Tullpanik kan trigga farlig dominoeffekt på marknaden

Marknadskaoset efter Trumps senaste tulloffensiv riskerar att skapa en självförstärkande kris, skriver The Economist. Faran är att ”paniken på marknaderna kan bli självuppfyllande”.

Stora Wall Street-banker har utfärdat de största marginalkraven på hedgefonder sedan pandemin, vilket tvingar fram snabba försäljningar av likvida tillgångar. Även amerikanska statsobligationer har sålts av – ett ovanligt tecken på stress i systemet.

Nästa steg kan bli ännu större tvångsförsäljningar, stigande kreditspreadar och ökad press på redan skuldsatta företag.

Where real danger might lurk in chaotic markets

The worry is that wild swings could cause their own damage.

Wild market moves are normally unnerving because they reveal how quickly sober-minded investors can give in to terror. Just now the scariest thing is how rational those scrambling to sell appear. Share prices around the world have cratered since Donald Trump announced his latest and biggest suite of tariffs on April 2nd, before stabilising a little on April 8th. Yet uncertainty around Mr Trump’s tariff plans remains. Although many market participants have held out hope that the new barriers would be swiftly lowered, perhaps after Mr Trump had used them to extract concessions from trading partners, the president still seems to suggest that the duties are coming.

As ever when prices swing wildly, a worry is that the swings will cause their own damage, which is when things can get really nasty. That threat loomed in 2022, when big drops in British government-bond prices imperilled pension funds that had made outsize bets on them, prompting the Bank of England to intervene and stabilise the market. The previous year turbulent prices felled Archegos, a buccaneering family office whose failure cost its bankers billions of dollars. In each case, sudden market moves led to the institutions involved facing margin calls on their loss-making positions, which they had to sell assets hurriedly to meet. In turn, this made the markets even wilder.

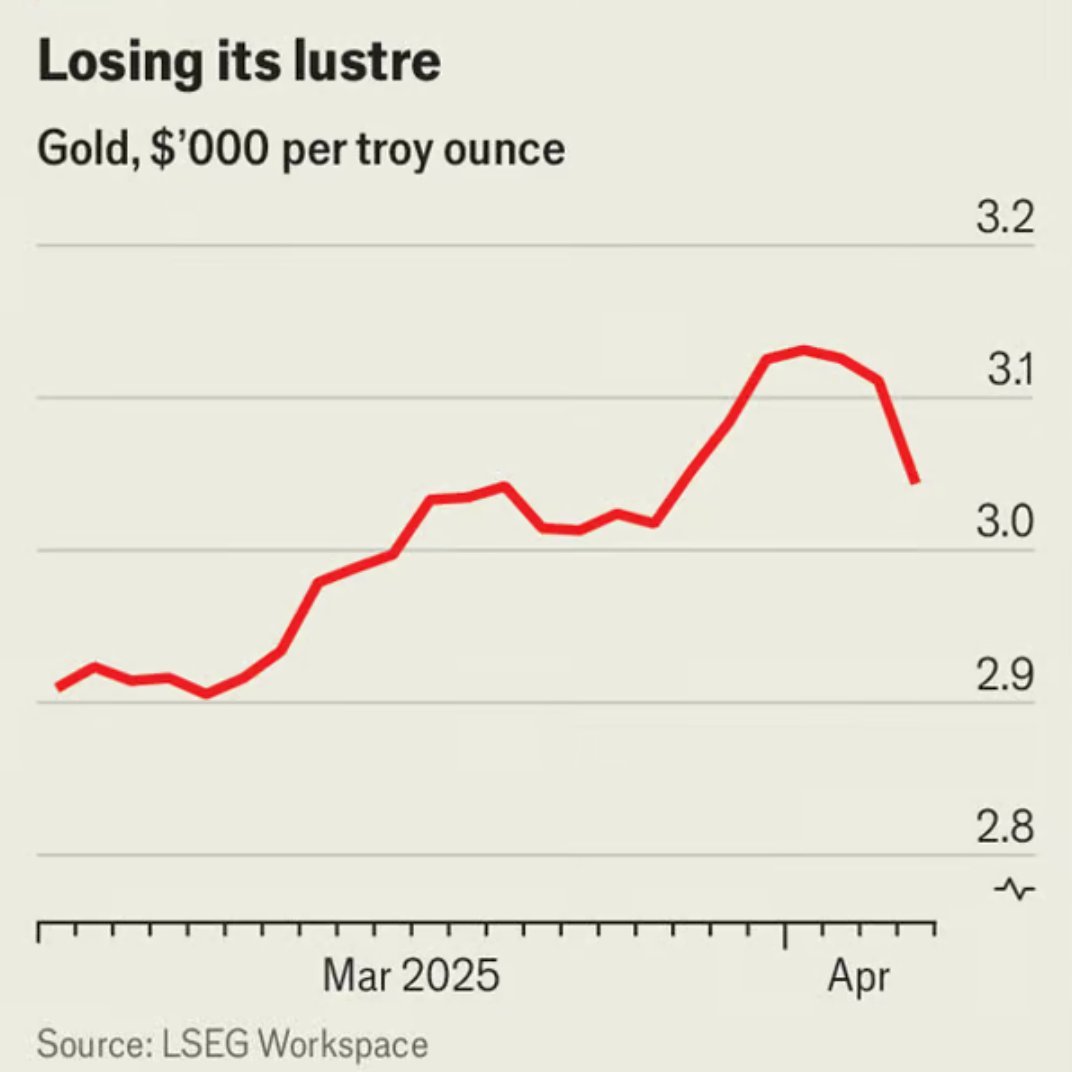

Could such a doom loop emerge now? There are ominous signs. The Financial Times reports that several Wall Street banks have hit their hedge-fund clients with the biggest margin calls since 2020, meaning they must stump up cash to cover their losses. In recent days American share prices have plummeted almost as fast as they did then, when the onset of the covid-19 pandemic shuttered much of the global economy. Concerningly, even the gold price dropped sharply in the days after Mr Trump’s announcement. Since gold is usually seen as a hedge against disaster, this sort of move suggests fire sales, with traders having to offload their most liquid assets to meet margin calls. On April 7th the price of Treasury bonds, another usual haven, fell as well.

At the time of writing, these moves would need to gain momentum to be truly troubling. But there are still good reasons to think that the panic in markets may become self-fulfilling. One is that gauges of expected volatility for the coming month have soared. These are implied by the insurance premiums traders pay to protect themselves from big swings in stock prices, bond yields and exchange rates. All have jumped over the past few days. The VIX index, which measures expected volatility for American stocks, has rocketed. For risk managers, such moves are a signal to tap their traders on the shoulder and instruct them to close their riskiest positions, to limit the potential damage from future turbulence. If that happens at many banks, hedge funds and asset managers at once, it is a recipe for forced sales and yet more volatility.

The corporate-bond market is another channel through which expectations could become self-fulfilling. As fears of a global recession mount, and investors mark up the odds that the firms will default on their debt, borrowing costs have leapt. The average extra yield paid by risky “junk bond” issuers in America, over and above that on Treasury bonds, has climbed to 4.5 percentage points, from 2.6 in mid-February. For companies with the riskiest credit ratings, of “CCC” or lower, it is now an eye-watering 11 percentage points. Firms with debt that is about to fall due have little choice but to pay such rates. The resulting squeeze will crimp their ability to spend and invest, making a slowdown—and a wave of defaults—more likely.

In different circumstances, investors would expect central bankers to slash interest rates in an attempt to loosen financial conditions and offset the hit to economic growth. Instead, on April 4th Jerome Powell, the Federal Reserve’s chairman, suggested that the Fed would “wait for greater clarity”. Consumers and market participants alike already expect Mr Trump’s levies to raise inflation; for the central bank to cut rates too quickly would risk more self-fulfilling worries of the runaway sort. And so Mr Powell appears reluctant to put a floor under the market. If investors are frightened, they have every reason to be.

© 2025 The Economist Newspaper Limited. All rights reserved.