”Världens energimarknader är farligt nära sammanbrott”

Världens oljemarknad må se relativt lugn ut, men under ytan håller buffertarna på att ta slut. Efter snart två månaders krig mot Iran har 550 miljoner fat råolja från Gulfregionen redan gått förlorade, skriver The Economist.

De sista tankfartygen som hann passera Hormuz före kriget har nu nått hamn, medan Asien ransonerar bränsle och raffinaderier drar ner produktionen. Europa har hittills skjutit upp smällen med subventioner. Men läget är skört.

”Det finns ingen buffert kvar som kan skydda världen från utbudschocken”, skriver tidningen.

Global energy markets are on the verge of a disaster

Scenarios now range from bad to awful.

Traders of oil futures are a sunny bunch. On April 17th, after Iran’s foreign minister declared the Strait of Hormuz “completely open”, the price of Brent crude fell by 10%, to $90 a barrel. Within hours Iran reversed course and attacked an Indian tanker. The next trading day the global benchmark rose by just 5%. It remains around $20 below its high in late March, even though an American blockade on Iranian oil means even more oil is trapped in the Gulf.

Fifty days into the Iran war the world has lost 550m barrels of Gulf crude—nearly 2% of last year’s global output. Every month Hormuz stays closed, the world misses out on 7m tonnes of liquefied natural gas (LNG), worth 2% of its annual supply. Yet in Western countries, which host the largest futures markets, pain remains limited. Petrol is a bit pricier, but most households can still afford to drive. Trucks keep trucking. Planes continue to fly. Fuel stocks remain close to pre-war levels.

This comforting picture is deeply misleading. By April 20th the last few oil tankers to cross Hormuz before the war began reached their destinations, in Malaysia and California. There is no buffer left to protect the world from the supply shock, at a time of the year when demand from holiday drivers starts to pick up.

To gauge how close the world is to energy catastrophe, The Economist has gathered a dashboard of indicators. It suggests that grave damage has already been done. Worse, without a reopening costs could soar, triggering events that cause the fuel system to seize up. A reopening of the strait now would—just—avoid a complete disaster. But some additional pain is already inevitable.

Three factors are pushing the world towards the cliff edge. Oil cargoes available to buy are drying up. Refineries are slashing output of fuel. And demand remains artificially high, especially in Europe. Something big must give somewhere large for energy markets to balance.

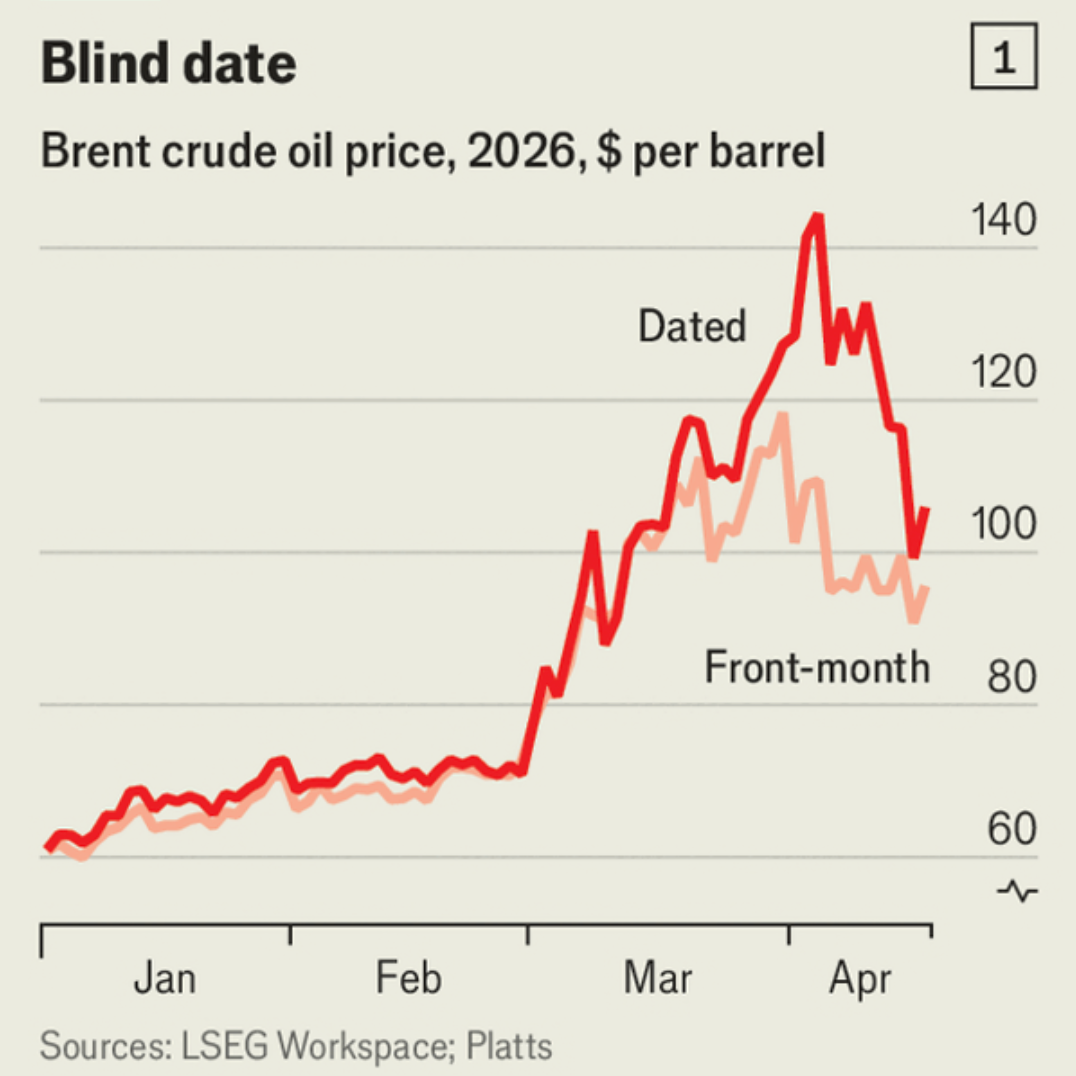

Take trade first. One reason the largest supply shock in petroleum history has not triggered global panic is that a near-record amount of oil was already at sea when the war started. As American warships set sail for the Gulf in February, countries there cranked up exports. After the latest deliveries, those seaborne stocks are now exhausted. So are most cargoes of Iranian and Russian oil, which were loitering at sea but found buyers after America eased sanctions on the two countries. Total volumes on water have fallen at record speed (see chart 1). For jet fuel and petrol they are well below historical norms, and possibly close to the minimum required for seaborne trade to function.

This leaves Asia, which used to receive four-fifths of Gulf exports, in a particular bind. Commercial inventories in a few Asian countries are running out. South Korea is due to taper releases from its strategic reserves in the coming days. Japan’s will be exhausted in May. Crude stocks in Asia excluding China fell by 67m barrels, or 11%, in the month to April 19th, according to Kayrros, a firm that estimates inventories using satellite imaging.

A shortfall of raw materials has forced Asian refiners to slash throughput by over 3m barrels a day (b/d), or 10% of their combined capacity. That could accelerate to 5m b/d in May and, if the strait remains closed, 10m b/d in July, says Neil Crosby of Sparta Commodities, a data firm. China could help by releasing some of the 1.3bn barrels of crude it holds in reserve. Instead it has suspended exports of refined products. A trader familiar with its energy strategy reckons it will not open the taps before a lasting truce. All this compounds shortages created by the loss of Gulf exports of finished fuel, on which Asia also relies.

If Europe keeps subsidising consumption, markets will get more out of whack

Refined-fuel prices are already very high. In Asian spot markets, petrol nears $120 a barrel, diesel $175 and jet fuel $200, up from $80, $93 and $94, respectively, before the war. Demand is adjusting, partly by government decree. Seven countries have imposed work-from-home mandates and at least five are rationing vehicle fuel, alongside imposing school closures and other measures. High prices are doing their bit, too. From small miners to fisheries, businesses without adequate diesel stocks are working part-time. Some plastics factories have shut units because they cannot afford naphtha, another oil product. The combination of state and self-imposed rationing may cause Asian crude demand to shrink by nearly 3m b/d in April compared with February.

Europe has so far avoided demand destruction. Governments are working hard to preserve people’s purchasing power. Of the 27 European Union countries, 16 are using taxpayer money or cutting fuel taxes to shield consumers from higher prices. European refiners have thus barely slashed production.

But, like their Asian counterparts, they, too, must buy crude at a much higher cost than Brent futures suggest. A better gauge is Dated Brent, the price for real cargoes delivered in the next few weeks. The spread between the two—usually $1-2—widened greatly in April, reflecting fears of near-term shortages, according to Platts, which produces the benchmark (see chart 1). It has narrowed since but remains bigger than usual (and does not include eye-watering freight rates and other costs).

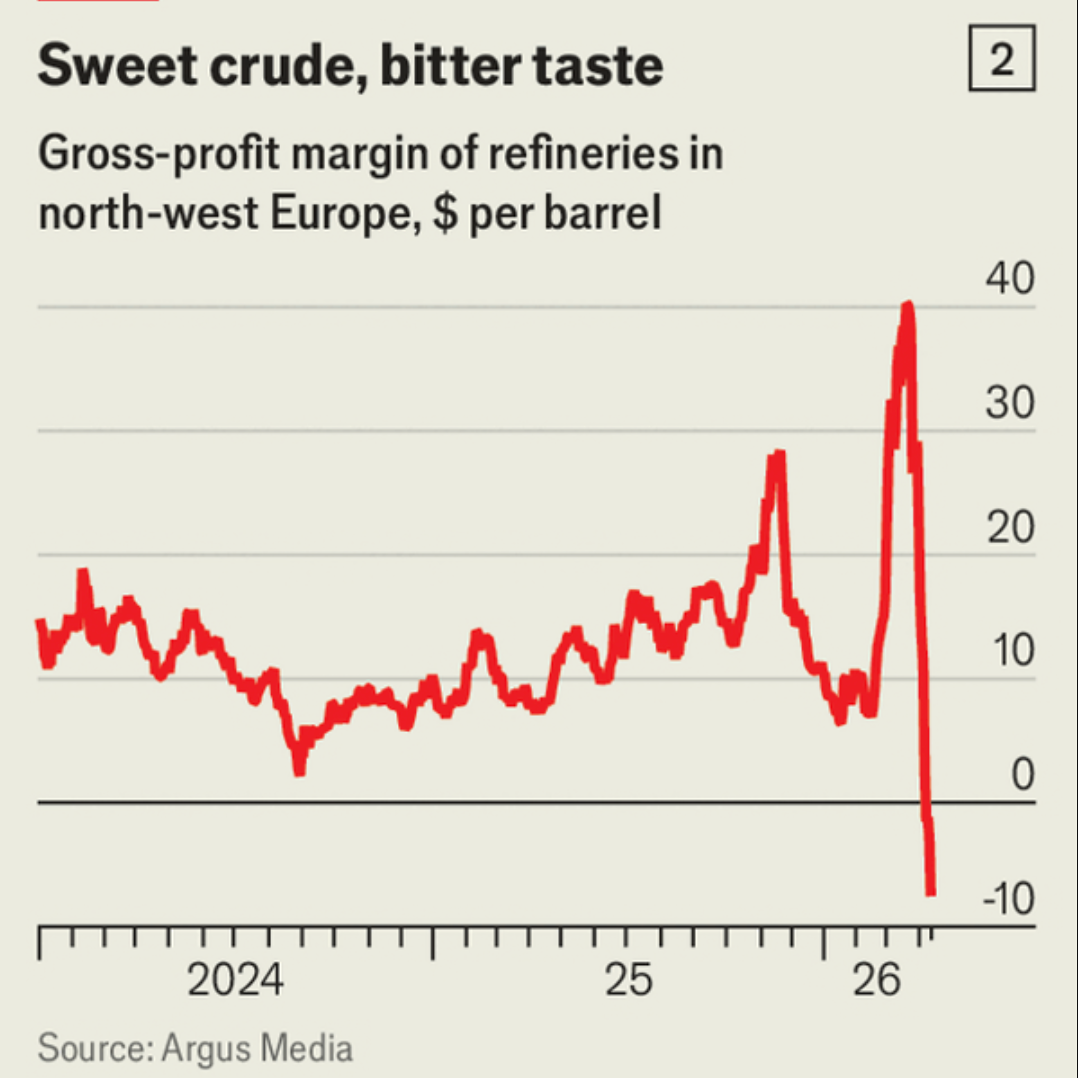

Raw material at near $130-150 a barrel has pushed European refiners’ margins into the red, reckons Benedict George of Argus Media, a price-reporting agency (see chart 2). Extreme backwardation—when commodity spot prices are much higher than those for futures—crushes their profits: they must pay up for crude now but sell their products at lower futures prices. Before long they will need to cut output.

If Europe keeps subsidising consumption, markets will get more out of whack. For one thing, prices for products will keep rising. America, where demand tends to jump in a period of summer road trips, will push them further. Competition for LNG, shortage of which was mostly absorbed by Asian consumers’ self-deprivation and a switch to coal, will also increase when Europe starts restocking gas for the winter.

Fast-depleting stocks make matters worse. Europe’s reserves of jet fuel cover some 50 days of consumption, their typical level. But modelling by Michelle Brouhard of Kpler, a data firm, for The Economist shows that European stocks will fall precipitously if Hormuz flows do not normalise by June. Those in other importing regions may disappear even faster (see chart 3). The outlook could worsen if America, seeking to tame domestic prices, emulates China and bans exports of refined products, which have risen by nearly half since the start of the war.

Futures markets have a different view of things. Yet even if Hormuz reopened today, it would take months for Gulf crude output, shipping and refinery production to resume in full. Saad Rahim of Trafigura, a trader, reckons a cumulative loss of 1.5bn Gulf barrels, or 5% of annual global output, is almost unavoidable. If the strait does not reopen, it could easily reach double that. The last time oil demand fell by 10% in short order was during the covid-19 lockdowns of 2020, a shock that also brought about a fall in world GDP of more than 3%. The time to avoid a similar tumble is running out.

© 2026 The Economist Newspaper Limited. All rights reserved.