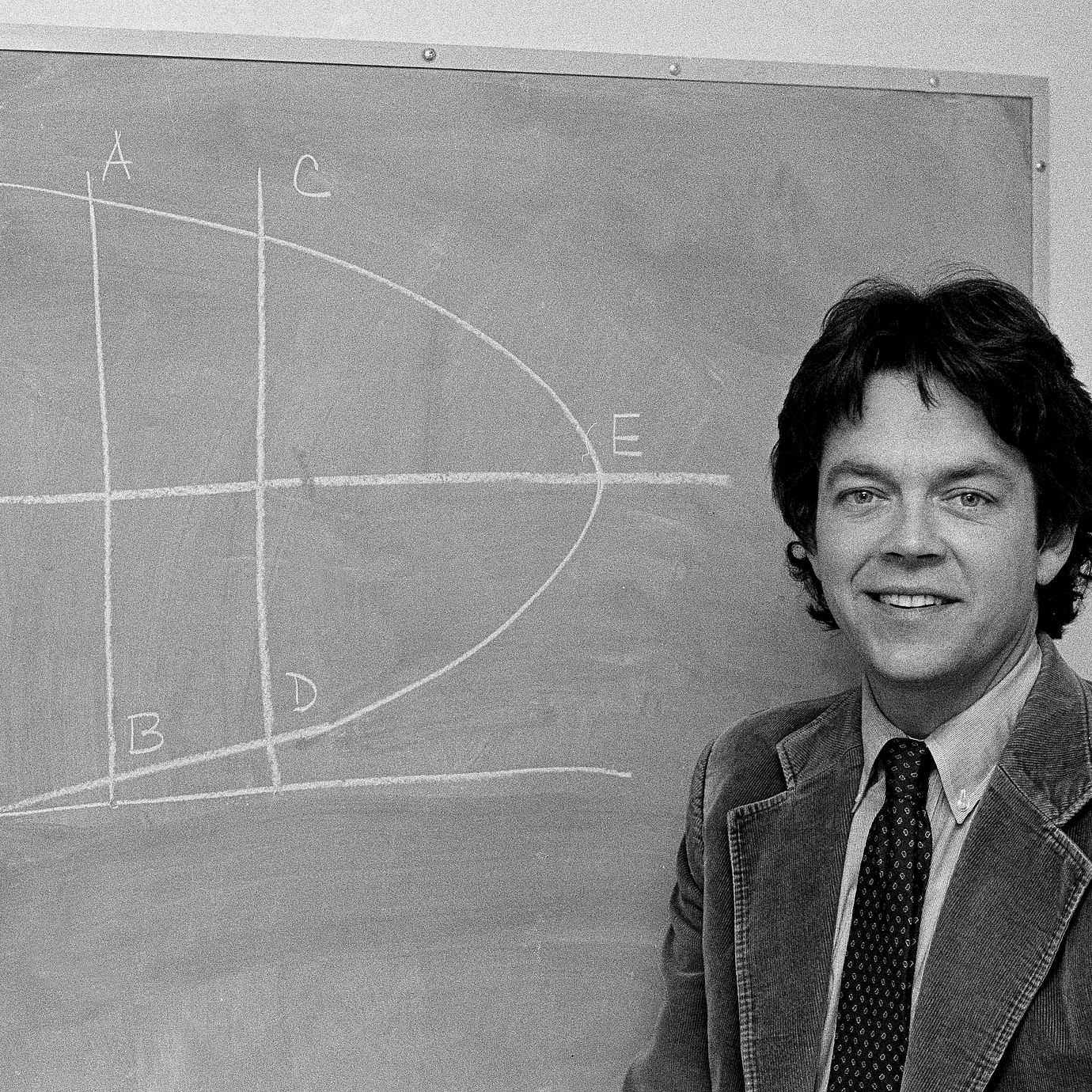

For those who may have lacked the patience to even read through it, Arthur Laffer—a real-life economist who attached himself to the project after inception—claimed the whole thing could be distilled into a single chart. He famously sketched it out for White House chief of staff Richard Cheney on a napkin in 1974. All it took was fixing tax rates at precisely the correct point—the apex of the so-called Laffer curve.

Miracles would follow, the Lafferites promised, at the mere announcement of the new, proper tax rate. The economy would grow so quickly that tax revenue would end up increasing. The federal budget could thus stay balanced without the need for painful (and also unpopular) spending cuts. Americans would shower the party responsible for lightening their tax burden with votes.

Reagan was particularly entranced by this fantasy. He first started selling the idea in his nationally syndicated newspaper column and five-minute radio editorials, which boosted its biggest backer on Capitol Hill, Representative Jack Kemp of New York. Reagan was so exuberant about it that in 1985, the second-term president told Congress, “You cannot show me a single time in history when a major tax cut did not result in greater revenues.”

“You cannot show me a single time in history when a major tax cut did not result in greater revenues”

Legislators could have responded: “What about the tax cuts you signed in 1981?” Within a couple of years, those had led to a 9% drop in federal revenue—which is why Reagan found himself forced to enact three tax hikes in the subsequent four years.

Nevertheless, by the end of Reagan’s presidency something dangerous had happened. Republicans, all evidence to the contrary, had locked themselves into thinking that tax cuts did result in higher government revenue.

When George W. Bush became president in 2001, he argued that the budget surplus he’d inherited from the outgoing Clinton administration was “the people’s money” and not Washington’s to spend. When Bush’s first tax cut passed, supply-side propagandist Lawrence Kudlow proclaimed, “Faster economic growth and more profitable productivity returns will generate higher tax revenues at the lower tax-rate levels,” adding that “budget surpluses will rise, not fall.”

Instead, Bush bequeathed Barack Obama the biggest deficit in American history. Some conservatives kept the lie going nonetheless. In 2009, Representative Louis Gohmert of Texas gave a speech in Congress in which he claimed, Trump-like, that Bush’s two tax cuts “created the greatest revenue coming into the US Treasury in American history, more money than ever coming into the Treasury.”

At least one conservative was dismayed. “There is no evidence,” National Review’s Kevin Williamson wrote in a 2010 article titled “Goodbye, Supply Side.” It was “a bedtime fairy tale Republicans tell themselves.”

I found Williams’ candor remarkable. A few years later, I contacted him to ask what happened after he’d rendered a detailed, empirical argument for why the article of faith upon which conservatives built their entire economic church was a fantasy. What had the response been on the right? Nothing, he replied, before revising his answer: Some Republican politicians admitted that he was correct but that it was “hard to get them to acknowledge it in public because it’s become such a piece of dogma.”

Lo and behold, a few years after that, at a debate hosted by the business cable network CNBC, one Republican presidential candidate after another described the economic miracles that would ensue from their tax-cut plans—with one Donald Trump promising that the economy would “take off like a rocket ship.” One of the moderators, John Harwood, replied that White House economic advisers from both parties had told him Trump had as much a chance of “cutting taxes that much without increasing the deficit as you would of flying away from the podium by flapping your arms.”

While conservatives may be in thrall of reckless fantasies, markets will no longer be fooled

Be that as it may, by 2022 the fallacy had flapped its way all the way across the Atlantic and into the infamous “mini-budget” of Prime Minister Liz Truss. But in the context of the United Kingdom, the notion that tax cuts pay for themselves made even less sense. The dollar is the primary reserve currency used by the rest of the world. That provides the US an ever-present market for its debt should the reckless experiments of its Treasury Department fail. Investors who understood that the British economy had no such backstop pulled so much money out of the country that Truss’ premiership wilted faster than a head of lettuce.

It is a valuable lesson: While conservatives may be in thrall of reckless fantasies, markets will no longer be fooled.

You’ll never catch Trump (or just about any conservative) uttering the words “supply side,” but their appeal survives. Laffer, he of the curve, remains a player in Republican economic policy circles. His name was on a short list of potential candidates to replace Jerome Powell as chair of the Federal Reserve that Trump’s advisers drafted earlier this year.

Which would have been quite a thing, for the original recipe to bring the supply-side Elysium into being also called for abolishing the central bank itself and resuscitating the gold standard. Fundamentalists will tell you that the reason tax cuts have never achieved their promised budgetary effects is because this has not come to pass.

Maybe the fourth time will be the charm.

Stephen Moore, another longtime supply-side propagandist, co-authored the 2018 book Trumponomics with Laffer, which claimed that the president’s tax cuts would not add a dime to the budget deficit. In fact, passage of the TCJA was followed by a 40% revenue decline within two years. In 2019, Moore’s nomination to serve as a governor of the Federal Reserve was scotched after he admitted on Bloomberg Television that he was not well acquainted with “how the Federal Reserve makes its decisions.”

The humiliation didn’t stand in the way of Moore being tabbed to co-author the chapter on the Treasury Department for the Heritage Foundation’s Project 2025. And just this September, Trump said that with the even more ambitious tax cuts he’s promising—an assortment that includes everything from further reductions to the rates on corporate income to special exemptions for tipped workers and senior citizens—“I look forward to having no deficits within a fairly short period of time.” Being on the supply side means never having to say you’re sorry.

For more articles like this please visit us at bloomberg.com